{kind=link}

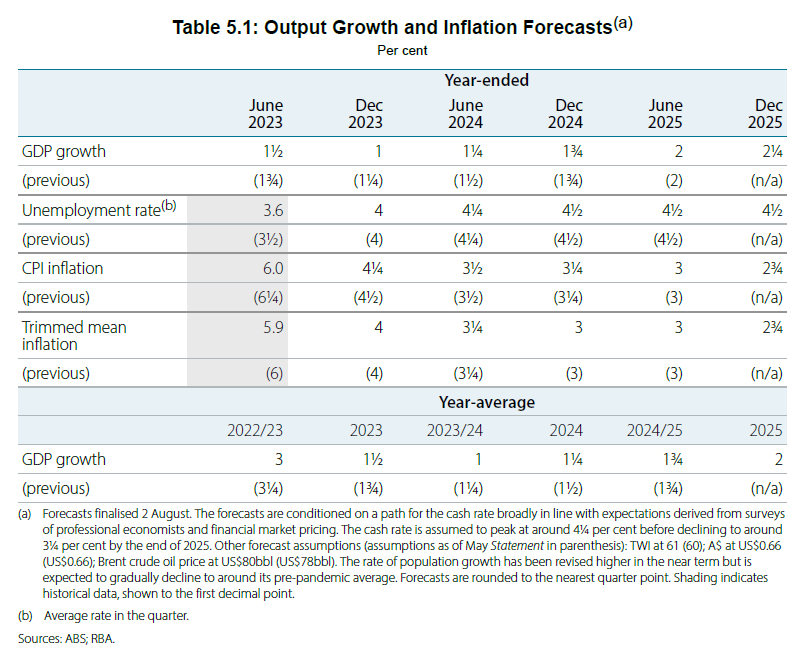

In the quarterly Statement on Monetary Policy, RBA reiterated that “some further tightening of monetary policy may be required”. This decision, however, would hinge on the incoming data and the evolving assessment of risks. Economic forecasts remain largely unchanged, with a slight downgrade in 2023 CPI forecast as well as 2023 and 2024 GDP projections.

The central bank’s outlook for inflation remains more or less steady as compared to three months ago. “CPI inflation is forecast to continue to decline, to be around 3¼ per cent at the end of 2024 and back within the 2–3 per cent target range in late 2025,” the statement highlighted. The Board maintains that the risks around the inflation outlook are “broadly balanced”.

While the labour market remains tight, conditions have seen slight relaxation. The bank notes, “In response to the tight labour market and high inflation, wage growth picked up to its highest rate in a decade.”

The economic growth perspective appears somewhat muted, with the statement acknowledging that “Growth in economic activity has been subdued this year.” Looking ahead, the central bank remains cautious, predicting that “Growth in the economy is expected to remain subdued over the period ahead.”

New economic forecasts

CPI inflation at (vs previous forecast):

- 4.25% in Dec 2023 (down from 4.50%).

- 3.50% in June 2024 (unchanged).

- 3.25% in Dec 2024 (unchanged).

- 300% in Jun 2025 (unchanged).

- 2.75% in Dec 2025 (new).

Trimmed mean CPI inflation at:

- 4.00% in Dec 2023 (unchanged).

- 3.25% in Jun 2024 (unchanged).

- 3.00% in Dec 2024 (unchanged).

- 3.00% in Jun 2025 (unchanged).

- 2.75% in Dec 2025 (new).

Year-average GDP growth at:

- 1.50 in 2023 (down from 1.75%).

- 1.25% in 2024 (down from 1.50%).

- 2.00% in 2025 (new).