{kind=link}

Fed Preview: Low-Key Optimism

- We do not anticipate the Fed to make changes to its monetary policy in the December meeting, in line with broad consensus and market expectations.

- Focus will be on the updated economic projections, where the 2024 ‘dot’ could be revised slightly lower, yet still above market pricing. Growth forecasts could be lifted slightly, while inflation projections are likely to remain mostly unchanged.

- We stick to our long-standing view that the Fed will initiate quarterly 25bp rate cuts from March. Current pricing signals limited downside potential for longerdated UST yields, but still rhymes with lower EUR/USD in 2024.

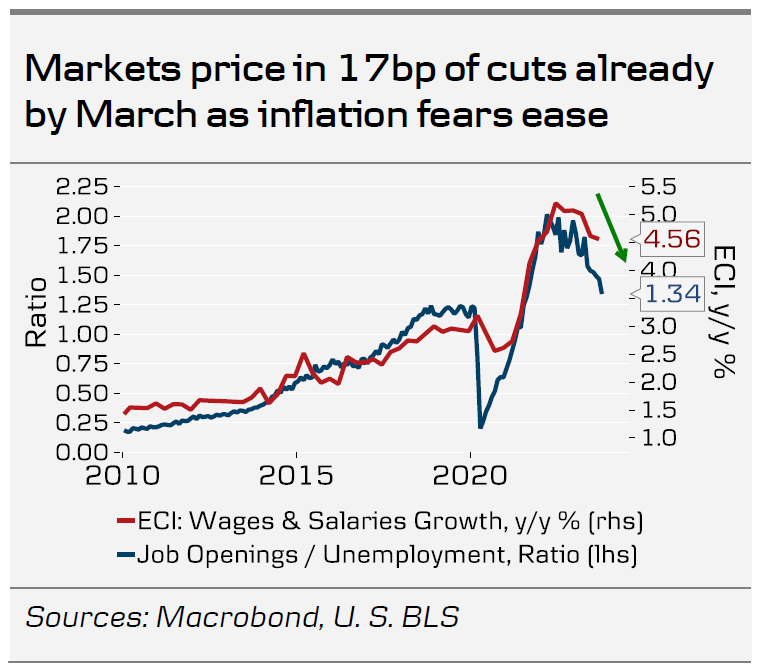

The recent FOMC commentators have made one thing clear ahead of the December meeting: now is the time to be patient. Markets have priced out any chance for a further hike and now expect the first cut in either March or May. And we would agree, as we still expect the first cut in March, followed by quarterly 25bp reductions through 2024-2025. First cut 9 months after the final hike would be well in line with historical standards.

In his final speech ahead of the blackout, Powell made little effort to guide the markets for next year. While few FOMC participants have openly discussed the case for rate cuts so far, there has been surprisingly little pushback to the sharp easing in financial conditions.

And for a good reason. Lower inflation expectations have pushed real rates to undoubtedly restrictive levels, while rising labour supply, cooling demand and higher productivity all support the case for easing underlying price pressures. Oil prices continue to fall despite the OPEC+’s supply cuts, suggesting that markets are now pricing in clearly cooling aggregate demand. It is still too early to celebrate victory over inflation, but between the lines the Fed appears to share markets’ optimism for now.

To be clear, we continue see some risks of persistent inflation over the long run, stemming from relatively tight labour, energy and housing markets. But as inflation looks to settle closer to 2-3% in 2024-2025, the nominal policy rate will have to be adjusted lower. If our forecasts of quarterly rate cuts and gradually cooling inflation hit the spot, the real policy rate would average 2.6% in 2024, which is still a clearly restrictive level in our view.

This is also what the markets are pricing in, as real short rates are seen stabilizing at 1.0- 1.5% over the next decade. In other words, the current rate cut pricing reflects expectation of cooling inflation and not a looming recession.

As all recent FOMC commentators aside from Michelle Bowman have suggested that they do not anticipate further hikes in their baseline view, the 2024 ‘dot’ could shift lower by 25bp (to 4.75-5.00%). 2023 and 2024 GDP forecasts will likely be adjusted slightly higher on stronger realized data, while inflation forecasts are likely to remain mostly untouched.

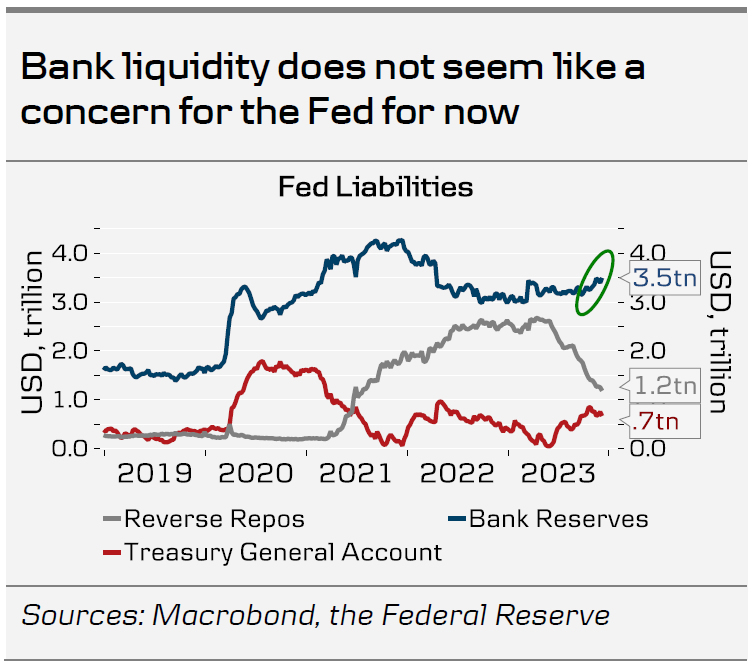

We will also watch out for any questions on the recent spike in SOFR and whether Powell sees it as a concern for the Fed. From liquidity perspective, we still doubt this is the case, as the drawdown of the ON RRP has meant that US bank reserves currently remain at a higher level than at the start of the year despite the ongoing QT.

Markets: December meeting unlikely to rock the boat

We expect a muted reaction in bond markets to the FOMC bringing the dots better in line with recent development. Nevertheless, the rapid repricing of policy expectations the past weeks has left bond yields sensitive to any signs of deviations from the current disinflation narrative for 2024. The bar for the FOMC to markedly affect market pricing seems high, as long as data continues being in favour of an early start to rate cuts.

As such, we do not foresee substantial influence on EUR/USD either. Our projection for the cross remains modestly lower at 1.06/1.04 over the next 6/12M horizon.