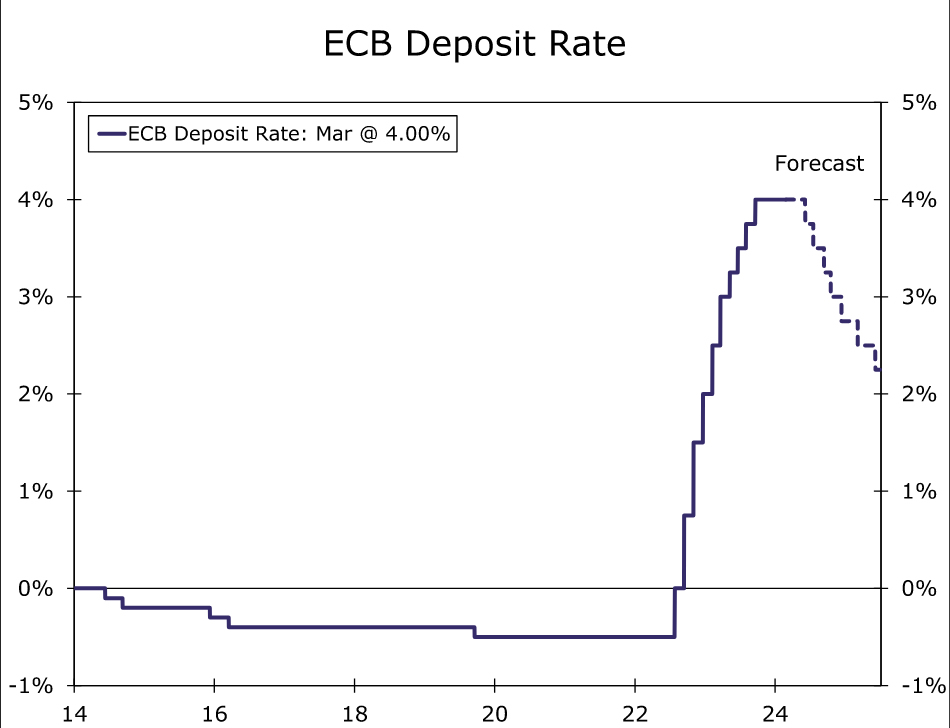

ended its tightening cycle with a final 25 bps rate hike in September last year and has, since early 2024, indicated the next move is likely to be a rate cut. The outlook for ECB monetary easing has been fluid, with expectations for an initial ECB rate cut at times fluctuating between April and June. That said, firmer Eurozone PMI surveys, a still-gradual disinflation process, and the weight of ECB policy rhetoric have seen expected rate cut timing shift more solidly towards June. In that context, we now also expect the ECB will begin its easing cycle with a 25 bps Deposit rate cut to 3.75% at its June monetary policy announcement.){kind=link}

Summary

The Eurozone economy faced a particularly challenging period during the second half of 2023, with the region only narrowly avoiding a technical recession. Given the challenging growth environment, the European Central Bank (ECB) ended its tightening cycle with a final 25 bps rate hike in September last year and has, since early 2024, indicated the next move is likely to be a rate cut. The outlook for ECB monetary easing has been fluid, with expectations for an initial ECB rate cut at times fluctuating between April and June. That said, firmer Eurozone PMI surveys, a still-gradual disinflation process, and the weight of ECB policy rhetoric have seen expected rate cut timing shift more solidly towards June. In that context, we now also expect the ECB will begin its easing cycle with a 25 bps Deposit rate cut to 3.75% at its June monetary policy announcement.

