{kind=link}

U.S. Highlights

- Speaking at the Jackson Hole Economic Symposium on Friday, Chair Powell noted that some progress had been made on the inflation front, but that inflation was still “too high”. He noted that the Fed would proceed carefully in either tightening the policy rate further or holding it constant as it watches the data.

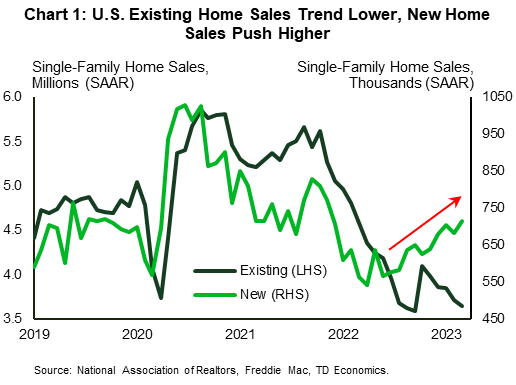

- Existing home sales were one piece of data reacting strongly to higher rates, falling further in July. Inventories remained lean, at 42% below pre-pandemic levels.

- Lack of supply in the existing market continues to push buyers to the new market, with sales there up strongly in July.

Canadian Highlights

- Consumer activity was soft in June, with retail sales posting a very mild gain. Actual Q2 consumer spending is released with GDP data next week, and the retail data is pointing to a subdued 1% annualized gain in overall spending.

- July’s flash estimate flagged stronger retail spending growth last month, in line with our internal debit and credit card data. However, temporary government income supports were likely behind these healthy prints, and spending growth is set to fade.

- In a bid to help housing affordability, the federal government may be looking at capping international students. This restricting of population inflows would weigh on consumption.

U.S. – Fed Chair Powell Sticks to Tough Talk

In a relatively quiet economic data week, markets took their cue from Chair Powell’s Jackson Hole Economic Symposium speech. The annual speech is always a highly anticipated event, but this year’s was particularly important with the Fed being at a monetary policy pivot point. The speech struck a balance between acknowledging that some progress had been made on inflation, but that it remained “too high” with substantial ground to cover to get back to price stability. Equity and bond markets didn’t like this reminder and were down on Friday (at time of writing).

The Chair noted the FOMC was prepared to “raise rates further if appropriate”, and that it intended to hold policy at a restrictive level until confident that inflation was moving sustainably down toward its objective. However, given that they are navigating in a cloudy environment, they would proceed “carefully”. What appeared to be off the table was any indication of potentially lowering rates, thus giving the speech a more hawkish tilt in our view. We believe that the continuation of this tough talk is necessary to prevent an undesirable give back in bond yields and, ultimately, to help keep inflationary expectations in check as it continues to monitor the data closely.

Powell provided a little more detail into the factors that will go into policymaking by breaking down inflation into three key categories. This included core goods inflation, along with housing and non-housing services. He noted progress on all three. On non-housing services – a category also known as “supercore”, which accounts for over half of the core PCE index – annual inflation has moved mostly sideways, but encouragingly it has started to decline on a three and six-month basis. Meanwhile, housing services inflation is expected to continue to ease given well-known lags, but they will be watching market rent data closely.

Speaking of housing, existing home sales continued to head lower in July. With mortgage rates some 40 basis points higher than in the two months prior it is no wonder that activity pulled back. The elevated rate environment also poses a hurdle on the supply side, as existing homeowners with much lower mortgage rates are reluctant to move and take on a higher rate. This theme is evident in inventories, which were 42% lower than pre-pandemic July levels (July 2019).

