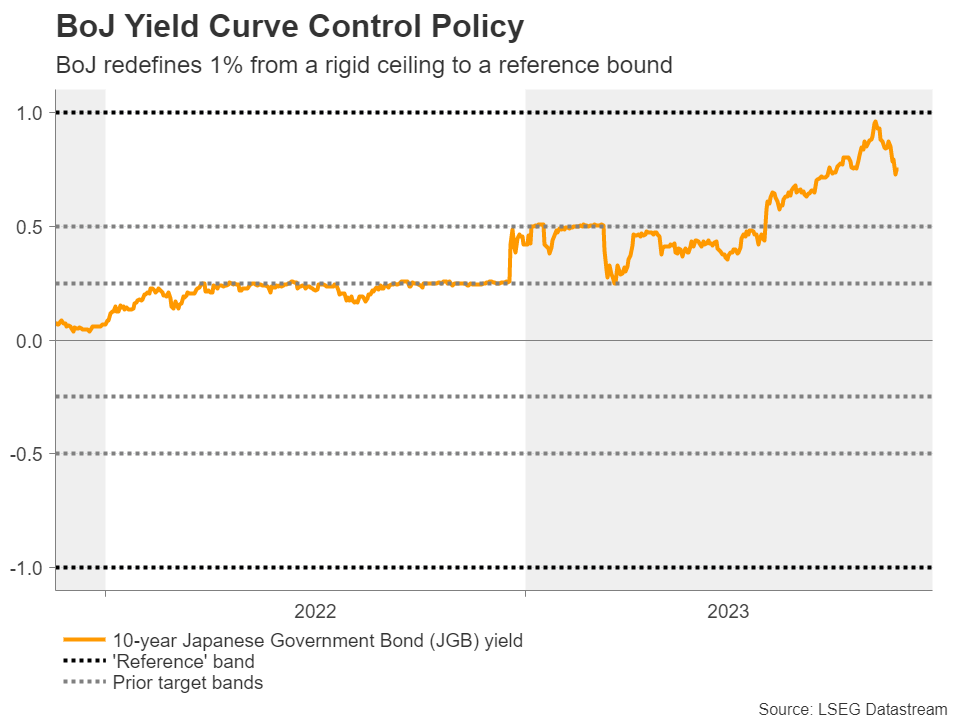

framework to allow 10-year Japanese government bond (JGB) yields to rise above 1%. However, they did not ditch the cap. They just redefined it from a rigid ceiling to a reference bound, which means that should officials judge it necessary, they will intervene in the bond market again. And indeed, this is what they did the day just after the decision.){kind=link}

- Weaker dollar helps the wounded yen recover some ground

- Focus turns to CPI numbers as traders speculate BoJ policy shift

- Accelerating inflation could bring the shift timing forward

- The data comes out on Thursday, at 23:30 GMT

Japan phases out its ultra-loose monetary policy

At their latest monetary policy decision, BoJ policymakers decided to adjust their yield curve control (YCC) framework to allow 10-year Japanese government bond (JGB) yields to rise above 1%. However, they did not ditch the cap. They just redefined it from a rigid ceiling to a reference bound, which means that should officials judge it necessary, they will intervene in the bond market again. And indeed, this is what they did the day just after the decision.

This disappointed investors as it suggested that, although the BoJ is phasing out its ultra-loose policy, the process could be much slower than anticipated. That’s why the yen tumbled in the aftermath of the decision and remained under pressure in the following days, with dollar/yen almost touching its October 2022 high of 151.94 on November 13.

Yen takes a breather as dollar tumbles

Nonetheless, it’s all been a retreat since then, despite Japan’s GDP data revealing that the economy contracted by more than anticipated in Q3, something that could complicate the BoJ’s plans for further policy normalization. Most likely, the slide in dollar/yen was the result of a broader dollar weakness and a pullback in Treasury yields following the lower-than-expected US CPI numbers that prompted market participants to price out any chance for another hike this year and to pencil in around 90bps worth of rate reductions by the Fed for next year.

