{kind=link}

U.S. Highlights

- Financial markets remained eerily positive this week, despite the debt ceiling X-date looming with no bipartisan deal in sight.

- Retail sales data for April showed the continued resilience of the U.S. consumer, while housing starts are looking to have reached a bottom after having fallen 24% last year. Home sales were lower in April, and likely have a bit further to fall.

- Fed speakers diverged this week on the near-term trajectory of the fed funds rate. Financial markets are still pricing 50 bps of rate cuts by year-end.

Canadian Highlights

- CPI inflation surprised to the upside, rising by 4.4% year-on-year (y/y) in April, up from 4.3% y/y in March. This was the first increase in the inflation rate since June 2022.

- Real estate data also came in hot, as home sales shot up by 11% month-on-month (m/m) in April, and the average home price rose by 6% m/m.

- Canadian retail sales data came in at -1.4% m/m in March, but when we add in services, consumer spending grew at an above trend clip in the first quarter of 2023.

U.S. – Optimistic Markets Cheer the Small Wins

Risk sentiment remained eerily positive across global financial markets this week, despite the clock ticking down on the debt ceiling X-date. But instead of losing the forest for the trees, investors seemed to cheer the incremental progress made this week. President Biden and Speaker McCarthy, and their negotiators, met on Tuesday for a closed-door meeting, where there appears to be some common ground on several items including clawing back unspent pandemic relief funds, speeding up permitting of domestic energy projects, and applying stricter work requirements for some social safety net programs. However, the two parties remain deeply divided on the size of broader spending cuts. At the time of writing, equity markets are looking to end the week up 2%, while the 10-year Treasury is up 25 bps to 3.71%.

Turning to the economic data, retail sales data painted a picture of a still resilient consumer in April. Although headline retail sales (+0.4% m/m) came in below expectations (+0.8% m/m), this was partially the result of a pullback in gasoline sales – largely a price- driven decline. The headline was also weighed down by weaker growth in motor vehicle sales, despite wholesale auto sales showing a healthy gain last month. After removing the volatile items, the control group – a more precise measure of consumer spending – rose by a healthy 0.7% m/m. This suggests continued momentum for Q2 consumer spending, with our current tracking around 1%-1.5%.

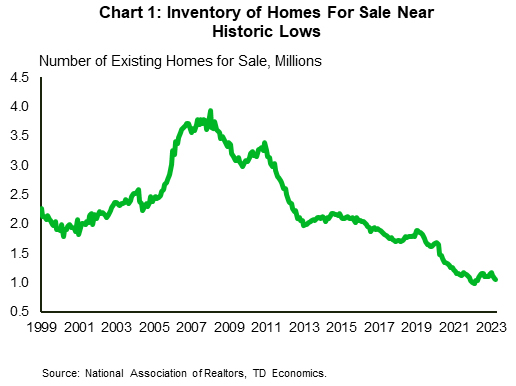

Data out this week on the housing market showed existing home sales fell by 3.4% m/m to 4.28 million units in April. The pullback comes after sales had shown signs of life earlier this year. However, much of that activity was the result of a pullback in mortgage rates that had occurred between October-January. Since then, mortgage rates have again turned higher, and at 7.1%, are not far off last year’s highs. Not only has this kept new homebuyers on the sidelines, but it has also discouraged move-up buyers from listing properties, which has kept inventory levels near historic lows (Chart 1).

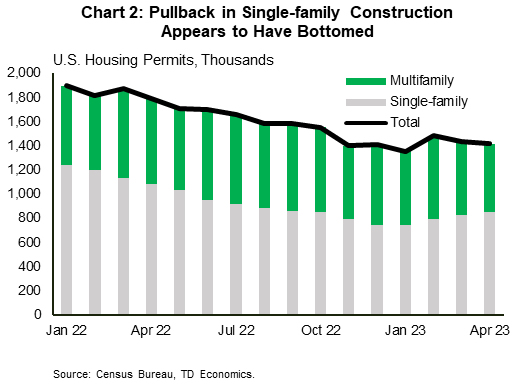

While home sales likely have a bit more room to fall, housing starts may have already reached a bottom. Residential construction rose 2.2% m/m to 1.4 million in April, with gains seen across both the multifamily (+3.2% m/m) and single-family (+1.6% m/m) segments. Permitting activity points to an uptick in construction in the single-family segment over the coming months, though this will likely be offset by some pullback in multifamily, which has yet to feel any correction through this tightening cycle (Chart 2).

