{kind=link}

Dollar finds itself on the back foot in early US trading as data showed both headline and core CPI slowed in April. This data release has also sent 10-year yield plummeting below 3.5% mark. Japanese Yen is finding some strength, bolstered by the drop in yields. On the other hand, commodity currencies are regaining their footing, emerging as the strongest contenders at present, while European majors lag significantly. Euro, in particular, continues to show a lackluster response to hawkish comments from ECB officials.

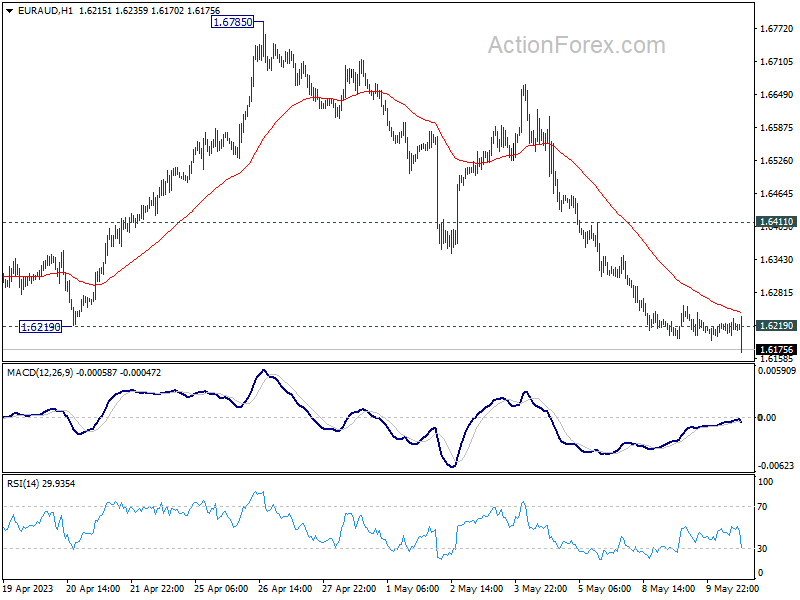

From a technical perspective, EUR/AUD pair seems to be gaining downside momentum, potentially breaking away from 1.6219 support level finally. Given that the drop from 1.6785 may be a correction of the entire uptrend that began at 1.4281, deeper decline back the 1.5976 resistance-turned-support level is anticipated.

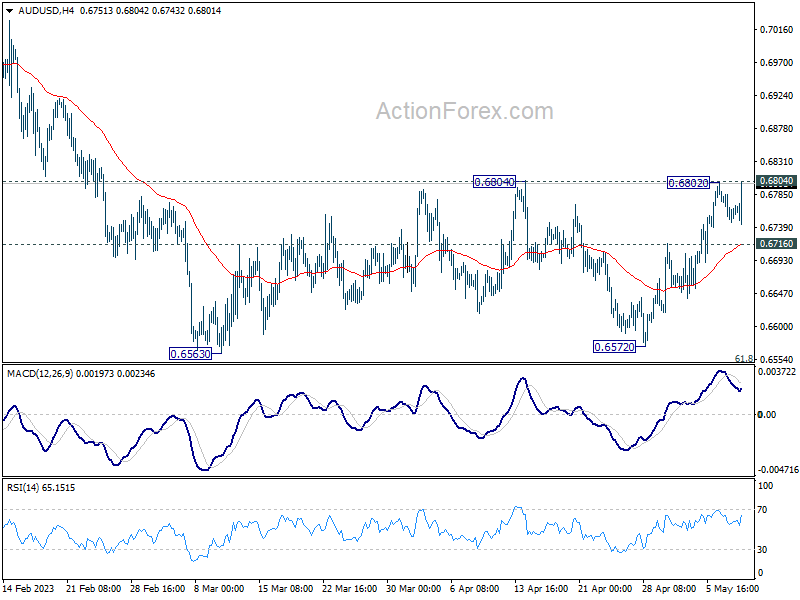

Meanwhile, AUD/USD pair’s key resistance at 0.6804 should be closely watched. Sustained breach of this level would cement Aussie’s near-term bullishness and could trigger a rally towards 0.7156 resistance level in AUD/USD.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is down -0.25%. CAC is down -0.20%. Germany 10-year yield is down -0.064 at 2.284. Earlier in Asia, Nikkei dropped -0.41%. Hong Kong HSI dropped -0.53%. China Shanghai SSE dropped -1.15%. Singapore Strait Times dropped -0.02%. Japan 10-year JGB yield dropped -0.0090 to 0.416.

