{kind=link}

Financial markets are awaiting with bated breath today’s US non-farm payrolls data, as labor market tightness continues to be a crucial variable in shaping Fed future policy trajectory. Market consensus predicts a healthy growth of 220k jobs in June, while unemployment rate is forecast to remain steady at 3.70%. Average hourly earnings are projected to see a moderate increase of 0.3% mom.

With the backdrop of this week’s related data, risks appear to be tilted towards a positive surprise. ADP reported private employment growth of 497k, which is almost double the anticipated 250k. ISM services employment bounced back from 49.2 to 53.1, while ISM manufacturing employment slipped from 51.4 to 48.1. The robust surge in service sector seems capable of more than compensating for the downturn in manufacturing sector.

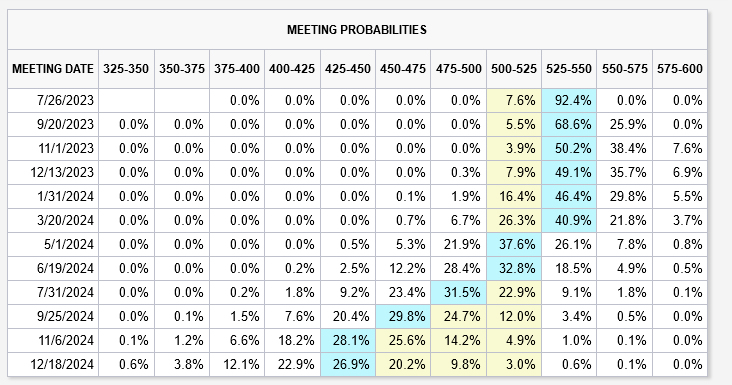

Ahead of the job report, Fed funds futures are pricing in a 92.4% likelihood of an additional 25 bps hike, which would bring rates to 5.25-5.50% at FOMC meeting in July.

Market participants appear to remain somewhat skeptical of FOMC members’ “strong majority” opinion that two or more rate hikes are necessary in 2023. However, probability of more tightening beyond July is gaining traction. Chance of interest rate reaching 5.50-5.75% in November currently stands at 46%.

Simultaneously, expectation for the first rate cut continues to be deferred, with odds remaining below 50% until March 2024.