{kind=link}

Japanese Yen is registering broad gains in today’s Asian trading session, buttressed by the 10-year JGB yield which solidly remains above the 0.8% threshold. However, the yen’s advancement is notably limited, still lingering below this week’s high, which many attribute to a suspected, yet unverified, intervention. Japanese

The spotlight falls on Japanese Prime Minister Fumio Kishida, who, in his an address to Rengo, Japan’s premier labor organization, underscored the imperative of instigating “a wave of sustainable wage hikes.”

This stance resonates with BoJ’s consistent viewpoint that persistent wage growth is the linchpin to attaining inflation target. Meeting this condition is a foundational step for BoJ to move away from its ultra-accommodative monetary stance. For many analysts, this shift by BoJ is critical for reversing the current bearish trend in Yen.

In tandem with the Yen, Australian New Zealand Dollar are also making positive strides today. Presently, global market sentiments hint at a semblance of stabilization, reflected in the pullback of global benchmark yields and recovery in stock markets. However, this tentative shift in market mood awaits validation, especially with the looming US non-farm payroll data scheduled for release tomorrow. Meanwhile, Dollar, Euro, and Sterling seem to be trailing, whereas Swiss Franc and Canadian Dollar are displaying mixed performances.

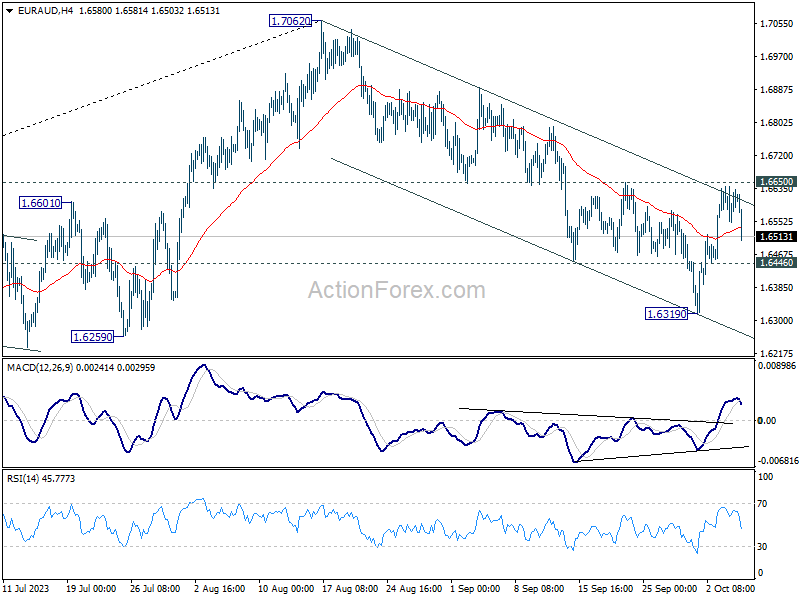

Technically, EUR/AUD dips notably after failing the break through 1.6650 resistance this week. The development keeps near term outlook bearish. Below 1.6446 minor support will likely resume whole decline from 1.7062 through 1.6319 support.

Should this EUR/AUD extended decline materialize, and be synchronized with decisive breaks below 0.8629 in EUR/GBP and 0.9617 in EUR/CHF, it could be indicative of a deep-rooted bearish momentum for the Euro, especially when analyzed in cross currency contexts.

In Asia, at the time of writing, Nikkei is up 1.66%. Hong Kong HSI is up 0.76%. Singapore Strait Times is up 0.75%. Japan 10-year JGB yield is down -0.003 at 0.805. Overnight, DOW rose 0.39%. S&P 500 rose 0.81%. NASDAQ rose 1.35%. 10-year yield dropped -0.067 to 4.735.

