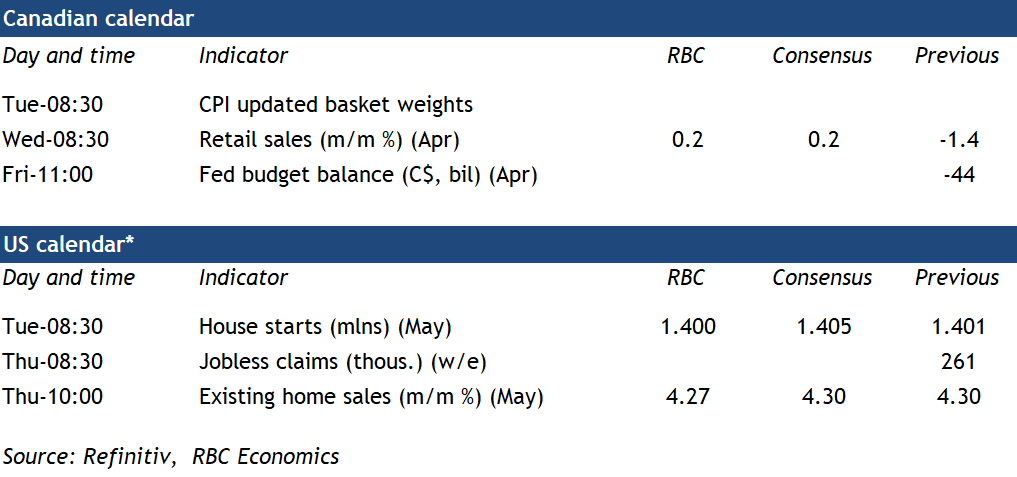

in both February and March.){kind=link}

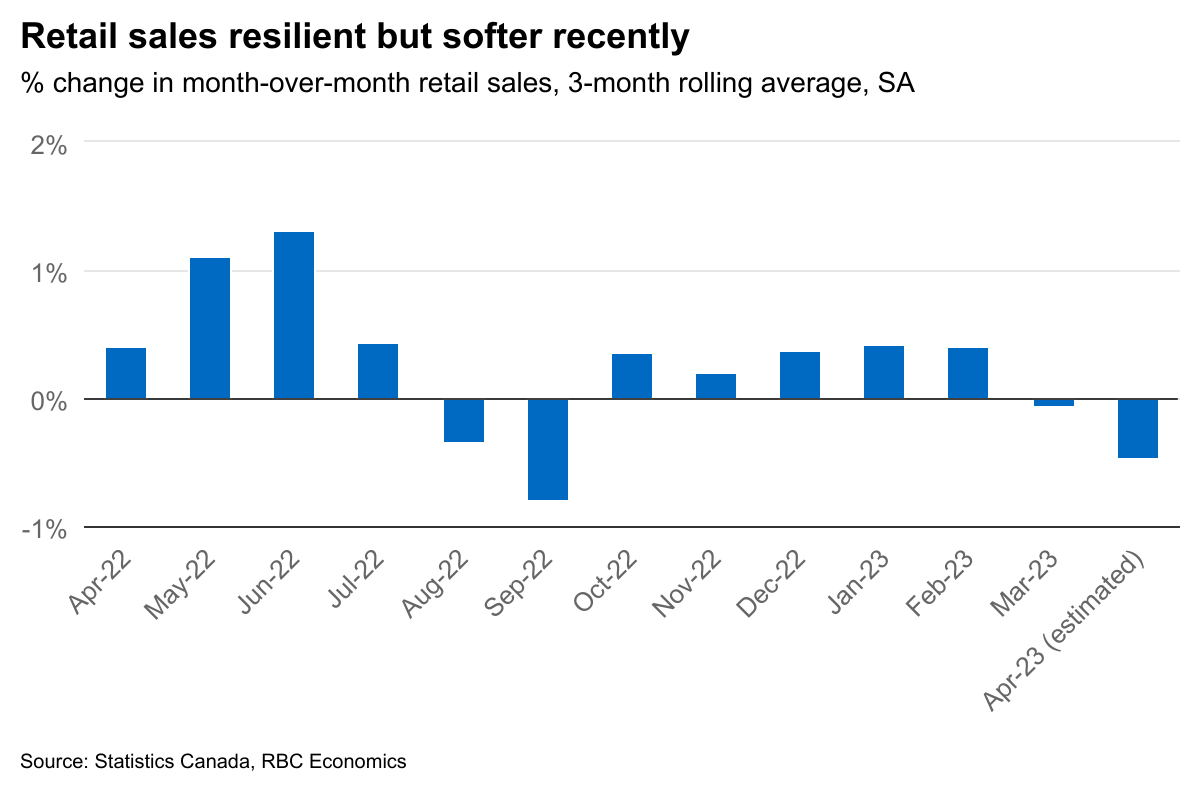

We expect next week’s retail sales data to show further softening in consumer spending for April. The advance estimate for the month’s sales was for a slight 0.2% increase that likely reflected higher prices for gasoline rather than an increase in the quantity of purchases. Consumer spending was surprisingly resilient early in 2023, with a 5.7% annualized increase in the first quarter. But most of that boost came from strong spending in January. Recent monthly readings have been softer with declines in retail sales volumes (excluding price impacts) in both February and March.

Our own tracking of spending is pointing to a stronger increase May, and spending on services (not counted in the retail sales data) has remained firm. That resilience was cited by the Bank of Canada in its decision to hike interest rates in June for the first time since January. Still, the lagged impact of higher rates continues to feed through to household borrowing costs with a lag. Canada’s debt service ratio rose to 14.9% in Q1 , just one tenth of a percent shy of the pre-pandemic record high. Higher prices and debt payments already soaked up all of the increase in Canadian household after-tax income last year, and delinquency rates on credit cards and auto loans have ticked back above pre-pandemic levels. Meantime, signs of cracks have continued to surface in labour markets. We continue to expect spending to flag over the second half of this year, even with surprising resilience year-to-date.

Week ahead data watch

Next Tuesday, StatCan will release the 2023 CPI basket weights update, which reflects the consumer expenditures in 2022. The new weights will account for changes in consumer spending patterns by looking at expenditure data from Household Final Consumption Expenditures, Survey of Household Spending, and alternative data sources.