{kind=link}

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 2 November, which is in line with current market pricing.

- Overall, we expect the MPC to stick to its previous guidance emphasising the “higher for longer” approach.

- We expect a muted reaction in EUR/GBP but see risks as tilted to the topside.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 2 November. This is in line with current market pricing. We expect the vote split to be 6-3 with Greene, Haskel and Mann opting for an additional hike of 25bp and the rest of the MPC including the newest MPC member Sarah Breeden to vote for an unchanged decision. Note, this meeting will include updated projections and a press conference following the release of the statement.

Overall, we expect the MPC to stick to its previous guidance noting that the “current monetary policy stance is restrictive“, that they “will ensure that Bank Rate is sufficiently restrictive for sufficiently long” and that “further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures“. However, we expect the bar for further hikes down the road to increase adding a slight dovish tilt.

Since the last monetary policy decision in September, data releases have broadly been to the soft side. Wage growth for August was weaker than expected and broadly showing signs of easing in line with the REC and KPMG report, which “tends to lead changes in the official measure of annual wage growth” as noted by the BoE. While monthly GDP for August was overall in line with expectations at 0.2% m/m and 0.3% 3M/3M, growth will most likely be below the BoE forecast for Q3 from the August MPR at 0.4% q/q and the downward revision in September for 0.1% q/q. Likewise, retail sales for September remain weak with retail sales ex auto fuels at -1.0% m/m (-1.2% y/y). UK September inflation came in slightly higher than expected for both headline and core. In m/m SA terms, core inflation pressures remain muted at 0.04% while headline jumped higher to 0.5% on the back of an upward contribution from motor fuels. Importantly, inflation averaged 6.7% in Q3, which is lower than the BoE’s forecast of 6.9% y/y. PMI’s in September and October broadly remain in contractionary territory with all indices below 50 and continue to signal a gloomy growth outlook. Overall, with unemployment higher, inflation lower and GDP growth lower than expected by the BoE this supports our call of an unchanged decision and by extension the conclusion of the hiking cycle having been reached.

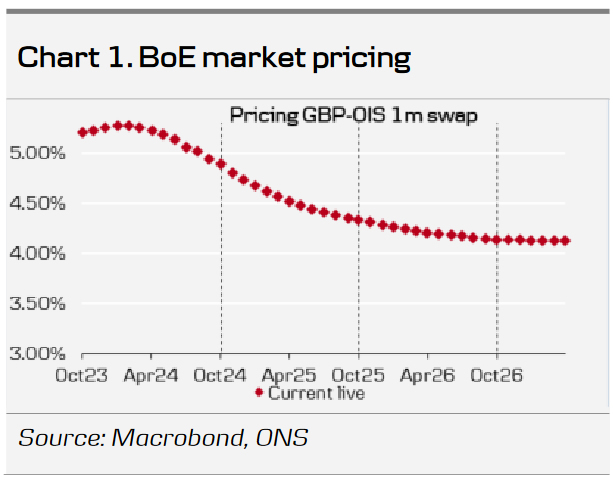

BoE call. We maintain our call that the BoE has delivered its final hike of this hiking cycle, which is in line with current market pricing. We expect the first rate cut of 25bp in June 2024 and subsequently a 25bp cut in the following quarters, totalling of 75bp of cuts for entire 2024.

FX. In our base case of an unchanged decision, we expect a muted reaction in EUR/GBP but on balance see risks as tilted to the topside. We anticipate the press conference to reiterate the MPC’s current guidance emphasising the “higher for longer” narrative and the data dependent approach. We continue to forecast EUR/GBP to move modestly higher the coming year to 0.89 on the UK economy performing relatively worse than the euro area.