and had a meeting between President Biden and Congressional leadership as they attempt to find an agreement to raise the debt limit. Markets ended the week relatively unchanged, with the S&P 500 down 0.1% and the ten-year Treasury Yield down 4bps at 3.41% as of the time of writing.){kind=link}

U.S. Highlights

- Inflation eased modestly in April, with headline and core CPI both ticking down by 0.1 percentage points to 4.9% and 5.5% year-on-year respectively.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed that a higher share of commercial banks tightened credit conditions in April than January.

- A meeting between President Biden and Congressional leaders failed to yield any progress on negotiations to raise/suspend the debt limit.

Canadian Highlights

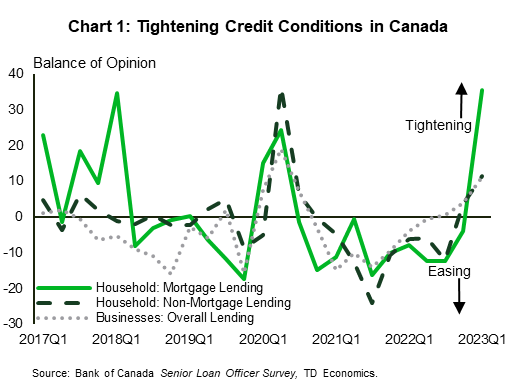

- Borrowing for households and businesses is getting tougher. The Bank of Canada Senior Loan Officer Survey highlights tightening credit conditions for households and business in the first quarter of the year. Notably, household mortgage lending has become less accessible.

- Transitory events including the PSAC workers strike and ongoing Alberta wildfires will throw curveballs into the next few GDP updates, but this will not affect the Bank of Canada’s monetary policy stance.

- Next week’s data-heavy calendar will be led by updates to April CPI, where we expect a cooling of headline inflation to 4.0% y/y with similar declines in various core measures.

U.S. – Inflation Continues to Cool in Earnest

On the heels of last week’s FOMC meeting, we were provided with a host of economic data this week to assess the Fed’s new wait-and-see approach, including April’s CPI report. In addition, we also received the second quarter Senior Loan Officer Opinion Survey (SLOOS) and had a meeting between President Biden and Congressional leadership as they attempt to find an agreement to raise the debt limit. Markets ended the week relatively unchanged, with the S&P 500 down 0.1% and the ten-year Treasury Yield down 4bps at 3.41% as of the time of writing.

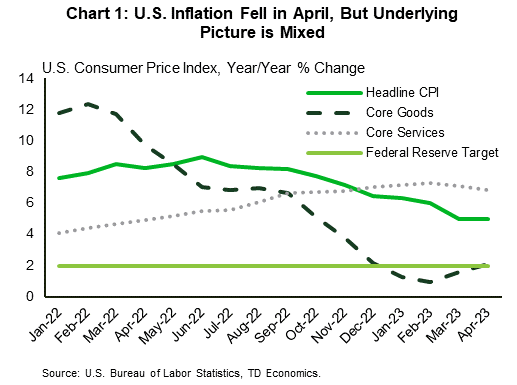

Inflation eased modestly in April, as headline inflation rose by 4.9% year-on-year, down modestly from 5% in March (Chart 1). Energy prices rose for the first time in three months as gasoline jumped by 3% month-on-month (m/m), and food prices were flat for a second consecutive month. Stripping out energy and food, core inflation ticked down to 5.5% y/y, having fluctuated between 5.5-5.6% y/y since January. While we did see shelter inflation decelerate for a second consecutive month, it still rose by 0.4% m/m. This in addition to the reacceleration in core goods inflation, worked to keep core inflation elevated. Although on aggregate this report had positive developments, it reiterated the fact that the path back to the Fed’s 2% target is unlikely to be a straight line.

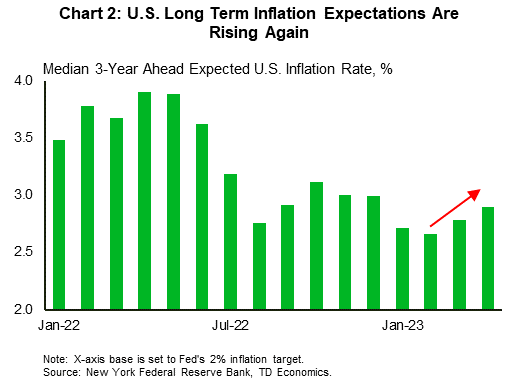

Of particular concern for the Fed is the potential for inflation expectations to become de-anchored. In the New York Fed’s Survey of Consumer Expectations this week, we saw three-year ahead inflation expectations rise for a second consecutive month to 2.9% in April (Chart 2). While this series has historically run slightly above the Fed’s 2% target, a sustained movement above 3% would be a concern for the FOMC.