Several Fed speakers this week showed a growing divergence among committee members on the near-term trajectory of the fed funds rate. While a few officials endorsed another rate hike, others are favoring a pause given the recent banking turmoil and the uncertainness it poses to the economic outlook. However, all officials still support rates remaining elevated through this year, which remains at odds with market pricing where 50 bps of cuts are still expected by year-end.

Canada – Canadian Economy is Too Hot to Handle

It was a busy week for Canadian economic data. CPI inflation readings showed an acceleration in prices, while the real estate market surged into the spring buying season. The hot data caused a massive repricing for the Bank of Canada (BoC), with markets now leaning towards another 25 basis point (bp) hike this summer. The Canada 2-year yield rose a whopping 40 bps, reaching its highest level since the start of the U.S. regional banking stress in March.

Consumer prices rose by 4.4% year-on-year (y/y) in April, up from 4.3% y/y in March. This was the first increase in the inflation rate since June 2022. Gasoline was the main contributor, with prices at the pump rising 6.3% month-on-month (m/m). Outside of energy, overall inflation was boosted by rising rent, mortgage interest costs, and prices for recreational vehicles.

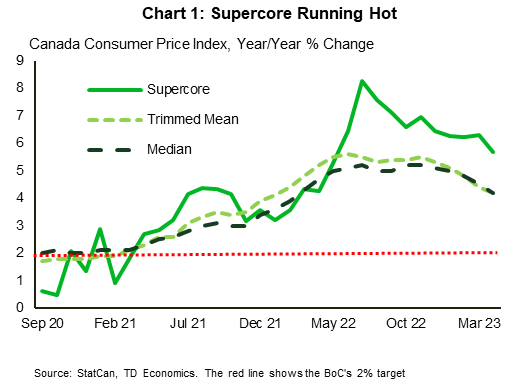

The Bank of Canada’s core inflation metrics (trimmed mean and median) were a little more encouraging, averaging 4.2% y/y, versus 4.5% y/y in March. Even our measure of ‘supercore’ inflation that reflects cyclically driven services inflation decelerated to 5.7% y/y, from 6.3% y/y in March (Chart 1). The cost of travel was the major disinflationary force as prices have come down from the peaks seen last year.

While the comparisons to last year are moving in the right direction, core readings on a three-month basis are more worrying. The average of the BoC’s core measures increased to 3.7%, from 3.4% in March. These timelier measures point to more persistent inflation pressures than we expected in our March forecast.

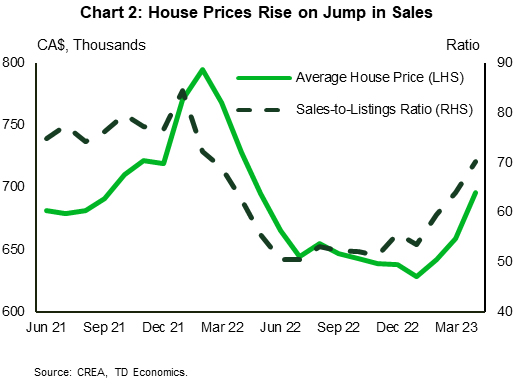

Speaking of hot, look no further than the Canadian real estate market. Home sales shot up by 11% m/m in April, as they jumped off the floor formed earlier in the year. At the same time, listings were only higher by 1.6% m/m, putting the sales-to-listings ratio firmly into sellers’ territory at 70.2% (Chart 2). The demand/supply imbalance pushed the average home price up by 6% m/m. Housing starts also shot-up by 22% m/m in April, as the reigniting of the real estate market incentivized building.

Canada is in the midst of a cyclical upturn. The jobs market has accelerated on Canada’s population boom, wages are growing faster than inflation, and governments are providing generous inflation support transfers. This income windfall has Canadians spending once again. While today’s retail sales numbers showed a -1.4% m/m drop in March, they are missing the surge in services spending and strong demand from online shopping. Our more holistic tracking for consumer spending for 2023 Q1 is coming in around 5% (quarter-on-quarter, annualized)!

BoC Governor Macklem spoke this week following the release of the Bank’s Financial System Review. Although the discussion was focused on the risks facing the Canadian financial system, it was notable that the Governor seemed to be looking past the recent upturn in economic data. While the BoC’s view is that growth will slow in the coming months, should the economy continue to accelerate in line with recent data, another rate hike may be put back on the table by this summer.