Eurozone Economy Shows Tentative Signs of Stabilization

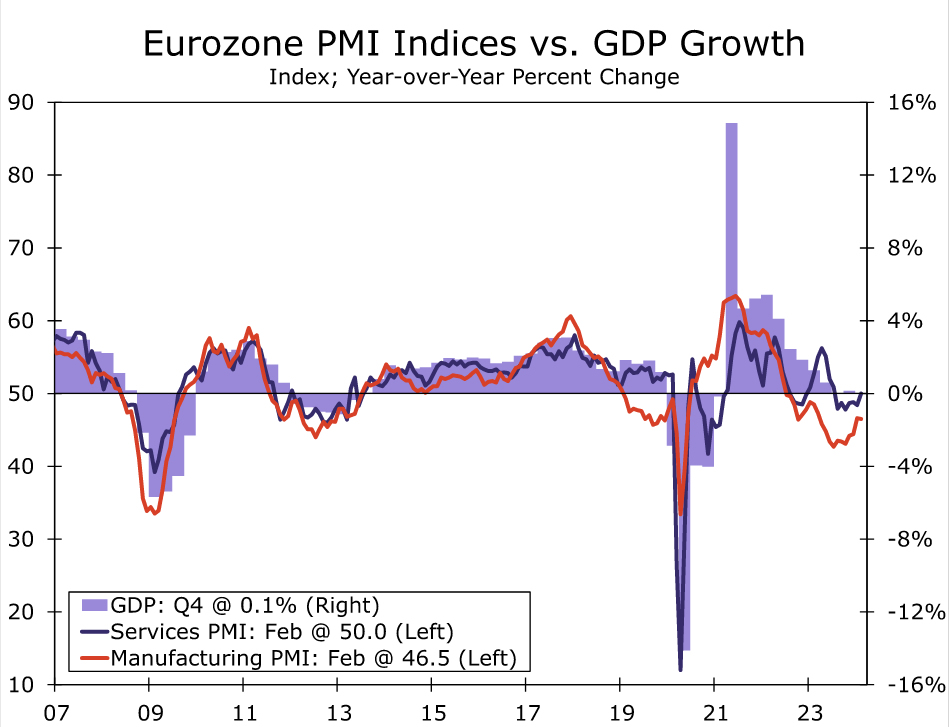

One of the most significant data releases since the European Central Bank’s (ECB) most recent policy announcement was the Eurozone PMI surveys for February. Of particular note, the February service sector PMI rose more than expected to 50.0, from 48.4 in January. That saw the services PMI exit contraction territory for the first time since July of last year. Service sector sentiment for the region’s largest economies was also favorable, as Germany’s services PMI rose to 48.2 and France’s services PMI rose to 48.0. The news from the Eurozone manufacturing PMI was not as upbeat, as that index unexpectedly eased to 46.5 in February from 46.6 in January, driven by weakness in German manufacturing. Still, with the service sector a much more sizable portion of the overall economy, the Eurozone composite PMI also rose to 48.9 in February, from 47.9 the prior month. Although not as significant as these headline figures, the details of the February PMI survey also hinted at lingering inflation pressures. The report noted that growth of average input costs across producers of goods and providers of services accelerated for a second successive month to reach the highest level since last May. The report also said that selling price inflation likewise accelerated, up for a fourth month running in February to also hit the highest level since last May.

Other confidence surveys since the ECB’s latest announcement are more mixed. At a national level, Germany’s February IFO business confidence index rose to 85.5, but French business confidence and Italian economic sentiment both fell in February. Meanwhile, the European Commission’s Economic Sentiment Indicator for the Eurozone also fell to 95.4 in February, but that same survey showed the Employment Expectations Indicator edging up to 102.5 in February, a level historically consistent with positive jobs growth. That suggests steady Eurozone labor market trends can continue. In recent weeks, labor market indicators have shown continued employment growth in Q4 of 0.3% quarter-over-quarter and 1.3% year-over-year, and a January unemployment rate that fell to 6.4%, a record low. Taken together, the firming in the PMI indices and mixed readings from other sentiment surveys, along with steady labor market trends, offer early—albeit tentative—signs the Eurozone economy is stabilizing. At the margin, we think tentative economic stability has reduced the urgency for ECB monetary easing, and is a contributing factor to expectations for an initial ECB rate cut getting pushed back to mid-year.

