{kind=link}

- China’s benchmark stock indices have underperformed against the rest of the world.

- Weak macro data and geopolitical risk have reinforced the recent bout of weakness.

- China’s central bank, PBoC may be forced to undertake more proactive accommodative policies.

In the past week, the performances of the benchmark China stock indices and its proxies have underperformed the rest of the world. In terms of week-to-date returns at this time of the writing, the CSI 300 and China A50 have recorded losses of -1.10% and -0.90% respectively that versus the MSCI All-Country Word Index ETF at -0.40%.

In addition, the Hong Kong benchmark stock indices have also lagged this week with losses seen in the Hang Seng Index (-2.00%) and Hang Seng China Enterprise Index (-1.70%). The exception so far is from the Hang Seng TECH Index which is heavily concentrated in China’s Big Tech stocks trimmed its earlier week-to-date loss of -3.5% to -0.15% assisted by better-than-expected Q1 earnings results of e-commerce giant, JD.com.

Weak macro data put downside pressure on the 5% GDP growth target of China for 2023

The recent key economic data out from China has indicated that the growth spurt from the “post-Covid zero reopening” policies has dissipated.

Manufacturing activities slipped back to contraction mode in April after three consecutive months of growth and the services sector is also signs of expansion fatigue as the Caixin Services PMI for April has slipped to 56.4 from a 28-month high of 57.8 printed in March.

Inflationary pressures have been surprisingly lacklustre in China despite the recent growth-oriented policies implemented by key policymaking state agencies. The latest consumer price index data for April has decelerated to 0.1% year-on-year, its 3rd consecutive month of slowdown below 2%, and factory gate prices measured by the producer price index plunged to -3.6% year-on-year, its seventh straight month of contraction.

These data are pointing to a weak external environment and the lack of inertia from domestic demand to cover the shortfall has increased the risk of the deflationary spiral in China, a toxic concoction that may persist if left unaddressed. Also, inflationary pressures in China are way below the average gauge of inflation rate among emerging and developed countries.

Heightened geopolitical risk may push away foreign investors

Foreign direct investments and portfolio flows into China may slow down due to the latest government-led policies that tighten foreign access to sensitive information on Chinese corporations and key management personnel amid growing tensions with the US.

In addition, an earlier initiative urged state-owned enterprises to phase out the internationally recognized “Big Four” accounting firms for audits in China due to data security concerns.

All these measures will create a shade of “opaqueness” in China’s financial markets that may deter foreign capital inflows despite the Chinese stock market that has a cheaper valuation than the US; the MSCI China trades at a forward price-to-earnings ratio of 10.2 versus a ratio of 18.0 on the US S&P 500 based on data from Refinitiv as of 10 May 2023.

China central bank, PBoC may be forced to open its liquidity tap

Credit growth in China has moderated significantly in April where aggregate financing reached 1.22 trillion yuan, below the consensus forecast of 2 trillion yuan. In addition, M2 growth, the broadest measure of money supply dipped down to 12.4% year-on-year, its slowest pace seen so far this year.

PBoC’s current stance in promoting growth is following the script of a targeted approach rather than an all-out quantitative easing style to prevent unproductive resources to be deployed into speculative activities.

Given the prior Politburo’s April meeting that emphasized proactive fiscal policy should be stepped up and work alongside monetary policy to boost the current insufficient levels of demand, PBoC may implement a policy interest rate cut on its one-year medium-term lending facility (MLF) rate soon, either next Monday, 15 May or in June to address the recent weak macro data as mentioned earlier; the last cut on the one-year MLF rate was implemented in August 2022.

