to be confident that inflation is returning to the 2% target. Earlier in the week, Boston Fed Collins, SF Fed Daly and Atlanta Fed Bostic all said that reaching that confidence will “take more time” than previously thought with Minneapolis Fed Kashkari also hinting that policy rates will remain at the peak levels for an extended period of time.){kind=link}

Markets

Fed speak cemented the higher-for-longer case last week. On Friday, governor Bowman said she doesn’t expect any policy rate cuts this year. Following three or four months on inflation disappointments, she wants to see a number of months of progress (and a number of probably meetings as well) to be confident that inflation is returning to the 2% target. Earlier in the week, Boston Fed Collins, SF Fed Daly and Atlanta Fed Bostic all said that reaching that confidence will “take more time” than previously thought with Minneapolis Fed Kashkari also hinting that policy rates will remain at the peak levels for an extended period of time. Chicago Fed Goolsbee, dove by nature, was the odd one out last week. He said that he doesn’t see much evidence of inflation stalling out at 3%, but doesn’t want to tie his hands when it comes to the timing of making monetary policy less restrictive. Recent eco data confirmed the inflation threat/risks. Accelerating prices paid components for example clashed with weakening growth momentum in ISM surveys. Friday’s University of Michigan consumer survey showed a similar split. Economic sentiment hit a YtD low while inflation expectations rose to a YtD high for the short-term (1-yr; 3.5%) and the long-term (5-10-yr; 3.1%). US Treasuries underperformed German Bunds with US yields closing 5 bps (2-yr) to 3.1 bps (10-yr) higher. Changes on the German curve ranged between +3.1 bps (2-yr) and +2.1 bps (30-yr). Correcting oil prices ($84.5/b to $82.5/b) partially help explain the curve move. The dollar kept a narrow trading range with EUR/USD closing at 1.0771. The eco calendar is thin today with NY Fed inflation expectations and more Fed speak. US PPI data are a step-up tomorrow to Wednesday’s April CPI print. Retails sales are due the same day.

EUR/GBP closed the week below 0.86 (0.8595) even as the Bank of England May policy meeting suggested that the BoE could cut its policy rate when it meet next in June. BoE Ramsden joined Dhingra in already voting for a rate cut (7-2) with the forward guidance in the policy statement now extended with the sentence “The Committee will consider forthcoming data releases and how these inform the assessment that the risks from inflation persistence are receding”. New inflation forecasts (based on the current market rate path) suggest inflation to drop to 1.9% by Q2 2026 (from 2.2%) and to 1.6% by Q2 2027. It prompted comments by BoE governor Bailey that the central bank could end up easing somewhat more. This week’s labour market report and Q1 wage data (PAYE) will immediately give an indication if current market pricing (50% probability for June) is too conservative or not. We err on the side of a June rate cut, sticking with our negative GBP-bias.

News & Views

Chinese inflation rose by 0.1% M/M and 0.3% Y/Y in April, up from 0.1% Y/Y in March. Core inflation, excluding food and energy, rose 0.7% Y/Y (0.6% in March). Services price rose 0.8% Y/Y. Food prices continue to decline (-2.7% Y/Y). While slightly higher than expected, the data still indicate mediocre demand in the Chinese economy as authorities are putting in place a policy of balanced economic stimulus. Chinese producer price growth in April remained deep in deflationary territory at -2.5% Y/Y. Even as it improved from -2.8% in March, it remained lower than expected and negative since October 2022. Other data this weekend also showed that aggregate financing in the country unexpectedly declined in April, the first decline since 2005. Lower than expected government bond issuance and weak overall demand for borrowing contributed. In this respect, the government announced to start selling a total of CNY 1 tn government bonds with ultra-long maturities with a first sale of 30-y bonds expected as soon as next Friday.

US president Biden is rumoured to announce a sharp rise of tariffs of several (strategic) goods the country is importing from China. The US is said to maintain existing tariffs on many goods that were decided by the previous government. At the same time, tariffs would be raised in sectors like semi-conductors and solar equipment, batteries, but also steel and aluminum. The Tariff on Electrical Vehicles for China even is said to be raised from 27.5% to 102.5%.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

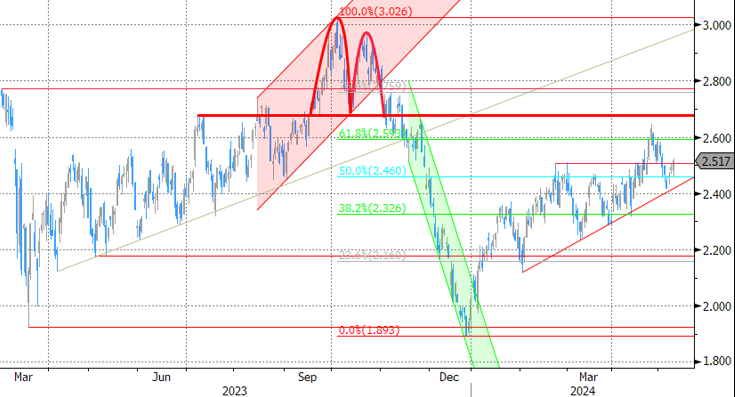

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.