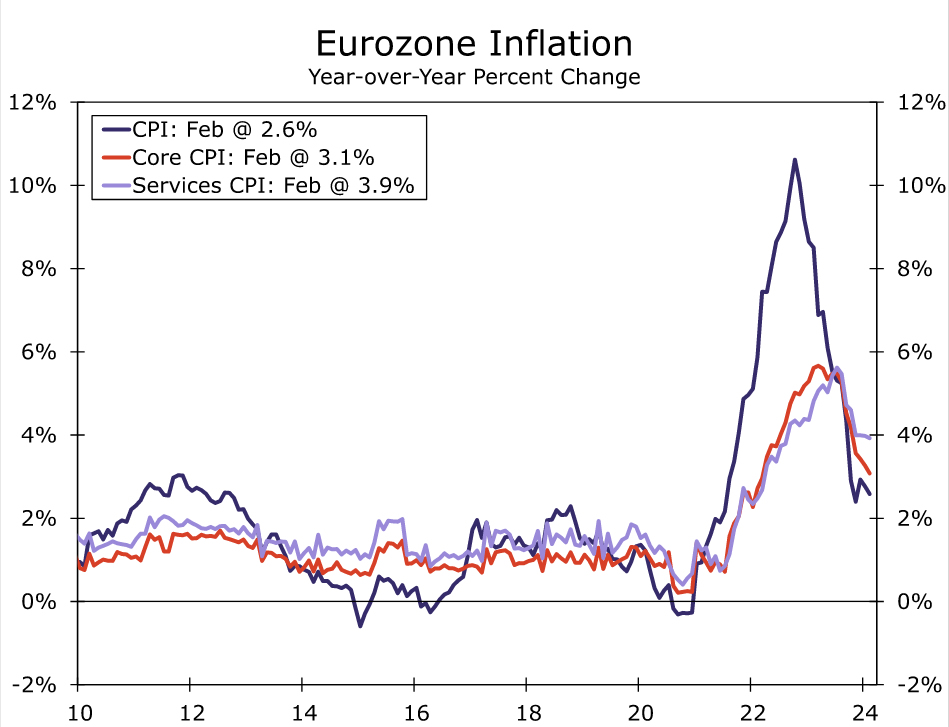

Eurozone Inflation News Still Favorable, But How Long Will It Continue?

The other key pieces of Eurozone economic news since the ECB’s latest policy announcement were inflation data for January and February. Those figures revealed some further progress on the disinflation front, albeit at a gradual pace. For the February CPI, headline inflation slowed to 2.6% year-over-year and core inflation slowed to 3.1% year-over-year. Service sector inflation remained somewhat sticky, easing only slightly to 3.9%. To be sure, the deceleration in annual inflation was flattered by base effects related to the large price increases that were seen in early 2023. Taking a closer and more granular look and price trends over the past six months, we note that the CPI excluding food and energy—which is close to but not identical to the official core CPI measure—has advanced at a 2.3% annualized pace. Thus even over this shorter time period, underlying inflation trends have moved closer to, but not yet converged, to the ECB’s 2% inflation target. And likely of concern to ECB policymakers, services inflation has persisted over the past six months, rising at a 3.4% annualized pace during that period.