US CPI ticked down to 4.9% yoy in Apr, core CPI down to 5.5% yoy

In April, US headline CPI slowed from 5.0% yoy to 4.9% yoy, below expectation of 5.0% yoy. That was the smallest 12-month increased since April 2021. Core CPI (all items less food and energy) slowed from 5.6% yoy to 5.5% yoy, matched expectations. Energy index was down -5.1% yoy while food index was up 7.7% yoy.

For the month, CPI rose 0.4% mom while Core CPI also rose 0.4% mom. Both matched expectations. Energy index rose 0.6% mom. Food index was unchanged.

ECB Lagarde: We still have more ground to cover

ECB President Christine Lagarde said in a Nikkei interview, “we are determined to tame inflation, to bring it back to our 2% medium-term target in a timely manner.” She acknowledged that “we have made a sizable adjustment already. But we still have more ground to cover”.

Highlighting the importance of data, Lagarde said, “Our reaction function will be anchored in the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, and this will dictate our decisions going forward.”

She emphasized ECB’s focus on headline inflation as the critical measure to ensure price stability. “That’s our thermometer, that’s what we are committed to doing,” she stated.

However, Lagarde also pointed to the relevance of additional inflation measures. “Core” inflation is one such measure, but others exist, such as those that exclude more volatile items or focus more on domestic inflation pressures.

She explained, “It’s to arrive at the ‘heart’ of inflation, the most persistent element in those price indexes that can help us understand where headline inflation is likely to settle in the medium term.”

Lagarde cautioned that significant upside risks to inflation outlook still exist, and the path of inflation remains uncertain. Therefore, she stressed the need for the ECB to be “extremely attentive to those potential risks.”

ECB Nagel: We’re coming to the home stretch, but we need to stay stubborn

In an interview with Deutschlandfunk radio, Bundesbank President Joachim Nagel painted a cautiously optimistic picture of ECB’s monetary policy landscape, implying that restrictive measures were beginning to bear fruit.

“We’re coming to the home stretch in the sense that we are reaching the area in monetary policy that’s considered restrictive,” Nagel noted, suggesting that ECB’s tightened policy stance was close to hitting its intended mark. He asserted his confidence that the monetary policy was indeed manifesting its effect.

However, he was quick to emphasize that ECB’s task was far from complete. “But we are not done hiking yet,” he added, “There is still work to be done on core inflation.”

Nagel emphasized the importance of staying the course with the current monetary policy, urging persistence. “We need to stay stubborn,” he said, reinforcing his commitment to seeing the central bank’s measures through.

Addressing concerns about the potential impact of the ongoing banking sector upheaval in the US on German banks, Nagel sought to allay fears. “German banks are in a fundamentally solid position,” he assured, indicating that he did not share the prevailing apprehensions over the stability of German banks.

ECB Stournaras: We can’t yet say how many more rate hikes will happen

In an interview with Greece’s Imerisia, ECB Governing Council member Yannis Stournaras indicated that while the end of the tightening cycle was in sight, it was not yet complete.

“We’re close to the end,” Stournaras remarked. But, “we’re not there yet, so I agree with Madame Lagarde that we still have some distance to go.”

Stournaras acknowledged the inherent uncertainty in projecting the number of additional rate hikes, with such decisions being heavily influenced by inflation forecasts, economic growth and the state of financial conditions.

“We can’t yet say how many more rate hikes will happen,” he said, tempering expectations for a concrete timeline. “As things stand today and if nothing dramatically changes, we can say that in 2023 rate hikes will end.”

He also emphasized the persistence of current or potentially higher rates, a measure deemed necessary until inflation approaches the 2% target. “Rates will remain where they are today or higher for some time until inflation comes very close to the 2% target,” he clarified.

BoJ Ueda: Too early to discuss exit strategy from massive stimulus

In an address to parliament today, BoJ Governor Kazuo Ueda stressed that it is premature to debate the specifics about exit strategy from the substantial stimulus program, which includes unloading its extensive holdings of exchange-traded funds.

He asserted that the central bank will discuss the exit strategy from its ultra-accommodative monetary policy and communicate this to the public only when conditions favor achieving stable inflation.

