{kind=link}

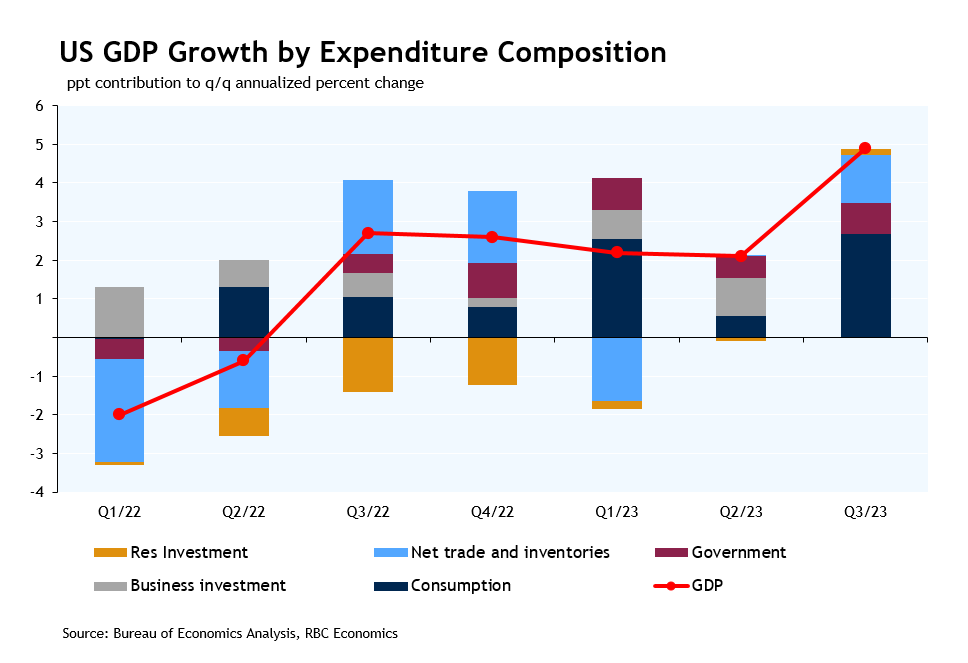

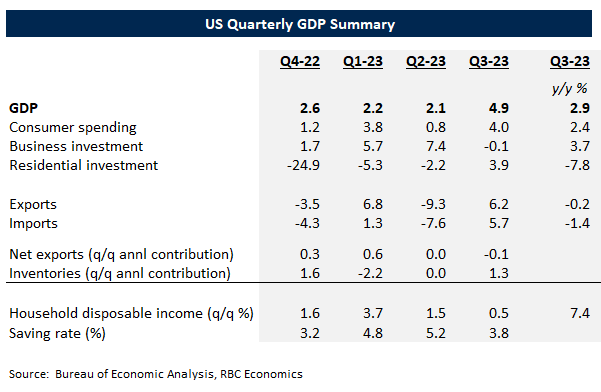

Third quarter U.S. GDP remained exceptionally strong, accelerating to an annualized rate of 4.9%. That was also the fifth consecutive increase since Q2/22 and largest since Q4/21.

A jump in the volatile inventory component accounted for about a quarter of the overall GDP gain. And residential investment surprised to the upside in Q3 (+3.9%), posting an increase after nine quarterly declines.

Consumer spending remained very strong, rising 4.0% in Q3, driven by broadly-based growth across goods (+4.8%) and services (+3.6%).

Still, household purchasing power showed further signs of deteriorating. Household after-inflation disposable income declined outright for the first time since Q3/23 and saving rate fell further below pre-pandemic levels. That is consistent with lower wage growth and slower hours worked growth over the summer.

Business investments on structures continued to climb higher, but at slower pace compared to the previous quarter, equipment investments declined by 3.8% in Q3. And net trade contributed little to growth.

Bottom line: Today’s GDP number indicates the U.S. economy still performed remarkably well in Q3, led by resilient household spending. Still, much of that strength came from another decline in remaining ‘excess’ savings accumulated during the pandemic – the household saving rate was still below pre-pandemic levels in Q3, and down from Q2. We continue to expect consumer spending to slow moving forward as higher interest rates and prices erode household purchasing power. Labour market conditions are also still exceptionally firm, but wage growth has ticked lower since June and lower job openings are flagging a pullback in hiring demand under the surface. We continue to expect the GDP growth backdrop to slow, and for that to keep the Federal Reserve from hiking interest rates further.