{kind=link}

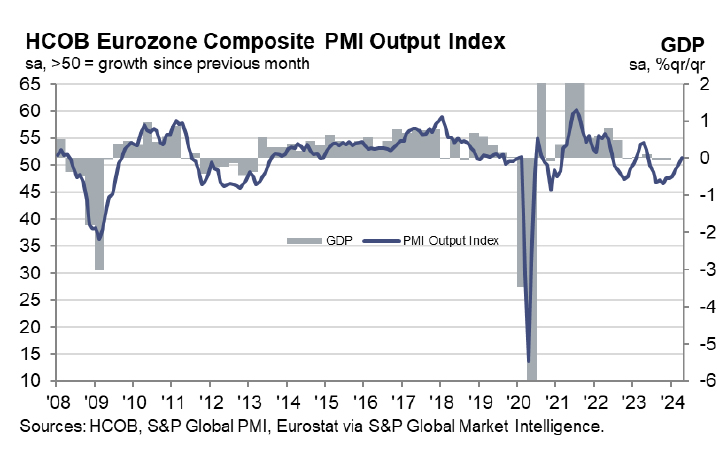

Eurozone’s PMI Manufacturing fell from 46.1 to 45.6 in April, below expectation of 46.5. PMI Services rose from 51.5 to 52.9, above expectation of 51.8, an 11-month high. PMI Composite rose from 50.3 to 51.4, also an 11-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that Eurozone had a “good start” to Q2, with GDP projected to expand by 0.3%, mirroring the growth rate of the first quarter.

De la Rubia outlined three factors contributing to the sustainability of the recovery. Positive momentum in new business over the past two months has spurred more aggressive hiring policies. Service providers have shown confidence in their pricing power. The recovery in Germany and France, Eurozone’s largest economies, have particularly underscored the broader regional trend.

However, the latest figures pose a critical test for ECB on its readiness to cut interest rates in June. The “accelerated increases in input costs”, driven by higher oil prices and wages, necessitates close scrutiny. Moreover, the quicker pace at which service sector companies are raising prices suggests that “services inflation will persist”.

Despite these inflationary pressures, HCOB still expects an ECB rate cut in June, although de la Rubia expects ECB to proceed with more caution rather than adopting the “pragmatic speed” earlier suggested by Governing Council member François Villeroy de Galhau.