10% decline in oil prices raises questions on demand destruction

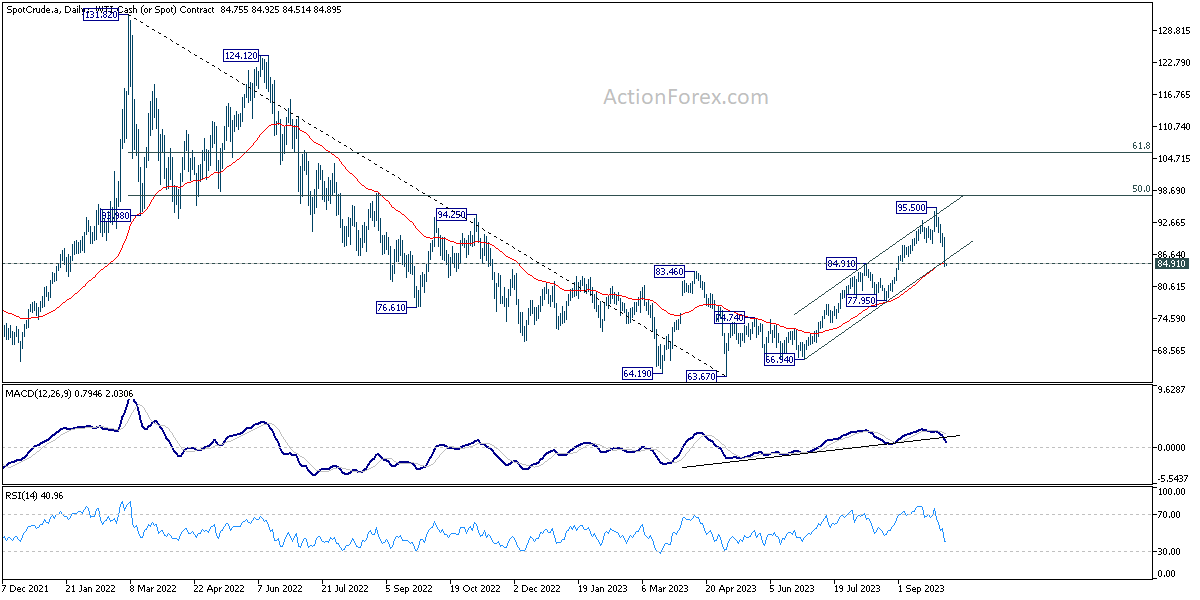

Oil prices took a significant dip overnight, with WTI now trading USD 10 beneath last week’s peak of 95.50. This decline is notably perplexing given the absence of a clear triggering event. OPEC+’s resolution to uphold output cuts is conventionally a precursor for a bullish response in the market. However, the rapid and profound dip has spurred conversations around the onset of demand destruction, provoked by the Q3 oil price spike.

In this week’s meeting, the OPEC+ ministerial panel opted for status quo, maintaining its existing oil output policy. Saudi Arabia pledged to persist with its voluntary cut of 1 million barrels per day through the end of 2023, while Russia committed to retaining its voluntary export reduction of 300k bpd until December’s end.

A note from JPMorgan’s commodity analysts titled “Demand destruction has begun (again)” highlighted that the repercussions of surging oil prices are re-emerging in the form of demand restraints in regions including US, Europe, and certain Emerging Markets.

The crux of global oil demand growth, anchored by China and India, is also showing signs of waning. China’s decision to utilize domestic crude inventories following the surge in oil prices is indicative of this trend.

In the US, gasoline consumption has plummeted to a 22-year low. The considerable 30% hike in fuel prices in Q3 has reportedly dampened demand, leading to an atypical decline of 223k barrels per day.

From a technical standpoint, WTI crude oil finds itself at a pivotal support juncture, which comprises the 84.91 resistance-turned-support and the 55 D EMA, currently pegged at 84.90. While a solid rebound from this position remains plausible, it’s expected to be restrained well below 95.50 high.

On the other hand, sustained break of 84.91 would confirm rejection by 50% retracement of 131.82 to 63.67 at 97.74. WTI could then be reversing whole rally from May’s low at 63.67, and risk falling further to 77.95 support.

Looking ahead

Germany trade balance, France industrial production and UK PMI construction will be released in European session. Later in the day, US will release jobless claims and trade balance. Canada will release trade balance and Ivey PMI.

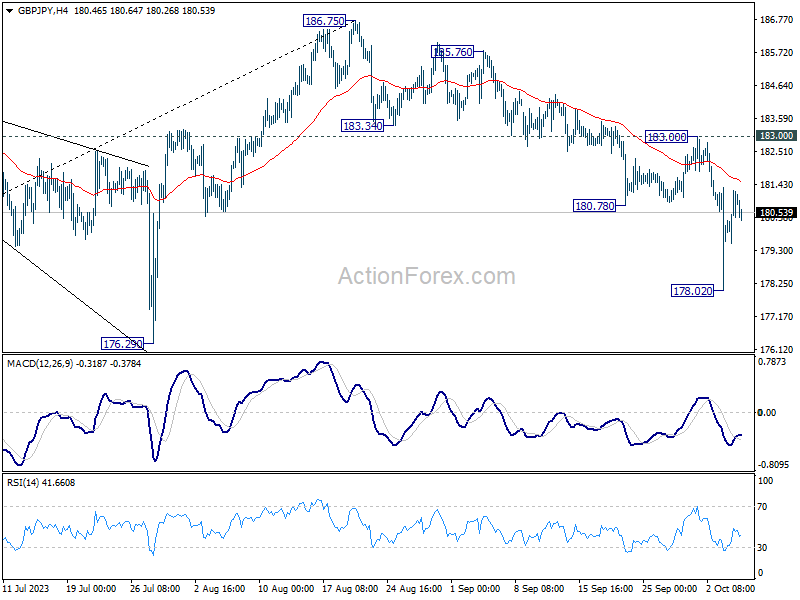

GBP/JPY Daily Outlook

Daily Pivots: (S1) 179.94; (P) 180.60; (R1) 181.63; More…

Intraday bias in GBP/JPY is turned neutral with the strong recovery from 178.02, and with 4H MACD crossed above signal line. Near term outlook stays bearish as long as 183.00 resistance holds. Break of 178.02 will resume the fall from 186.75 to 176.29 support. However, firm break of 183.00 will argue that the pull back has completed, and turn bias back to the upside.

In the bigger picture, fall from 186.75 is currently seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | 9.64B | 8.61B | 8.04B | 7.32B |

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | 14.3B | 15.9B | ||

| 06:45 | EUR | France Industrial Output M/M Aug | -0.40% | 0.80% | ||

| 08:30 | GBP | Construction PMI Sep | 49.9 | 50.8 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | 266.90% | |||

| 12:30 | USD | Initial Jobless Claims (Sep 29) | 211K | 204K | ||

| 12:30 | USD | Trade Balance (USD) Aug | -65.1B | -65.0B | ||

| 12:30 | CAD | Trade Balance (CAD) Aug | -1.4B | -1.0B | ||

| 14:00 | CAD | Ivey PMI Sep | 50.8 | 53.5 | ||

| 14:30 | USD | Natural Gas Storage | 97B | 90B |