, likely keeping them on hold for the third straight month. One reason for the RBA’s increased caution lately is weaker economic growth. GDP data due on Wednesday (01:30 GMT) will reveal whether growth remained sluggish or improved in the second quarter. The Australian dollar is vulnerable to further losses amid mounting worries about China on top of a less hawkish RBA.){kind=link}

The Reserve Bank of Australia will decide on interest rates on Tuesday (04:30 GMT), likely keeping them on hold for the third straight month. One reason for the RBA’s increased caution lately is weaker economic growth. GDP data due on Wednesday (01:30 GMT) will reveal whether growth remained sluggish or improved in the second quarter. The Australian dollar is vulnerable to further losses amid mounting worries about China on top of a less hawkish RBA.

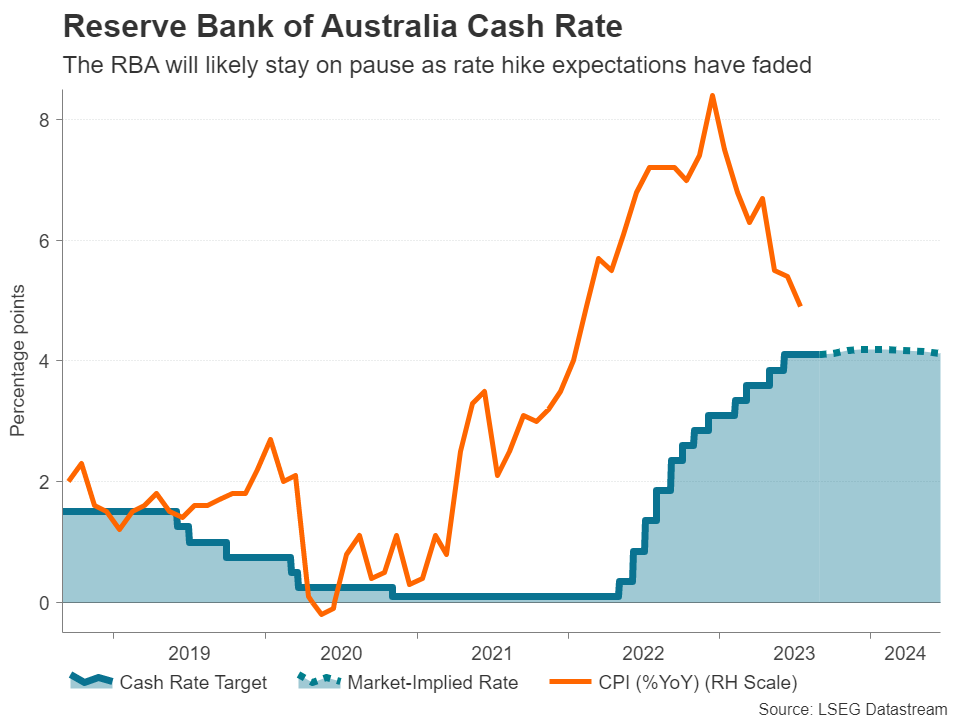

Inflation threat is receding

As policymakers continue their battle against high inflation, there is good news and bad news for the Australian economy. The good news is that inflation is well on the way down. The consumer price index eased to 4.9% y/y in July – the lowest since February 2022. Underlying measures of inflation are also falling, with weighted CPI declining from 5.4% to 4.9% y/y. In a further encouraging sign, wage growth appears to have peaked.

For a central bank that is highly conscious about the cumulative effects from the 400-bps-worth of tightening that have yet to be felt, leaving the cash rate unchanged in September seems like a sensible move. Analysts and markets both concur, and no change is almost fully priced in by investors.

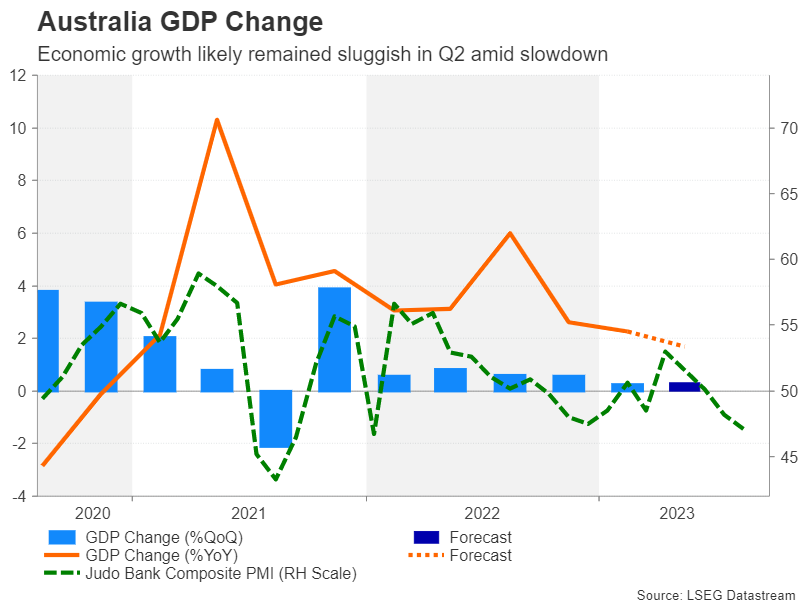

Is Australia headed for recession?

The bad news, however, is that growth has slowed substantially this year amid a number of headwinds, higher rates being the main one. The housing market was the first to feel the heat from rising borrowing costs and was a significant drag on growth in 2022. However, this year, higher rates are taking their toll on consumption, as households are being forced to rein in their spending.

