{kind=link}

Summary

- Fed Chair Jerome Powell reiterated the FOMC’s commitment to bring inflation down to 2% during his speech in Jackson Hole, WY today. He stated that “two percent is and will remain our inflation target.”

- In order to bring inflation back to target, Powell said that a period of below-trend economic growth will be required. Consequently, the stance of monetary policy will need to remain restrictive for the foreseeable future. The Fed Chair also indicated that the FOMC “is prepared to raise rates further if appropriate.”

- But the FOMC is facing a number of uncertainties at this juncture. Consequently, Fed policymakers will need to be “agile.” In other words, the FOMC is in data dependency mode for the foreseeable future.

- We believe there is a high bar for the FOMC to raise rates at its September 20 meeting. We forecast the Committee will remain on hold at subsequent meetings, but we acknowledge the risk of further tightening if economic growth does not slow to a below-trend rate and/or inflation remains unacceptably high.

Fed Committed to 2% Inflation Target

As has become customary for the Chair of the Federal Reserve, Jerome Powell kicked off the Kansas City Fed’s annual Jackson Hole Economic Policy Symposium today with a speech entitled “Inflation: Progress and the Path Ahead.” The speech that Powell delivered last year at Jackson Hole, which we discussed in our Weekly Economic and Financial Commentary on August 26, 2022, was short and to the point. In the five-page speech that he delivered last year, Powell essentially said that the FOMC would do everything needed to ensure that inflation would return to the Committee’s 2% target. The FOMC had already raised rates by 225 bps when Powell delivered his speech last year. It would go on to hike by another 300 bps in the subsequent 12 months.

The mission at Jackson Hole last year was simple. Powell needed to convince market participants that the FOMC was committed to bringing down inflation, and his concise and direct remarks largely succeeded in that regard. Because inflation remains above target today, the Fed Chair apparently wanted to send a message that the FOMC remains committed to bringing inflation down. He reiterated last year’s mantra at the very beginning of his remarks today by saying “it is the Fed’s job to bring inflation down to our two percent goal, and we will do so.” In case the point was missed, he closed by saying “restoring price stability is essential,” and “we will keep at it until the job is done.” Powell also threw cold water on any expectations that the FOMC might tweak its inflation target higher by stating “two percent is and will remain our inflation target.”

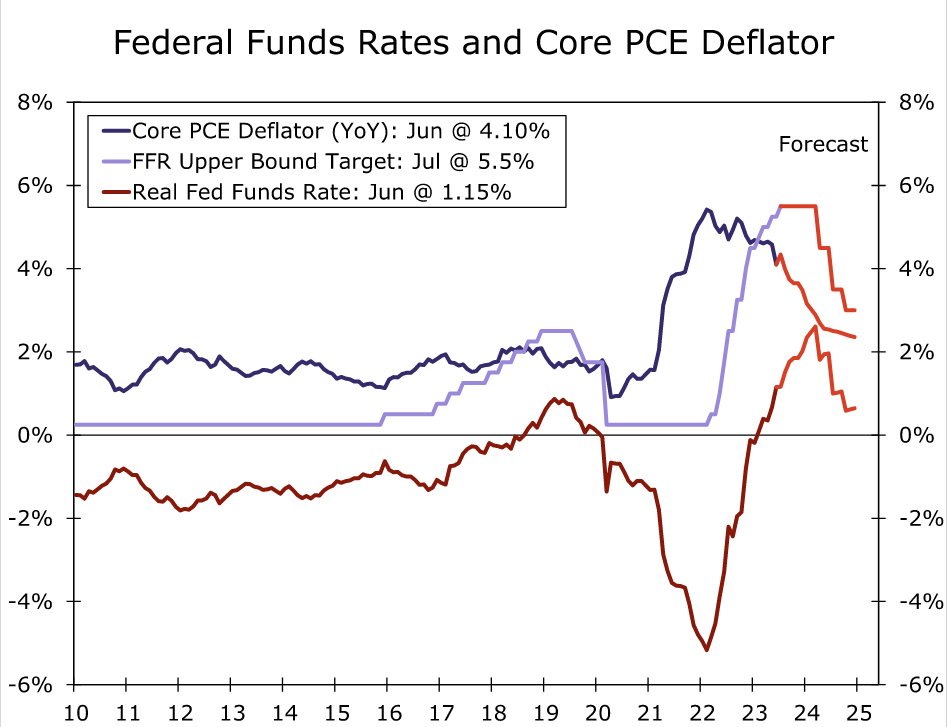

Although Powell welcomed the decline in the rate of inflation that has occurred since last year’s speech—the year-over-year rate of core PCE inflation has receded gradually from its peak of 5.4% in February 2022 to 4.1% currently—he indicated that “it remains too high.” In order to bring inflation back to the Committee’s 2% target, the Fed Chair said that the labor market must become less tight. Powell went on to state that “a period of below-trend economic growth” will be needed to bring inflation sustainably back to target. Consequently, the stance of monetary policy, which Powell characterized as “restrictive” at present, will need to remain so for the foreseeable future. In short, the Fed likely will not be cutting rates anytime soon. Indeed, Powell indicated that the FOMC “is prepared to raise rates further if appropriate.”

Uncertainties Cloud the Outlook for Monetary Policy

But Powell also highlighted in this year’s speech the uncertainties the FOMC faces in achieving its goal. He noted that “it is challenging to know in real time” when a sufficiently restrictive stance of policy has been achieved, and he said “that assessment is further complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation.” Because there is a risk of doing too much (i.e., tanking the economy) as well as a risk of doing too little (i.e., allowing high inflation to become entrenched), Powell said that policymaking will need to be “agile” going forward. In short, the FOMC is in data dependency mode at present. Incoming economic data will determine whether the Committee tightens policy further or whether it decides to remain on hold. But given the current state of play—the real economy appears to be holding up rather well and inflation remains well above target—don’t expect monetary easing anytime soon.

Our assessment is that there is a high bar for the FOMC to raise rates at its next policy meeting on September 20. Patrick Harker, the president of the Federal Reserve Bank of Philadelphia and a voting member of the FOMC this year, said yesterday that the Committee has “probably done enough” in terms of monetary tightening. It appears that there are a number of other Committee members who also think that further tightening is not warranted. If the macro U.S. economy evolves largely in line with our forecast in coming months, then we think the FOMC will remain on hold at its November 1 meeting as well. That said, we acknowledge the risk that the Committee could tighten further at future meetings if economic growth does not slow to a below-trend rate and/or inflation remains unacceptably high.

Even if the FOMC remains on hold, the stance of monetary policy is likely to tighten passively in coming months. Real interest rates matter more for real economic growth than nominal interest rates. If, as we forecast, the FOMC remains on hold as inflation recedes gradually further in coming months, then the real fed funds rate will creep higher (Figure 1). Although the probability of a “soft landing” has increased, the economy is by no means “out of the woods” in terms of a potential recession. Indeed, we continue to forecast that real GDP will contract modestly in the first half of 2024 and that the unemployment rate will rise by roughly one percentage point or so from its current level of 3.5%. For details, see our most recent U.S. Economic Outlook.