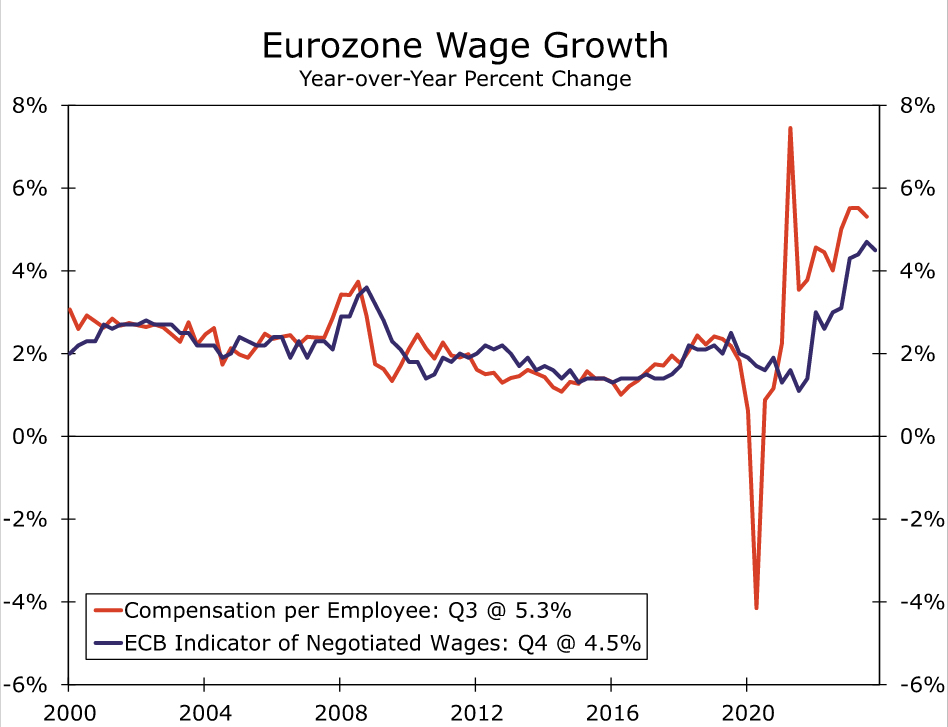

Another reservation regarding the inflation outlook, and one cited by several ECB policymakers, is the still-elevated pace of wage growth. The most up-to-date wage figures available on a Eurozone-wide basis is the ECB’s indicator of negotiated wages. The negotiated wage index decelerated slightly to 4.5% year-over-year in Q4 from 4.7% in Q3 but, at least for now, suggests wage growth is at a level that is probably still too high to achieve the 2% inflation target on a sustained basis. The fact that the unemployment rate is at a record low perhaps reinforces concerns that wage growth may decelerate only gradually. It is against this backdrop, and despite the improving inflation trends of the past several months, that ECB policymakers have been wary of moving too aggressively in lowering interest rates, and have indicated an increasingly clear preference to see wage trends from early 2024 before making a decision to adjust interest rates. Those wage data for early 2024 will only be available in time for the ECB’s June monetary policy announcement, and not for the ECB’s April monetary policy announcement.

Chief among comments from policymakers have been those of ECB President Lagarde. Among her more recent comments, she said the ECB must be convinced that disinflation is sustainable and that Q1 wage data will be important for the ECB’s assessment. Some other policymakers (Nagel, Holzmann, Schnabel) have cautioned against early rate cuts, while others have indicated a desire to see more wage data or even cited June as more likely timing for initial ECB easing. In the wake of these comments, market participants are now pricing in just 6 bps of rate cuts for the April meeting, and 24 bps of rate cuts for the June meeting.

Given current market pricing, it would likely take a proactive effort from ECB policymakers to accelerate the market’s easing expectations and to allow for an April rate cut to become a more realistic possibility. That proactive guidance from ECB policymakers is something we view as a low probability outcome. Indeed, for those hoping for dovish elements from the ECB monetary policy announcement on 7 March, at best we expect the ECB to repeat it is “not there yet” on inflation, to perhaps caution against premature monetary easing, and to repeat that its preference is to see more wage data before adjusting its policy interest rate. At worst, we would not completely rule out more aggressive guidance in which the ECB takes the possibility of an April rate hike off the table. The other key element of the ECB’s March monetary policy announcement to watch will be the central bank’s updated economic projections. In the absence of a significant downward revision to its inflation forecast (in December, the ECB projected CPI inflation ex food and energy at 2.3% in 2025 and 2.1% in 2026), there would also be little reason for market participants to pull forward their expected rate cut timing. Since we view dovish policy guidance and/or a sharp downward revision to inflation forecasts as unlikely at the ECB’s March announcement, and at the risk of adjusting our own forecasts with ‘perfectly imperfect’ timing, we now view an initial 25 bps Deposit Rate cut to 3.75% at the ECB June’s monetary policy announcement as the most likely outcome.

Beyond the initial June move, we expect the ECB will keep lowering interest rates in steady 25 bps rate cut increments at the following meetings. We expect Eurozone economic growth to improve, but remain moderate overall. Meanwhile, we expect wage growth in particular, and price inflation to a lesser extent, to decelerate further as the year progresses. Should those economic trends transpire, we forecast the ECB will follow up with 25 bps rate cuts at the July, September, October and December meetings, which would see the Deposit Rate end 2024 at 2.75%. As the ECB’s policy rate moves somewhat closer to a more neutral level and economic activity firms further in 2025, we expect a step down in the pace of ECB rate cuts to once per quarter next year. We forecast 25 bps Deposit Rate cuts in March, June and September 2025, which would see the ECB’s policy rate reach a terminal level of 2.00% by late next year.