also slowed to 4.8% year-on-year from 5.3% recorded in May and dipped below the current Fed Funds rate of 5% to 5.25%.){kind=link}

- Current up moves in long-duration equities and fixed income came at the expense of a weaker US dollar.

- A persistent weak US dollar may lead to an upside revival in commodities prices.

- Inflationary expectations may creep up again due to higher oil/commodities prices.

- Disinflationary narrative seems premature and may be mispriced.

Market participants have taken a “disinflation ecstasy pill”, bidding up long-duration equities and fixed income in the past two sessions after the latest June US CPI data came in below expectations with the headline print dipped to 3% year-on-year, its slowest rate of growth seen in two years. The core consumer inflation rate (excluding food & energy) also slowed to 4.8% year-on-year from 5.3% recorded in May and dipped below the current Fed Funds rate of 5% to 5.25%.

In terms of week-to-date performances as of 13 July, higher beta and long-duration equities outperformed, and the Nasdaq 100 rallied by +3.56%, just 7.7% away from its November 2022 all-time high. Over in the fixed income space, last week’s losses were almost recouped; iShares 20+ Year Treasury Bond exchange-traded fund (ETF) recorded a week-to-date gain of 2.84%, iShares Investment Grade Corporate Bond ETF (+2.61%), and iShares High Yield Corporate Bond ETF (+2.44%).

This latest bout of “disinflationary optimism” has revived the “Fed Pivot” narrative where participants are now anticipating that the upcoming July FOMC meeting will likely see the last interest rate hike of 25 basis points (bps) to end this current cycle of monetary policy tightening in the US and negate the current “higher interest rates for a longer period” guidance advocated by Fed officials.

US Dollar Index’s major downtrend was reinforced via a break below 100.95 key support

Fig 1: US Dollar Index medium-term and major trend as of 14 Jul 2023 (Source: TradingView, click to enlarge chart)

The current disinflationary theme play has come at the expense of a weaker US dollar that sank to a 15-month low, the US Dollar Index has tumbled by -2.52% for this week, set for its worst weekly performance since the week of 7 November 2022 as it broke below the key medium-term support of 100.95.

Right now, there are second-order effects at play where significant global financial market movements are likely to spiral into the real economy in the months ahead. A weaker US dollar may translate to higher commodities prices as most commodities; physical and paper (futures contracts) are priced in US dollars.

This above-mentioned linkage of a weaker US dollar to higher commodities prices seems to be emerging in the financial markets; the week-to-date performance of WTI crude oil futures is up by +4.1% and a broader basket of commodities as measured by the Invesco DB Commodity Index Tracking Fund has rallied by 3.6% for this week.

