{kind=link}

Dollar’s attempted rally quickly reversed overnight, following disappointing consumer confidence data. Interestingly, equities gained on what some market participants are calling a “bad news is good news” factor. The logic here is that Fed is now less likely to raise interest rates again this year, thereby giving stocks a lift, as Treasury yields also took a dip. However, it’s worth noting that there hasn’t been a sustained selloff in the greenback as market attention is largely focused on the impending non-farm payroll and PCE inflation data due this Friday. Meanwhile, today’s ADP private job data might still trigger some market reactions.

Australian Dollar is emerging as the week’s best performer for now, largely ignoring the lower-than-expected monthly CPI data. It is followed closely by the New Zealand Dollar, buoyed by an overall positive risk sentiment. Euro and Swiss Franc have also firmed up, benefiting from Dollar’s momentary stumble. For now, Dollar, Yen, and Canadian Dollar are the laggards in currency markets.

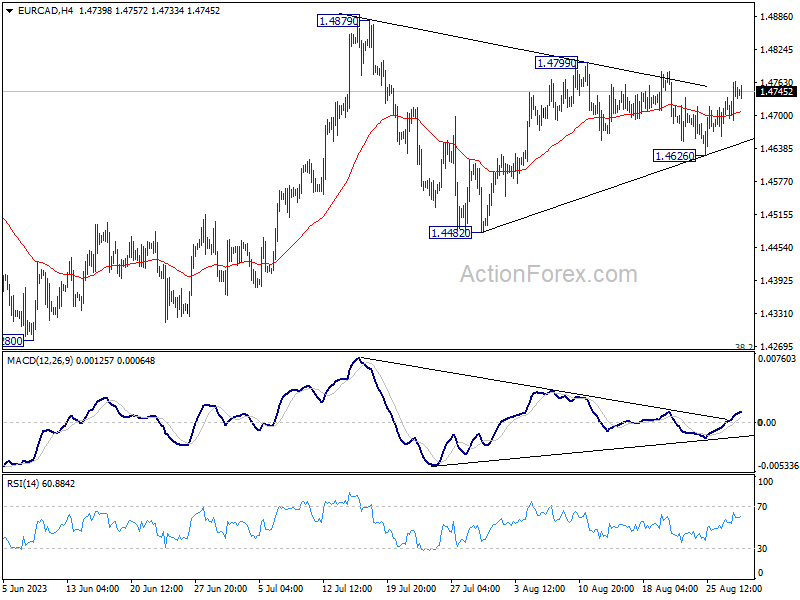

Technically, EUR/CAD is worth a watch in the next few days, with focus on 1.4799 resistance. Firm break there would argue that corrective pattern from 1.4879 has completed, and further rally could then be seen through 1.4879 to resume whole rise from 1.4280. On the other hand, break of 1.4626 support will extend the pattern from 1.4879 with another fall through 1.4482. The next move would be a reaction to either Eurozone CPI flash or Canada GDP, or both.

In Asia, at the time of writing, Nikkei rose 0.33%. Hong Kong HSI is up 0.37%. China Shanghai SSE is up 0.07%. Singapore Strait Times is up 0.16%. Japan 10-year JGB yield rose 0.011 to 0.658. Overnight, DOW rose 0.85%. S&P 500 rose 1.45%. NASDAQ rose 1.74%. 10 year yield dropped -0.090 to 4.122.

Australian CPI eases more than expected to 4.9% in July

Australia’s monthly CPI for July registered a deeper than expected slowdown, easing from 5.4% yoy to 4.9% yoy. Analysts had forecasted a milder decline to 5.2% yoy. The underlying inflation measures also indicated a deceleration. CPI excluding volatile items such as holiday travel came in at 5.8% yoy, down from 6.1% yoy. The trimmed mean CPI, which is often regarded as a more accurate reflection of inflationary pressures, slowed from 6.0% yoy to 5.6% yoy.

A closer look at the inflation contributors reveals a mixed picture. Housing costs remained a significant upward pressure, climbing 7.3% on an annual basis. Food and non-alcoholic beverages followed closely, rising by 5.6% yoy. However, this was offset by substantial price falls in other areas. Automotive fuel costs dropped by -7.6%, while fruit and vegetable prices declined by -5.4%, thus tempering the overall July increase.

The latest CPI data comes on the heels of yesterday’s hawkish comments from incoming RBA Governor Michele Bullock, who emphasized that her first priority is still to maintain a focus on bringing inflation back down to target. Today’s lower-than-expected inflation figures might lend some flexibility to RBA’s policy approach, but with sectors like housing and food still exhibiting strong price pressures, the central bank’s task appears far from straightforward.