But that’s not the only trouble spot. Exports have slumped in the past few months as China’s economy has hit a stumbling block. China is Australia’s largest trading partner so any slowdown there would have a material impact on local exporters.

GDP growth moderated to just 0.2% q/q in the first three months of the year and it likely quickened slightly to 0.3% in the second quarter. But if the S&P Global PMI surveys are any indication, a worse figure is possible and the economy could be headed for a small contraction in Q3.

Some green shoots

However, even if a poor GDP reading adds to the slew of data supporting a prolonged pause by the RBA, that might be an assumption too far as there are some positive developments as well. The labour market remains tight even if there has been a slight cooling off lately, and that should support consumption. There are already some early signs that consumer spending is picking up.

What is more incredible is that house prices have started to rebound again, countering the argument that further rate hikes could cause a crash in the housing market.

Moreover, all the evidence at the moment is that inflation globally is proving to be a lot stickier than anticipated so even if the economy continues to lose steam, the RBA may have to provide an extra nudge for CPI to fall sustainably within its 2-3% target band. Hence, there’s a risk some investors are too readily dismissing policymakers’ warnings about the need for further rate hikes. After all, the outlook could easily change if the economic situation in China starts to improve.

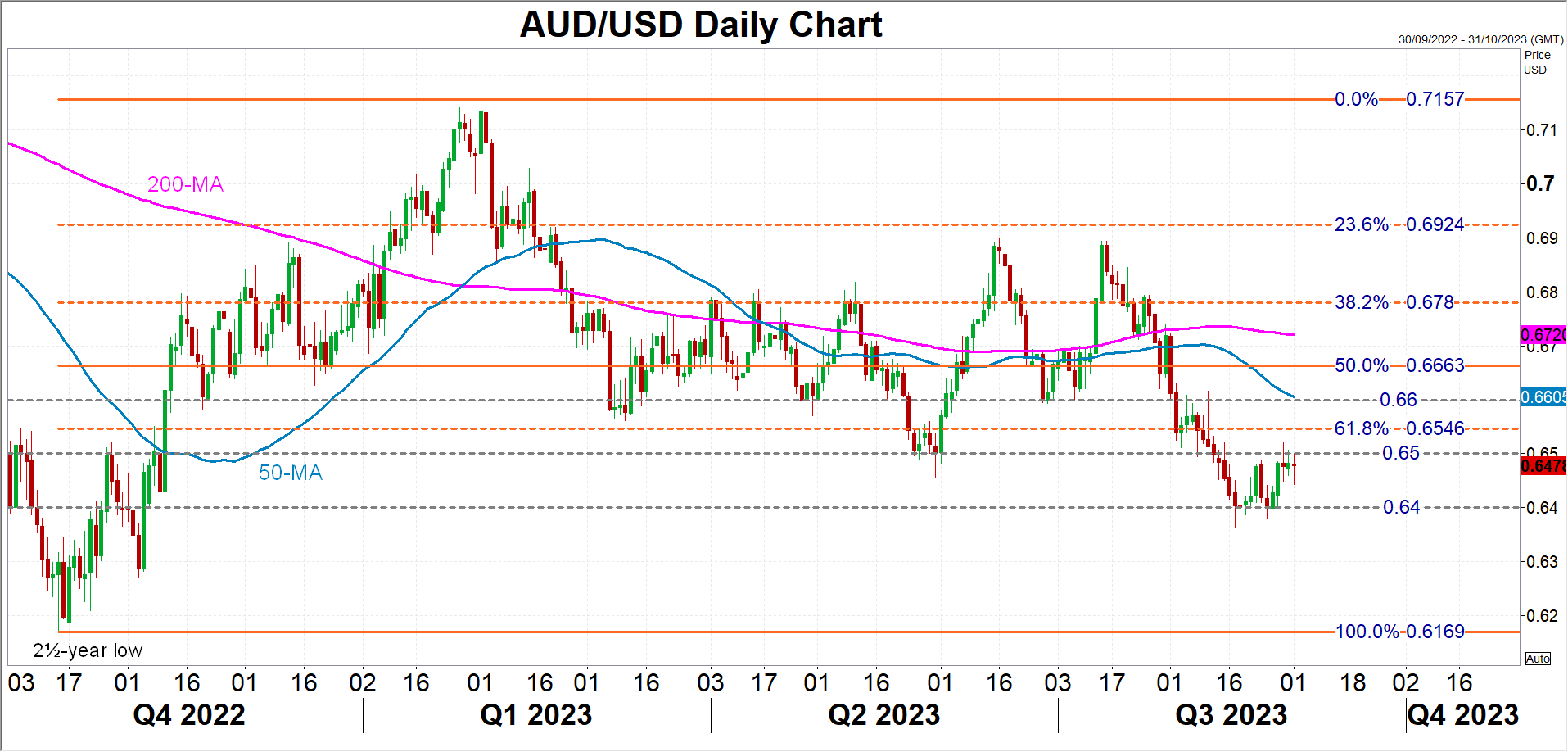

Aussie slide may have more to go

This applies to the Australian dollar too. While a relatively more hawkish Fed and stronger American economy go some way in explaining the aussie’s weakness against the US dollar this year, the main factor behind the extent of this underperformance is all the gloom surrounding China in recent months.

In the near term, however, a neutral RBA won’t be enough to stem the aussie’s losses and a breach of the October 2022 low of $0.6169 is possible. But in the event that the RBA stresses the upside risks to inflation or the incoming US data keeps surprising to the downside, the aussie could rebound towards its 50-day moving average just above the $0.66 level.