{kind=link}

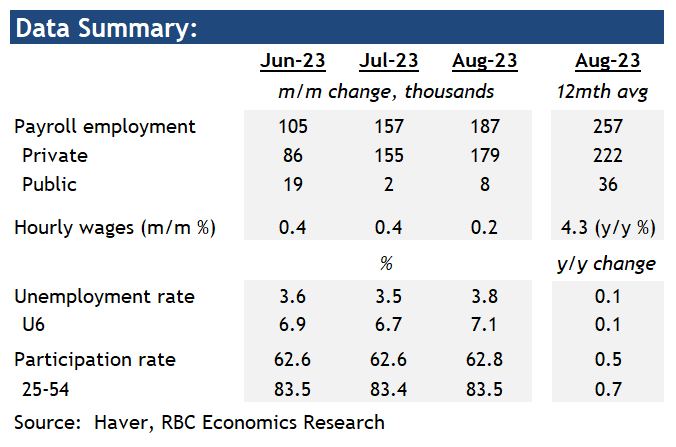

Job growth in the U.S. remained firm in August at 187k, following downwardly revised 157k and 105k increases in July and June.

The majority of employment growth was again accounted for by services sectors. Health care and leisure and hospitality added the most jobs, by 71k and 40k, respectively in August. Transportation and warehousing continued to show weakness, losing 34k jobs in August. That was also the 5th decline out of 8 months this year.

Separately released household survey showed the unemployment rate rising higher to 3.8% in August from 3.5% in July. The increase was mostly driven by a rise in the participation rate not being offset by higher employment. Labour force participation rate rose to 62.8% in August.

Other indicators have continued to point to slowing labour demand. Job openings in July dropped to the lowest level in almost two and a half years. Quits rates in the U.S. also continued to decline, suggesting that tight labour market conditions are continuing to unwind.

Wage growth is persisting at higher levels, but the 0.2% increase in average hourly earnings in August was relatively small and the year-over-year rate of growth ticked down to 4.3% from 4.4% in July.

Bottom line: The employment growth in August is still historically strong and the increase in the unemployment rate could still be partially reversed in coming months. But signs of flagging labour demand elsewhere mean we can expect conditions to continue to cool. That outlook, together with easing inflation trends should be enough to keep Fed on a “hopeful” pause. We expect the Fed Funds to be held at current range (5.25% – 5.5%) throughout the remainder of 2023.