{kind=link}

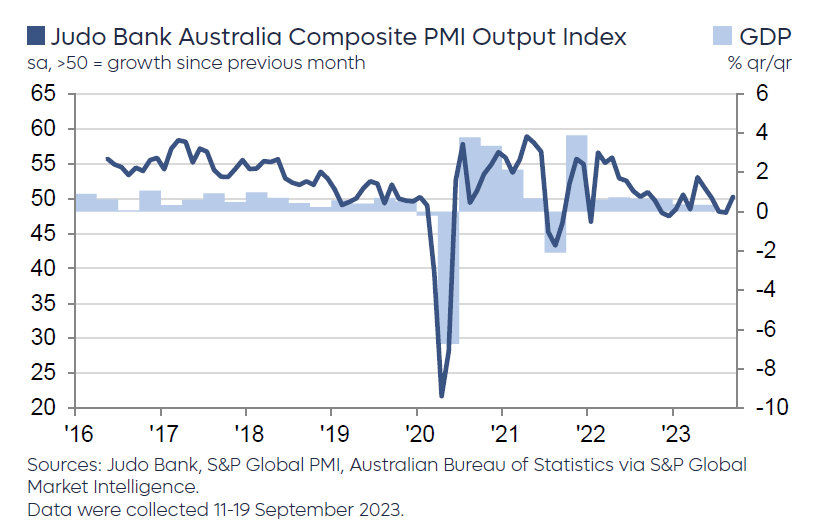

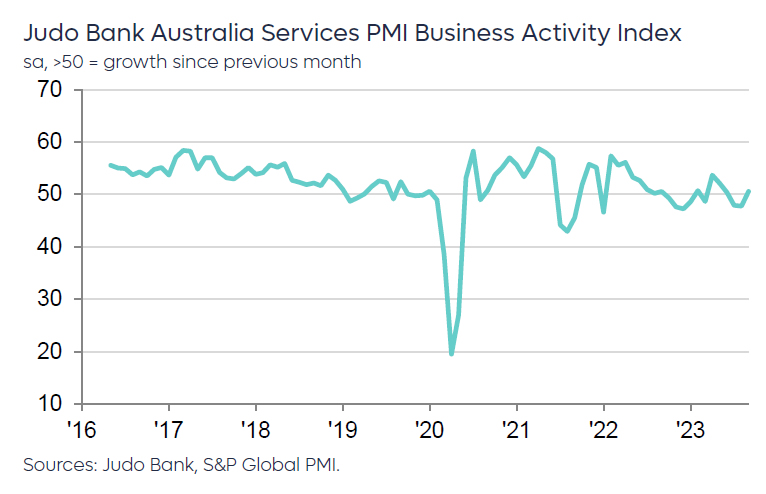

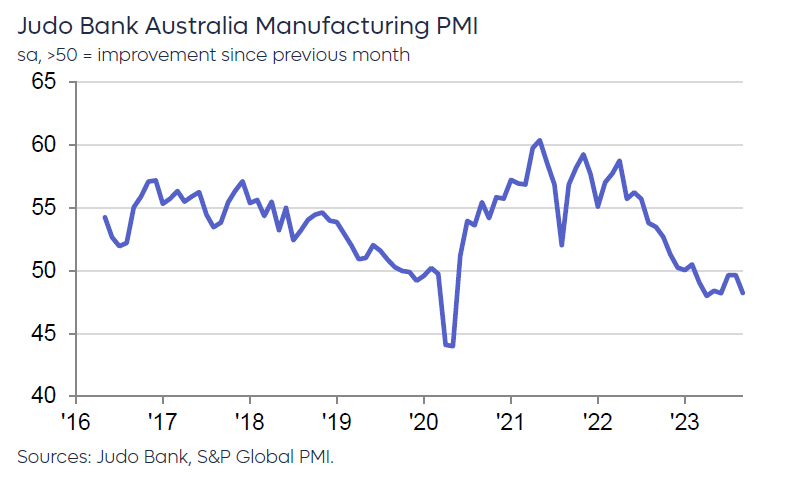

In September, Australia’s Manufacturing PMI slipped to a 3-month low, declining from 49.6 to 48.2. In contrast, PMI Services showcased resilience, rising from 47.8 to a 4-month high of 50.5. PMI Composite also surged from 48.0 to 50.2, a 4-month peak, signaling a return to expansion in the broader economy.

Warren Hogan, Chief Economic Advisor at Judo Bank,said that “demand in the economy is holding up, and business activity remains on a sound footing.” He further remarked that, contrary to some expectations, the present economic scenario isn’t about choosing between a “hard or soft landing.” Instead, he proposed that the real risk is of “no landing” for the economy.

Hogan further touched upon the inflation concerns that have been a pivotal discussion in financial circles. “The inflation indicators remain elevated at levels pointing to above-target CPI over the next 6-9 months,” he stated. He pointed out that input prices remained unchanged in September, hinting at continued cost pressures. However, the final prices index experienced a slight dip in the September flash report. Despite this marginal decline, Hogan suggested that “inflation over the second half of 2023 could be higher than desired.”

This latest PMI data follows a trend of stronger-than-predicted figures emerging from Australia in recent weeks. While this demonstrates economic stamina and persisting inflation, all eyes are on RBA’s next steps. Hogan postulates that the RBA Board, under leadership of the new Governor Michele Bullock, will likely adopt a patient stance. However, he doesn’t rule out further monetary tightening, possibly “in early November on Melbourne Cup day,” should the economic indicators not align with RBA’s projections of a slowdown.