Higher CPI rates could increase chances for more wage rises

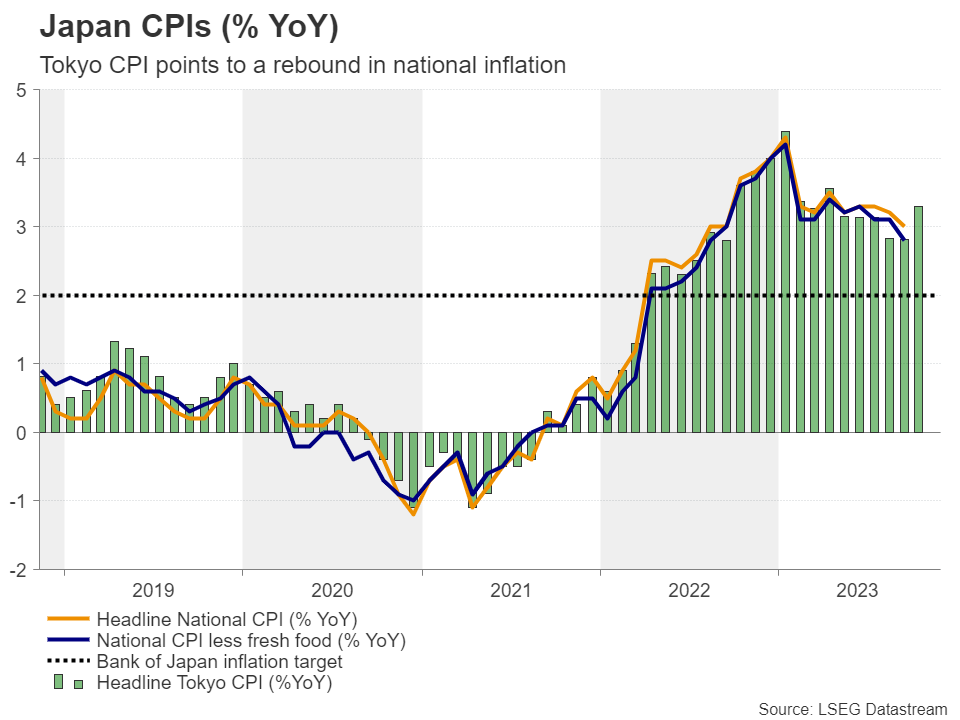

With all that in mind, Japan’s upcoming inflation data for October may be of extra importance for yen traders as they try to figure out when the BoJ may decide to abandon its YCC framework and take interest rates out of the negative territory.

There is no forecast available for the headline rate, but the core one is expected to have rebounded to 3.0% from 2.8%. The headline rate may have also rebounded, despite the slide in oil prices during the month, and that’s suggested by the acceleration in the Tokyo CPI for the month to 3.3% from 2.8%.

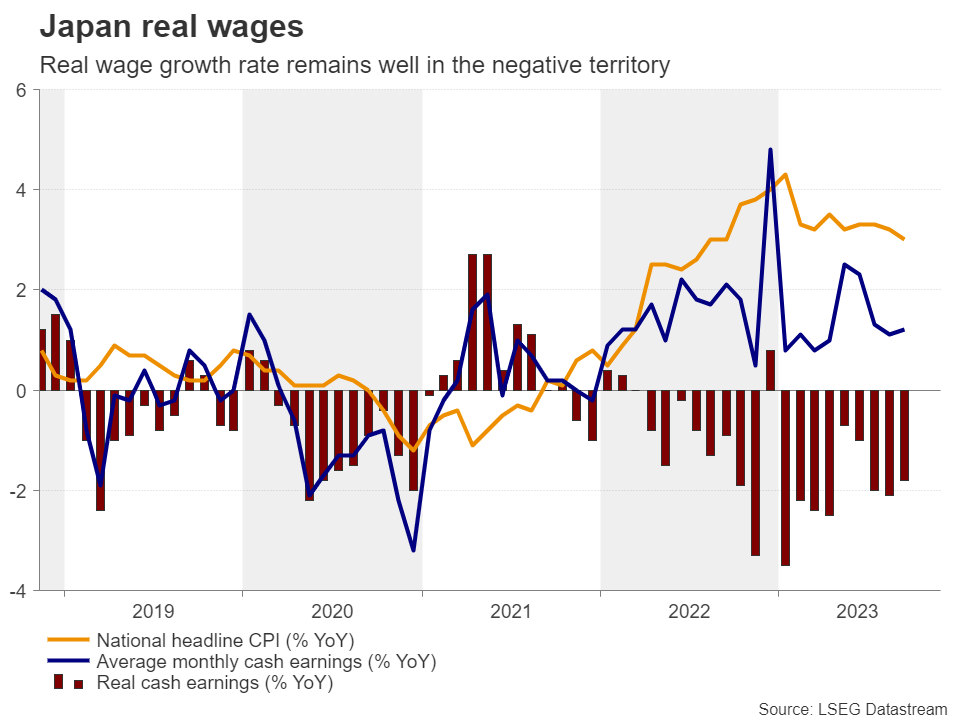

Accelerating price pressures could increase the likelihood for businesses and labor unions to agree on another round of strong pay hikes next year, especially after the BoJ revised up its inflation projections when it last met. With real wage growth staying well in the negative territory, despite improving somewhat, Japan’s largest industrial union will seek a 6% wage increase at next spring’s negotiations, according to a union official.

