{kind=link}

Dollar surged overnight and remains firm in Asian session today. ECB’s dovish tapering is seen as a key factor driving the greenback higher. But more importantly, another step was taken forward as House passed Senate’s versions of the budget bill. That procedural path is now cleared to move on to US President Donald Trump’s tax cuts. Staying in the currency markets, commodity currencies remain the weakest ones for the week. Aussie’s selloff accelerated after CPI miss earlier this week and weighed further down by PPI miss today. Canadian Dollar remains weak as post cautious BoC statement selloff continues. Euro, while weak, is trading mixed only.

Dollar index confirms reversal

Dollar index’s strong break of 94.14 key resistance finally confirms medium term reversal. That is the pull back from 2016 high at 103.82 should have completed at 91.01, on bullish convergence condition in daily MACD. That also came after drawing support from 91.91/3 long term cluster support (38.2% retracement of 72.69, 2011 low, to 103.82, 2016 high) at 91.93. Near term outlook will now remain bullish as long as 93.47 support holds. Further rise should be seen to 38.2% retracement of 103.82 to 91.01 at 95.90 at least. There is prospect of hitting 61.8% retracement at 98.92 and above. But we’ll monitor the upside momentum to assess the chance later.

ECB’s dovish Tapering

ECB announced that it would begin in January 2018 to reduce the asset purchase size to 30 B euro per month. The program would last until September, "or beyond, if necessary". It added that stimulus measures would be implemented "in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim". In order not to let the market interpret the move as a trim in stimulus, President Mario Draghi called it "recalibration".

The accompanying statement affirmed that "if the outlook becomes less favorable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the APP in terms of size and/or duration". Moreover, the ECB announced that it would reinvest the principal payments from maturing securities "for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary". It would also continue to provide liquidity via fixed rate full allotment refi operations until at least the end of 2019.

More on ECB:

- ECB Begins Trimming Asset Purchase in 2018, Pledges to Expand/ Extend if Necessary

- ECB Tightening Remains Distant

- ECB Review: ECB Opts For ‘Lower-For-Longer’ QE Extension

- ‘Soft’ ECB Decision Triggers Modest Euro Setback

- ECB to Halve Monthly Pace of Asset Purchases to €30 Billion Starting in January 2018

- (ECB) Introductory Statement to the Press Conference

- (ECB) Monetary Policy Decisions

On the data front

Japan national CPI core was unchanged at 0.70% yoy in September, in line with consensus. Tokyo CPI core rose to 0.6% yoy in October, above expectation of 0.5% yoy. Australia PPI rose 0.2% qoq, 1.6% yoy in Q3.

US Q3 GDP is the main focus of the day ahead and is expected to show 2.6% annualized growth.

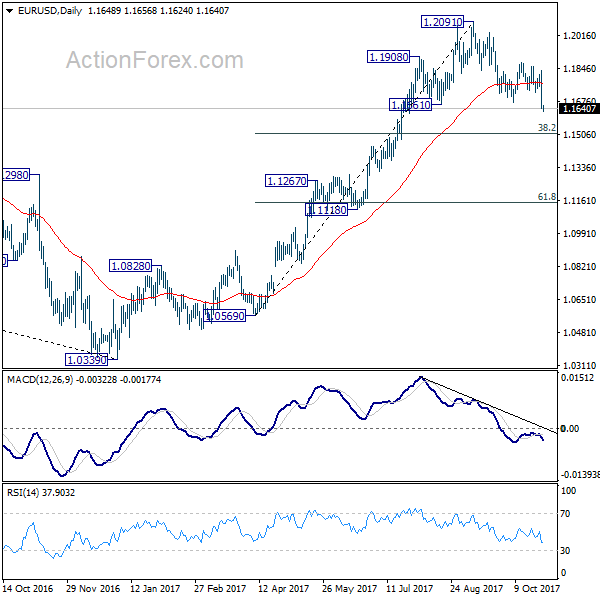

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1582; (P) 1.1709 (R1) 1.1779; More…

EUR/USD dives to as low as 1.1624 so far today. The break of 1.1669 support confirms resumption of whole fall from 1.2091. Intraday bias is back on the downside for 38.2% retracement of 1.0569 to 1.2091 at 1.1510 next. At this point, such decline is still viewed as a correction. Hence, we’d expect strong support from 1.1510 to bring rebound, at least during first attempt. However, firm break there will bring deeper decline to 61.8% retracement at 1.1150. ON the upside, above 1.1724 support turned resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 1.1879 resistance holds.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It’s expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we’d be cautious on strong resistance from 1.2516 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Sep | 0.70% | 0.70% | 0.70% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 0.60% | 0.50% | 0.50% | |

| 0:30 | AUD | PPI Q/Q Q3 | 0.20% | 0.40% | 0.50% | |

| 0:30 | AUD | PPI Y/Y Q3 | 1.60% | 1.70% | ||

| 6:00 | EUR | German Import Price Index M/M Sep | 0.9% | 0.50% | 0.00% | |

| 12:30 | USD | GDP (Annualized) Q3 A | 2.60% | 3.10% | ||

| 12:30 | USD | GDP Price Index Q3 A | 1.80% | 1.00% | ||

| 14:00 | USD | U. of Michigan Confidence Oct F | 101 | 101.1 |