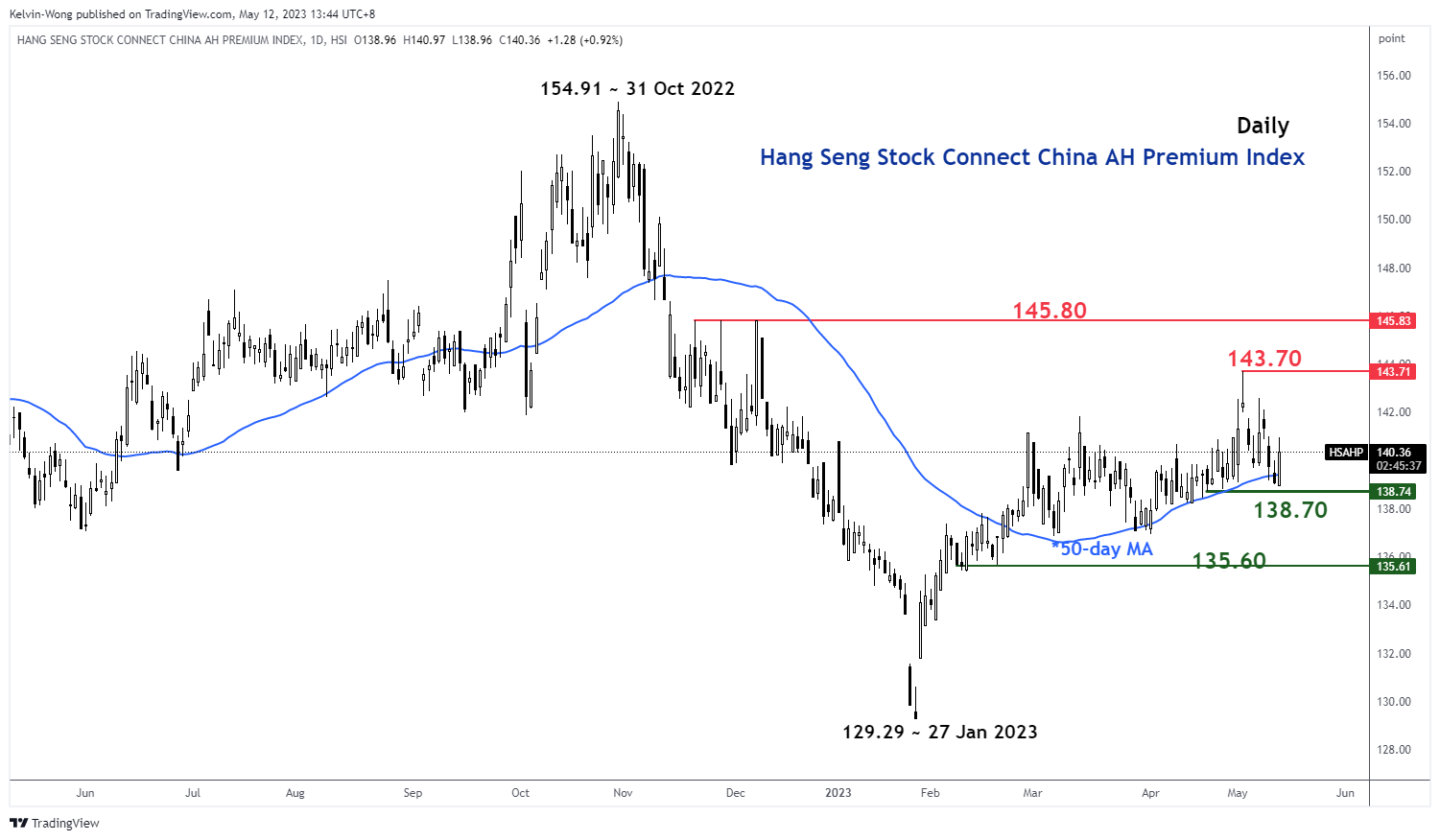

China AH share premium has reached a key support area

Fig 1: Hang Seng Stock Connect China AH Premium Index trend as of 12 May 2023 (Source: TradingView, click to enlarge chart)

The Hang Seng Stock Connect China AH Premium Index measures the absolute price premium or discount of China A shares over their dual-listed H shares in Hong Kong. A level above 100 indicates that A shares are more expensive than H shares and vice versa when the Index goes below 100.

The recent 3.3% contraction of the AH Premium Index from its 3 May 2023 high of 143.71 high has reached a key medium-term support at the 138.70 level which is defined by an upward-sloping 50-day moving average that the Index has traded above it since 22 February 2023.

Looking at the lens from a technical analysis perspective, the AH Premium Index may start to stage a rebound at this juncture and such a move is likely to be reinforced by more proactive accommodative monetary policies from PBoC. A potential up move in the AH Premium Index may reverse the recent softness seen in the China benchmark stock indices.

China A50 Technical Analysis – 12,300 remains the key support to watch

Fig 2: China A50 trend as of 12 May 2023 (Source: TradingView, click to enlarge chart)

The China A50 Index (a proxy for the FTSE China A50 futures) failed again to stage a bullish breakout above its 13,470 intermediate range resistance on Tuesday, 9 May; its second attempt and it staged a decline of -3.7% thereafter.

Short-term upside momentum is still non-existent as indicated by the 4-hour RSI oscillator which is still below a corresponding resistance at the 58% level and has room for a potential further slide before it reaches an oversold region (below 30%).

A point to note is that the Index is still evolving in a potential long-term bullish impending “Inverse Head & Shoulders” configuration since the 15 March 2022 low with the key medium-term pivotal support at 12,300.

A clearance above 13,470 sees the next resistance coming in at 14,100.