Inflationary expectations may start to creep up

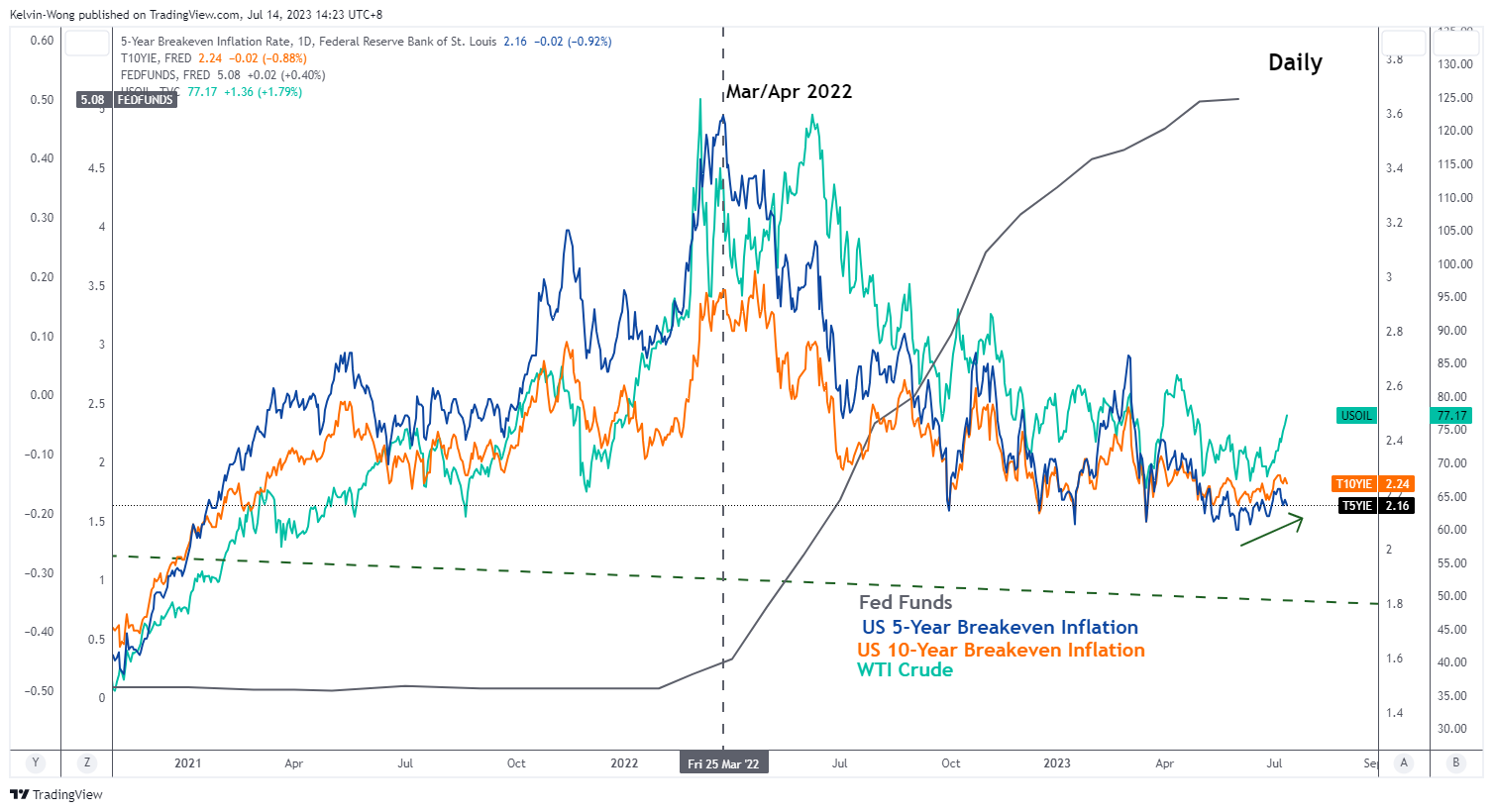

Fig 2: WTI crude oil correlation with US 5-YR & 10-YR breakeven inflation rates as of 13 Jul 2023 (Source: TradingView, click to enlarge chart)

Commodity prices such as oil have a high degree of direct correlation with forward-looking inflationary expectations.

In the past three years, the price actions of WTI crude oil have moved in lock-step with the US Treasury’s 5-year and 10-year breakeven inflation rates (a measurement of inflationary expectations). If WTI crude oil can maintain its current upward trajectory, inflationary expectations may creep higher from this juncture.