BoJ’s Tamura eyes next Q1 for decisive inflation data for policy shifts

BoJ board member Naoki Tamura offered insights into the timeline for potentially phasing out the central bank’s ultra-accommodative stance. he signaled that by the first quarter of 2024, BoJ could gather sufficient data to evaluate whether the 2% inflation target could be sustainably achieved.

“It’s appropriate at this stage to sustain monetary easing, and earnestly scrutinize wage and price developments,” Tamura said, adding that he is hopeful for “further clarity” on the inflation target “around January through March next year” through wage and price data available by that time.

Tamura anticipates that Japan’s inflation could slow down for the time being, only to moderately accelerate later. This coincides with his expectation of high wage growth in the next year’s spring wage negotiations.

Tamura emphasized that the “biggest key to monetary policy outlook is whether Japan achieves a positive cycle of rising wages and inflation.”

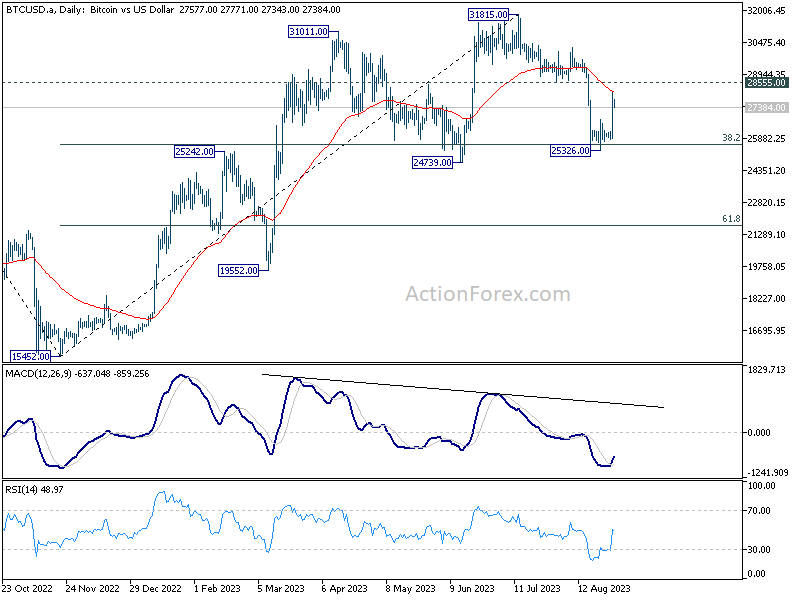

Bitcoin soars after Grayscale’s legal win, now pressing 55 D EMA

In a notable development for cryptocurrency enthusiasts and investors, Bitcoin experienced a significant surge overnight, pulling other cryptocurrencies higher in its wake. This rally was triggered by Grayscale’s key legal victory against the US Securities and Exchange Commission in its bid to launch a Bitcoin exchange-traded fund. The favorable ruling could pave the way for the SEC’s approval of other Bitcoin ETF applications, thereby providing the cryptocurrency industry with access to a new pool of retail investor capital.

From a technical perspective, Bitcoin’s strong bounce suggests that cluster support zone around 25k is defended well for now. This support zone comprises various key levels, including 24739 support, 25242 resistance-turned-support, and more importantly 38.2% retracement of 15452 to 31815 at 25564.

The overnight activity implies that recent price actions from 31815 may simply represent sideways consolidation rather than a bearish trend. It suggests that the medium-term rise from 15452 isn’t over just yet.

However, to firmly establish this bullish case, Bitcoin still has hurdles to overcome in the near term. Specifically, it will need to break through the 55 D EMA, currently at 28173, and 28555 support-turned-resistance.

Looking ahead

Swiss will release KOF economic barometer and Credit Suisse economic expectations. Eurozone will release economic sentiment indicator. Germany will release CPI flash.

Later in the day, US will publish ADP job, goods trade balance, pending home sales and Q2 GDP revision.

