{kind=link}

US stocks held onto losses after a data dump didn’t really give a clear signal about the economy. Wall Street is suffering from a Fed hangover that won’t go away anytime soon as the economy will remain vulnerable as further tightening seems likely. The US consumer remains robust, the labor market is slowly weakening, and the manufacturing sector is full of mixed signals. This morning’s data won’t move any Fed members, but if we continue to see healthy spending throughout the summer, the Fed will need to deliver on that dot plot forecast that has penciled in two hikes.

Now that we’ve seen so many mega-cap tech stocks overextend themselves, traders are reassessing some of the high-flying stocks, like Tesla. Tesla’s 13-day surge couldn’t last forever and that is leading to some profit-taking. Tesla’s pullback may have been triggered by the Fed’s hawkish pause, but it could also be a sign that some momentum behind the AI boon could be running out of steam for now.

US Data

Retail spending is not cooling and should keep Wall Street nervous that the disinflation process could struggle going forward. Strong buying confirms what everyone knows about the job market… it is too strong. Retail sales in May rose 0.3%, much better than the expected decline of 0.2%. Americans are buying everything from cars, furniture, electronics, and building materials.

Weekly jobless claims were unchanged at 262,000, a high print compared to the consensus estimate range of 230-268K. The labor market is still slowly weakening here.

A couple Fed regional surveys painted a mixed picture. The Empire manufacturing report posted an impressive rebound, while the Philly Fed outlook remained deeply in contraction territory. The manufacturing part of the US economy is stabilizing here, but not at a level that is triggering inflation worries for goods pricing.

FX

The Japanese yen is approaching the danger zone as FX traders anticipate the BOJ will disappoint in tightening when compared to the US. Betting on the yen has been painful and if dollar-yen falls to 145, that could trigger action by Japan.

ECB

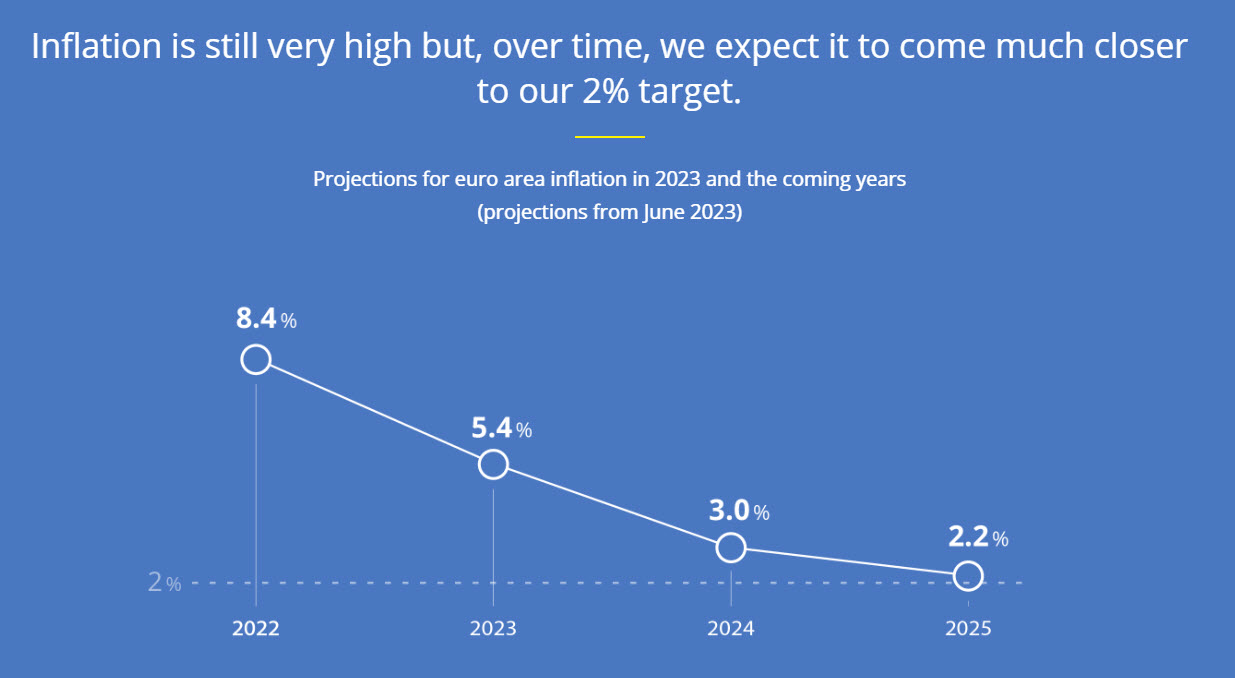

THE ECB raised rates by a quarter percentage point and raised their inflation forecasts for the next couple of years. The statement noted that the key ECB interest rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and will be kept at those levels for as long as necessary. They confirmed that they will discontinue the reinvestments under the asset purchase program.

The euro initially rallied on the raised inflation forecasts but that doesn’t change expectations that they are getting close to the end of this rate hiking campaign. Lagarde signaled a hike in July and more importantly a determination to get inflation down. The euro is now trending above all three key (200-, 100-, and 50-day) SMAs. Critical resistance doesn’t emerge until 1.10 region.