{kind=link}

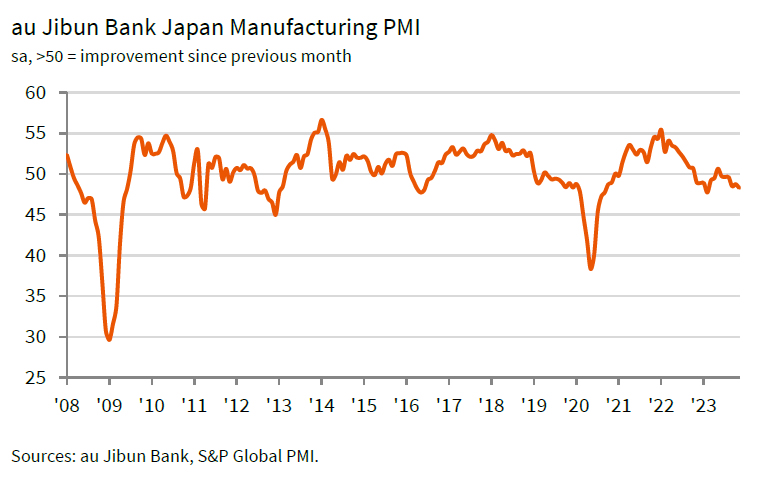

November saw Japan’s Manufacturing PMI finalized at 48.3, a slight decline from October’s 48.7. This figure, reported by S&P Global, indicates a continued contraction in the manufacturing sector, with more pronounced decreases in output and new order inflows. The PMI reaching its lowest since February signals a challenging phase for the sector, primarily due to weakened demand both domestically and internationally.

Usamah Bhatti of S&P Global Market Intelligence commented on the sector’s performance, noting, “The headline PMI slipped deeper into contraction territory, largely due to quicker deteriorations in output and new order inflows.” He identified weak customer demand across both domestic and international markets as key factors behind this downturn.

On the inflation front, although inflationary pressures remained high, there was a noticeable easing. Input cost inflation slowed down to a three-month low, and selling price inflation reduced to its softest since July 2021. This easing in inflation suggests some relief in cost pressures for manufacturers.

Despite the current contraction, Japanese manufacturers are holding onto a sense of optimism for the future. Bhatti emphasized this positive outlook, stating, “Manufacturers remained optimistic that muted demand and production conditions would lift over the coming year.” This confidence is underpinned by expectations of a boost in demand, spurred by new product launches, particularly in the semiconductor sector.