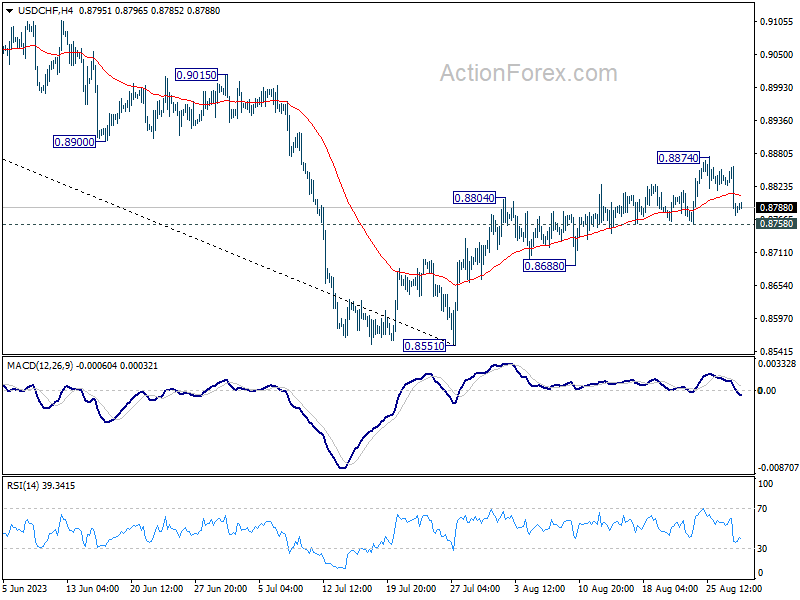

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8753; (P) 0.8806; (R1) 0.8837; More….

USD/CHF’s retreat from 0.8874 extended lower but stays above 0.8758 support. Intraday bias remains neutral first and further rally remains in favor to continue. On the upside, break of 0.8874 will resume the rise from 0.8551 to 0.9146 cluster resistance next. Nevertheless, break of 0.8758 will turn bias back to the downside for 0.8688 support and below.

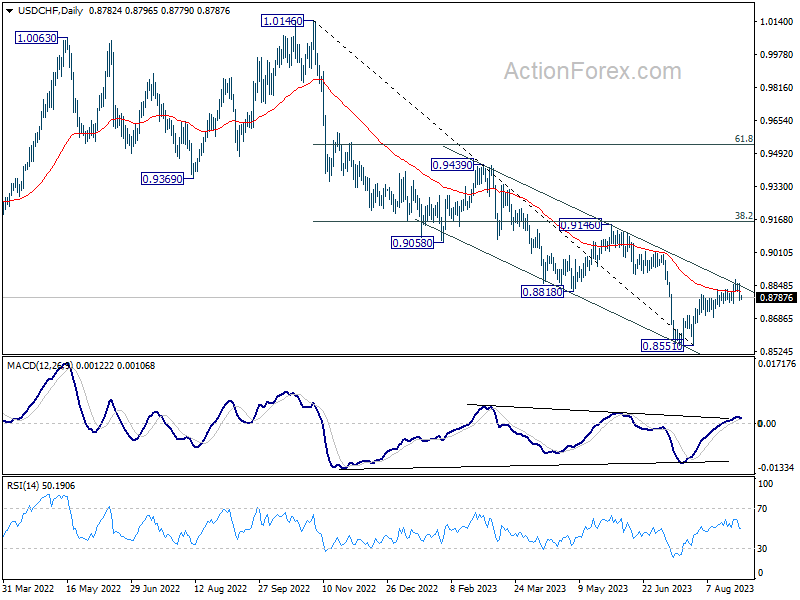

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt. Nevertheless, medium term outlook is neutral at best as long as 0.8551 holds, until further developments.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jul | -5.20% | 3.50% | 3.40% | |

| 01:30 | AUD | Monthly CPI Y/Y Jul | 4.90% | 5.20% | 5.40% | |

| 01:30 | AUD | Building Permits M/M Jul | -8.10% | -0.50% | -7.70% | -7.90% |

| 05:00 | JPY | Consumer Confidence Index Aug | 36.2 | 37.5 | 37.1 | |

| 06:00 | EUR | Germany Import Price Index M/M Jul | -0.60% | -0.20% | -1.60% | |

| 07:00 | CHF | KOF Economic Barometer Aug | 91.3 | 92.2 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Aug | -32.6 | |||

| 08:30 | GBP | Mortgage Approvals Jul | 52K | 55K | ||

| 08:30 | GBP | M4 Money Supply M/M Jul | 0.10% | -0.10% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | 93.9 | 94.5 | ||

| 09:00 | EUR | Eurozone Services Sentiment Aug | 4.2 | 5.7 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Aug | -9.8 | -9.4 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | -16 | -16 | ||

| 12:00 | EUR | Germany CPI M/M Aug P | 0.30% | 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Aug P | 6.00% | 6.20% | ||

| 12:15 | USD | ADP Employment Change Aug | 205K | 324K | ||

| 12:30 | USD | GDP Annualized Q2 P | 2.40% | 2.40% | ||

| 12:30 | USD | GDP Price Index Q2 P | 2.20% | 2.20% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jul P | -90.0B | -87.8B | ||

| 12:30 | USD | Wholesale Inventories Jul P | 0.20% | -0.50% | ||

| 14:00 | USD | Pending Home Sales M/M Jul | -0.40% | 0.30% | ||

| 14:30 | USD | Crude Oil Inventories | -2.2M | -6.1M |