{kind=link}

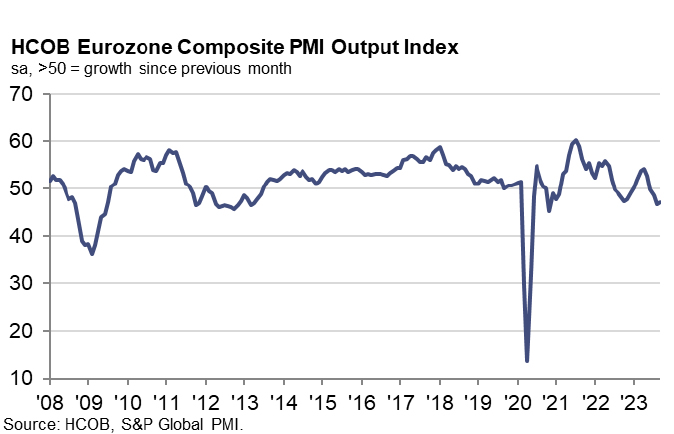

The latest Eurozone PMI Services data brings both a glimmer of optimism and a note of caution to an economic region. The finalized PMI Services for September stood at 48.7, marking an increment from August’s 47.9. Composite index also saw a marginal uplift to 47.2 from the previous month’s 46.7. While the numbers reflect an uptick, the fragility of the recovery becomes apparent when examining the country-specific data and underlying factors.

A look at the composite PMI output index reveals a contrasting scenario among the countries. Ireland tops the chart with a two-month low of 52.1, while France lags at a 34-month low of 44.1. Germany (46.4) and Italy (49.2), despite being on a multi-month high, are still not out of the woods, pointing towards a segmented recovery pattern.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, offers a balanced perspective. “The HCOB Composite PMI for the Eurozone did rebound a bit. However, we can’t jump on the hope train yet,” he cautioned. The declining new business, especially in powerhouse economies like Germany and France, underscores this sentiment, indicating a continual decline in outstanding business and a drop in business expectations.

In the corridors of ECB, where deliberations over the next interest rate decision are underway, the latest PMI data could act as a double-edged sword. The hawks find solace in the Input Price Index, propelled by wages and energy costs, marking a four-month pinnacle. In contrast, the doves might highlight the moderated pace at which service prices are increasing – the slowest since the summer of 2021.

“Prices are nevertheless still climbing the ladder rather fast, a weird twist when the economy is singing the blues,” de la Rubia noted.