.){kind=link}

Markets

All eyes are on Wednesday’s US CPI inflation print and to a lesser extent its PPI precursor tomorrow. That led to stoic, listless trading at the start of the new week. China announced during early Asian dealings that it will kick off its CNY 1tn stimulus plan on Friday with a CNY 40bn 30-yr auction of special bonds (of which the proceeds are used for predetermined investments). It’s the first round of the many that will stretch the year through November, with maturities ranging between 20 and 50 year. News of the rare event (China has issued special bonds on four occasions only, this one included) pulled Chinese equities from the intraday lows but had little impact on markets ex-China. European stocks lose some minor ground with the likes of the EuroStoxx50 shedding 0.2%. US stocks open with marginal gains of about 0.3%. Most commodities are well bid with oil seeking a gain to $83/b after a sharp drop earlier this month. Copper is on track for the highest close since April 2022. Core bonds gained some ground with a slight outperformance of US Treasuries vs German Bunds. US yields ease between 2.4 (30-yr) and 3.4 bps (2-yr). German rates give up 1.7-2.8 bps across the curve. Japanese yields are the odd one out today, having added up to 2.7 bps at the long end of the curve. This followed the Bank of Japan offering to purchase a smaller amount of government 5-to-10 year bonds in a regular operation than it did the previous time (April 24). While the amount was still within the planned range for the running quarter, it is seen as a baby step by the central bank to reduce its presence in the debt market and an attempt to support the ailing currency. The Japanese yen barely, if at all, profits though. USD/JPY holds steady around 155.7 even as the US dollar is suffering a bit from the Monday blues. DXY eases from 105.3 to 105.12 currently. EUR/USD is flirting with the 1.08 big figure compared to an 1.768 open. Technically, resistance is spotted at 1.0807, followed by 1.0885 (38.2% recovery on the December-April decline; April correction high). Sterling whipsawed within an extremely tight trading range between 0.8595 and 0.8611. The UK labour market is scheduled for release tomorrow. It’s one of the two reports that the Bank of England receives ahead of the June policy decision, along with two CPI prints. The data will be crucial with the central bank in last week’s meeting looking to cut rates sooner rather than later.

News & Views

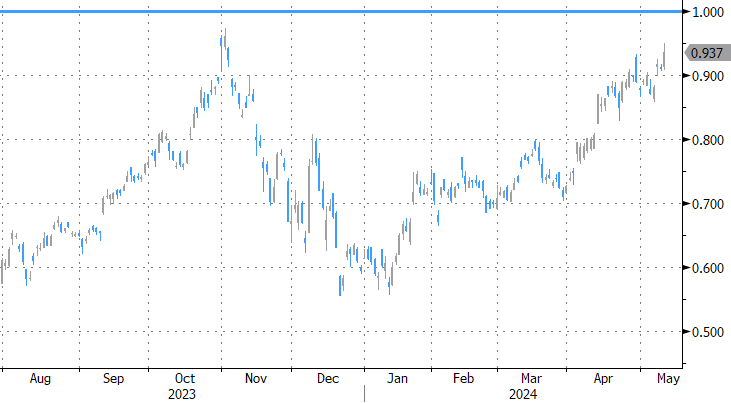

Czech inflation in April accelerated more than expected by 0.7% M/M with the Y/Y-figure approaching the upper band of the tolerance band around the Czech National Bank’s 2% inflation target (2.9% from 2% in March). The CNB in its spring monetary policy report (published early May) only expected a rebound to 2.5% Y/Y. The deviation was mainly due to food prices which rose 1% Y/Y instead of the projected -0.5% Y/Y decline. In line with expectations, core inflation slowed slightly further to 2.6% Y/Y. The CNB reacted that the qualitative message of the spring forecast remains valid with inflation moving back close to the 2% target throughout the year. The Czech koruna rallied after inflation numbers with EUR/CZK testing the 200-day moving average at 24.75 (strongest CZK-level since early February). CZK swap rates rose up to 9 bps at the front end of the curve. Today’s figures strengthen the case for a reduction in the CNB rate cut pace from the next meeting onwards (25 bps instead of 50 bps).

Polish Monetary Policy Council member Kotecki currently doesn’t see any room for interest rate cuts. Some room may come at the end of the year if wage growth slows. It doesn’t seem to be the base case and any potential rate cut will just be the minimal 25 bps. MPC Wnorowski also sees stable rates in 2024 as the base scenario and even thinks that the likelihood of a rate cut this year is smaller than a month ago. He also thinks that 2025 is too distant of a future to give already guidance on the scale of any potential cuts. The Polish zloty at EUR/PLN 4.30 holds strong against the euro.

Graphs

EUR/CZK: Czech crown rallies after CPI accelerates more than expected, bolstering case for slowdown the easing pace

Japanese 10-yr yield rises to new YtD high after BoJ cuts buying amount in regular bond auction

Copper prices on track for highest close since early 2022. Will Chinese stimulus boost demand further?

EUR/USD attacks 1.0805 in quiet trading and ahead of important US data tomorrow (PPI) and Wednesday (CPI)