Pay hikes may allow the BoJ to exit ultra-loose policy

Thus, back-to-back pay hikes could allow the BoJ to eventually exit ultra-loose policy conditions sooner than previously thought. Speculation on that front could keep the yen supported and if the BoJ indeed decides to abandon its YCC policy and raise interest rates at a time when other central banks start to consider interest rate reductions, the currency may be poised to decisively reverse course against most of its major counterparts, as JBG yields rally when yields elsewhere continue to fall.

Yen may be preparing for a comeback

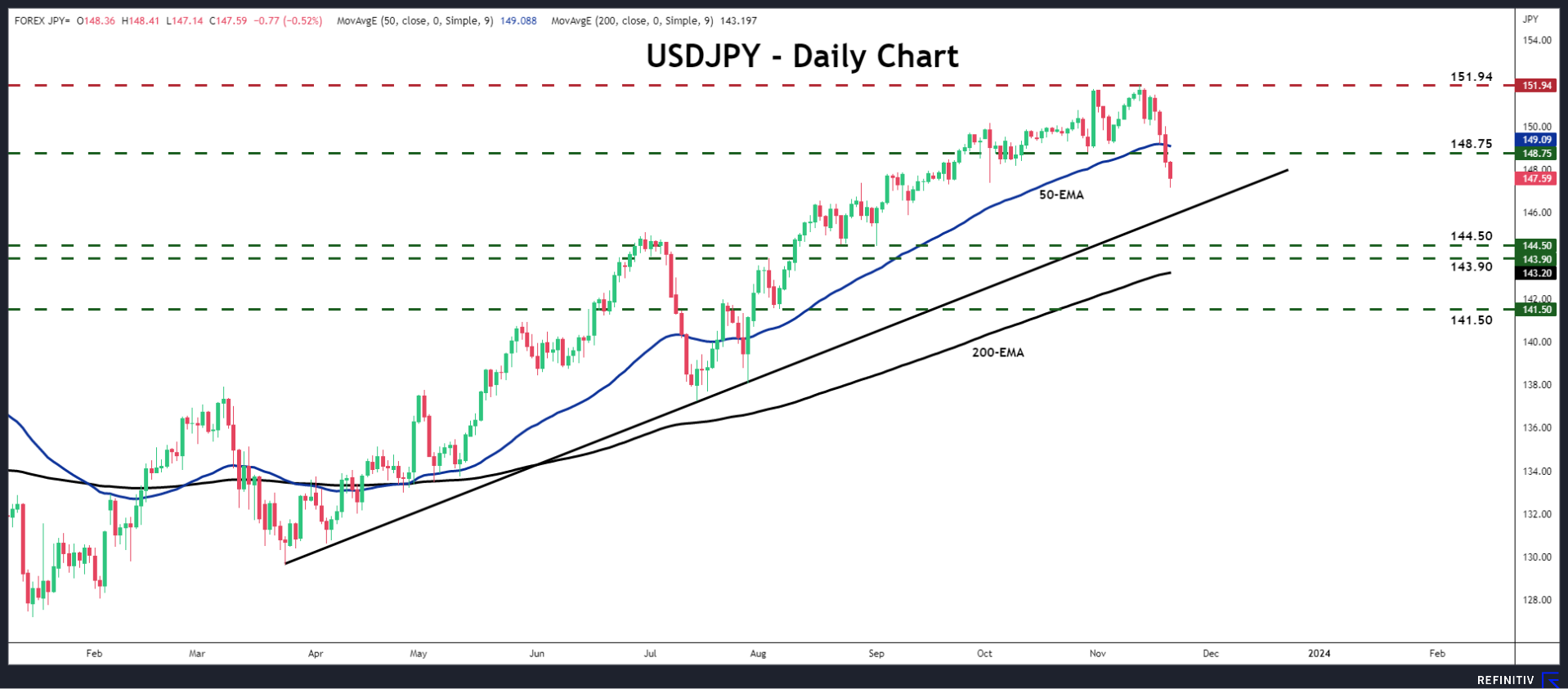

Dollar/yen has been in a steep decline since it nearly hit its 32-year high of 151.94 on November 13. However, it is still trading above the uptrend line drawn from the low of March 24, and above the key zone of 146.50. For a bearish reversal to start being examined, the pair may need to fall below the crossroads of those two hurdles, a move that could pave the way towards the 143.90 – 144.50 territory.

For the prevailing uptrend to resume, dollar/yen may need to break above the 151.94. This could be the case if investors get disappointed by a dovish BoJ that remains willing to intervene in the bond market even after abandoning YCC. Nonetheless, even in such a case, the risk of intervention by Japanese authorities could resurface and traders may be hesitant to initiate new long positions aiming for higher levels.