Potential upside momentum in commodities may spark another ascend in US CPI

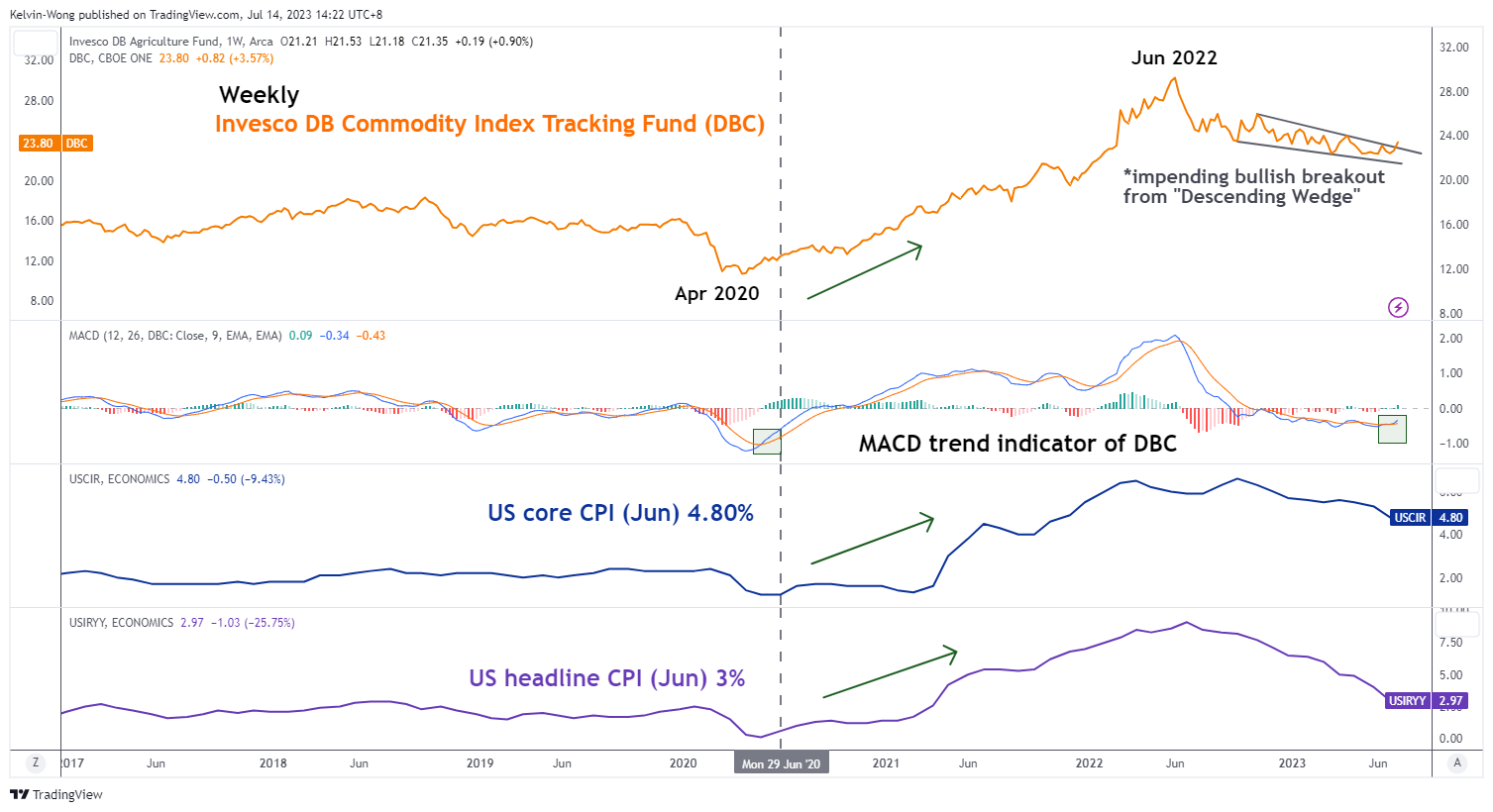

Fig 3: Invesco DB Commodity Index Tracking Fund major trend with US CPI as of 13 Jul 2023 (Source: TradingView, click to enlarge chart)

In addition, from a momentum perspective, an imminent trend change may start to take shape for commodities prices after close to one year of downtrend since June 2022 using Invesco DB Commodity Index Tracking Fund (DBC) as a commodities benchmark.

The current weekly MACD trend indicator of the DBC has just flashed a bullish crossover signal below its centreline that suggested that the major downtrend of DBC in place since the June 2022 high may have ended which in turn increases the odds of a bullish reversal for commodities prices.

A similar MACD bullish crossover observation on the DBC occurred in early June 2020 that spiralled into the real economy where inflationary pressures; headline and core US CPI started their ascend.

Therefore, a potential uptick in inflationary expectations coupled with the current positive momentum in commodities prices may put a halt to the current inflationary slowdown trajectory seen in the latest US CPI prints. The ongoing disinflationary narrative may be premature and mispriced at this juncture.