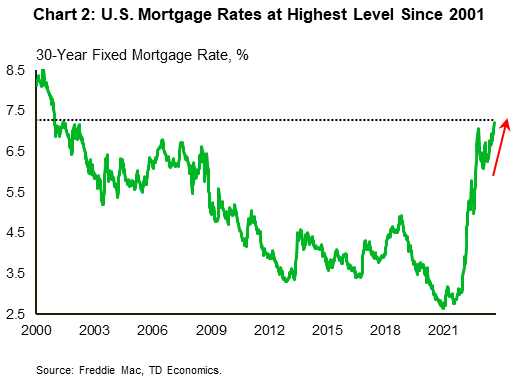

The tightness in resale market has kept a floor on home prices, while also pushing more would-be buyers to the “new” home market. New single-family home sales continue to buck the broader negative trend, making additional gains in July (Chart 1). This has been much to the delight of homebuilders, who have looked to boost supply in the single-family sector. While this trend may have some more room to run, mortgage rates have pushed even higher recently and are now hovering in the 7.2-7.5% range (Chart 2). This could test the strength of the positive single-family homebuilding trend sooner than anticipated, as evidenced by the recent pullback in homebuilder confidence and some flattening in single-family housing permits. Ultimately, it all ties back to interest rates, which, given the Fed’s continued tough talk, appear set to remain higher for longer.

Canada – Cooler Spending On Tap

It was a choppy week for bonds, with Canadian yields diving lower on Wednesday amid weak global PMI data before recovering some lost ground to end the week. As of writing, the benchmark Canadian 10-year yield was on track to end the week modestly lower than where it began. Oil prices are seemingly headed for their second weekly decline on Chinese growth concerns, reports of healthy supply coming out of Iran and the possibility that U.S. sanctions might be lifted on the Venezuelan oil sector.

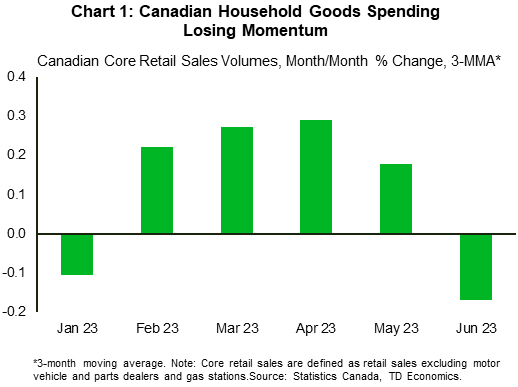

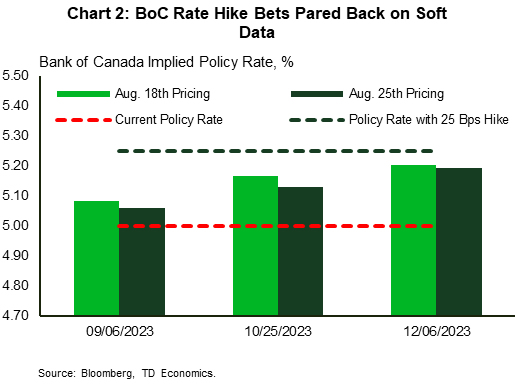

This soft tone extended to the June retail sales data, which inched only marginally higher by 0.1% month-on-month (m/m). On the one hand, it slightly beat Statistics Canada’s advance estimate. On the other, core sales (which strip out autos and gas stations), plunged nearly 1% m/m (Chart 1), and volumes were slightly lower. This cooler consumer momentum contributed to traders paring back their expectations for BoC hikes (Chart 2).

One silver lining from the retail report was that nominal spending may have increased 0.4% m/m in July according to Statcan’s preliminary estimate. Taken together with healthy flash estimates for manufacturing and wholesale activity in July and growth in hours worked reported in the Labour Force Survey, it appears that overall economic growth was positive last month.

The retail report also squares with our internal data showing a solid monthly gain in debit and credit card spending in July. But there are good reasons to fade this positive news. Recall that last month, the federal government paid out the $2.5 billion Grocery Rebate and one payment of the enhanced Canada Workers Benefit. Assuming no additional step-up in government supports, this temporary boost to household incomes will dissipate and with it, momentum in consumer spending. Accordingly, after a hefty third quarter, we expect a slowdown in household spending thereafter.

The federal government may soon be doing their part to soften consumer spending by limiting population flows. Cabinet ministers met this week to discuss Canada’s housing affordability crisis and one of the solutions floated was a cap on international students. Capping international student inflows is likely an easier lever to pull to address rental affordability than ramping up new home construction quickly. However, the idea was met with some resistance. At least one province – Quebec – has been unreceptive, vowing to reject the federal government’s idea. Provinces would likely be on the hook for some of the tuition shortfall for post-secondary schools.