Earlier in the week, we saw that U.S. commercial banks continued to tighten credit conditions in April in the Fed’s SLOOS. Commercial & industrial loans as well as commercial real estate (CRE) loans saw a higher net percentage of banks tightening credit standards than in January. Demand for these loans from businesses fell as a result, however household demand for consumer-facing loans (mortgages, auto, credit card, etc.) rose as credit remained relatively accessible. Further analysis of the SLOOS can be found here.

Lastly, in the Oval Office this week, President Biden met with Congressional leaders on Tuesday to attempt to find an agreement to raise/suspend the debt limit. Treasury Secretary Yellen warned last week that the Treasury could run out of funds by early June, thus the impetus to reach an agreement is elevated. However, no progress has been made in the negotiations so far.

Looking ahead to next week, we will get a fresh update on the U.S. consumer with April retail sales as well as existing home sales. With the unemployment rate back down to 3.4% consumers may still have some wind in their sails, but we expect that this will be short-lived as past rate hikes continue to filter through the economy.

Canada – New Information, Same Narrative

Canada quietly stood on the sidelines this week without any top-shelf macro updates on the economic calendar. Jittery market sentiment continues to be driven by contentious U.S debt limit discussions, turmoil in the banking sector, and more recently, the concern that tighter credit conditions could lead to excessive slowdown south of the border. In Canada, we received our own pulse check on credit conditions.

The Bank of Canada’s (BoC) Senior Loan Officer Survey for the first quarter highlighted a significant tightening in mortgage lending conditions (Chart 1). Data availability restricts drawing comparisons to the ’08–’09 financial crisis, but current readings suggest stronger headwinds against mortgage credit growth in the near-term. Non-mortgage household lending conditions also tightened, making credit less accessible to consumers. On the business side, overall lending conditions also tightened notably, but remain below the peak seen during the pandemic, and the previous high in 2016. Credit conditions in Canada are displaying differing characteristics to those in the U.S., where credit standards for businesses are tightening disproportionally compared to household credit.

Aside from this, a series of transient shocks over the last couple of months will throw kinks into forthcoming data, notably monthly GDP readings. Firstly, the federal PSAC workers strike that kept ~150,000 workers off the job for two weeks may have lopped two-tenths of a percent off of April GDP. This effect may have been partially counteracted by the Federal government’s GST/HST credits that hit Canadians’ accounts at the beginning of April.

The expected GDP boost for May as workers came back on the job, could now be weighed down somewhere to the tune of 0.2 percentage points (ppts) by to the ongoing Alberta wildfires. Alberta’s oil & gas sector accounts for roughly five percent of national level GDP, and while conditions have improved, major oil producers had curtailed cumulative oil output by up to ~320,000 barrels per day (or almost 4% of national level production). The shut-ins are temporary but have been sustained long enough to have measurable effects.

In Statistics Canada’s February GDP release, they noted that the Canadian economy likely contracted by 0.1% in March. This puts first quarter GDP tracking above-trend at around 2.5% annualized. Imposing net-drag effects from recent events, Q2 GDP will likely come in lower than the 0.7–1.0% annualized estimates that both we and the BoC have penciled in. However, this should give way to a growth rebound in Q3. All said, we do not see any effect on monetary policy as the Bank of Canada will likely look through the noise, instead focusing on the fight to bring inflation durably back to target.

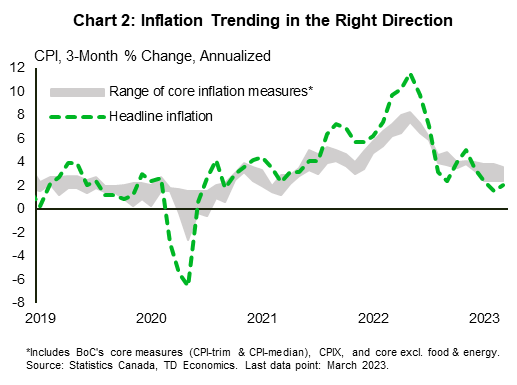

After a quiet week for data, next week features a lineup of heavy hitters. April’s inflation release next week will be the lead off. We expect headline CPI to cool another 0.3 ppts to 4.0% y/y with broadly equivalent slowdowns across the suite of core measures (Chart 2). Also on tap, retail sales for March likely slowed, evidenced by our TD Spend data that showed consumers pumped the brakes on spending for the month. Lastly, we’ll receive updates on April’s housing starts and existing home sales.