, underpinned by decision of Saudi Arabia and Russia to extend its voluntarily output cuts in the fourth quarter.){kind=link}

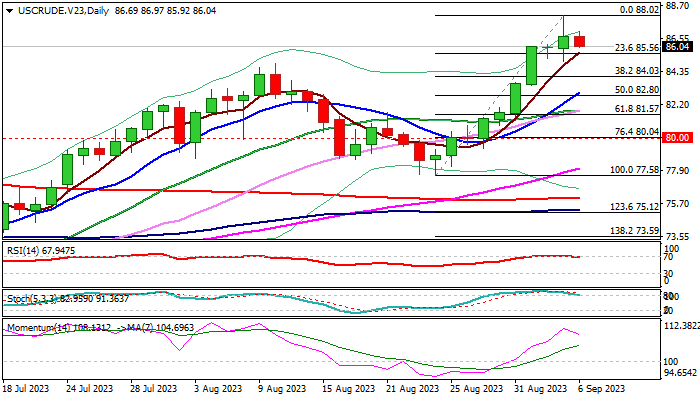

WTI oil price edged lower in early Wednesday’s trading, after advancing 0.9% on Tuesday and hitting new 2023 high ($88.02), underpinned by decision of Saudi Arabia and Russia to extend its voluntarily output cuts in the fourth quarter.

The decision for extended supply reduction is expected to keep the oil market tight, although the positive impact on the price was partially offset by signals that two key oil producers will be reviewing its decision on a monthly basis.

Persisting demand concerns also weigh on oil price as recent weaker than expected global economic data warn that the EU and US economies feel stronger negative impact from high borrowing cost, while economic growth in China, world’s biggest oil importer, is still to gain desired pace in post-Covid recovery.

Short-term picture is overall positive, but overbought conditions on daily chart (14-d momentum and RSI are about to reverse from overbought territory) is likely to trigger some profit taking and push the price lower.

Tuesday’s daily candle with long both shadows generated initial indecision signal, which may add to the scenario of pullback.

Dips should ideally find footstep above $84.00 zone (Fibo 38.2% of $77.58/$88.02 upleg) to mark a healthy condition ahead of fresh push higher, with deeper dips not to exceed $82.80 (50% retracement / rising 10DMA) to keep larger bulls intact, for push through the recent top and acceleration towards psychological $90 barrier.

Conversely, violation of $82.80 pivot would risk deeper correction and expose strong supports at $80.00 (psychological) and $78.70 (top of rising and thickening daily cloud).

Release of US crude inventories reports (API due today and EIA on Wednesday) are also expected to provide fresh signals.

Res: 88.02; 90.00; 93.72; 94.53.

Sup: 85.56; 85.00; 84.03; 82.80.