Governor Ueda pointed out that BoJ’s ETF purchases have significantly contributed to bolstering consumption and capital expenditure. “We buy ETFs as part of our massive stimulus programme,” he stated, suggesting that these purchases are critical components of Japan’s broader economic stimulus efforts.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2587; (P) 1.2613; (R1) 1.2648; More…

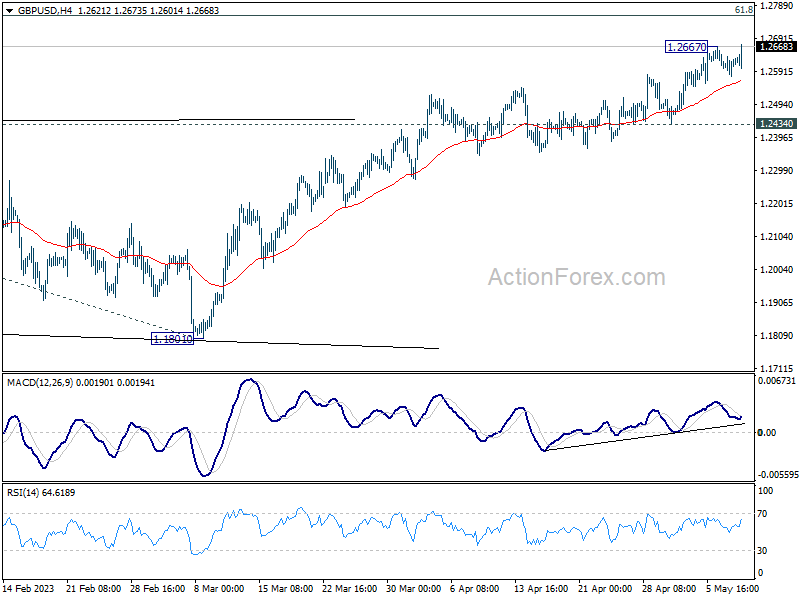

GBP/USD’s up trend resumes by breaking 1.2667 temporary top. Intraday bias is back on the upside. Current rise should now target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. In any case, outlook will remain bullish as long as 1.2434 support holds.

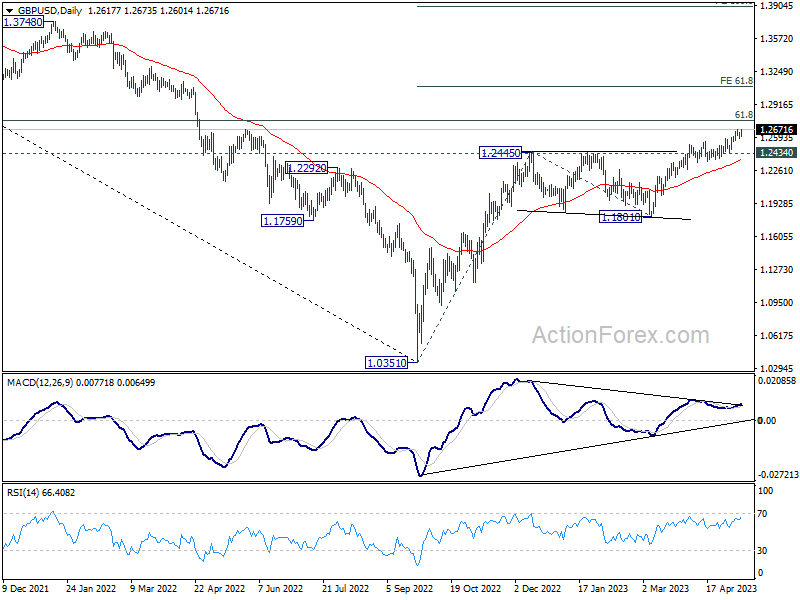

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Mar P | 97.50% | 97.90% | 98.00% | |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.40% | 0.40% | 0.40% | |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 7.20% | 7.20% | 7.20% | |

| 08:00 | EUR | Italy Industrial Output M/M Mar | -0.60% | 0.20% | -0.20% | |

| 12:30 | CAD | Building Permits M/M Mar | 11.30% | 2.30% | 8.60% | |

| 12:30 | USD | CPI M/M Apr | 0.40% | 0.40% | 0.10% | |

| 12:30 | USD | CPI Y/Y Apr | 4.90% | 5.00% | 5.00% | |

| 12:30 | USD | CPI Core M/M Apr | 0.40% | 0.30% | 0.40% | |

| 12:30 | USD | CPI Core Y/Y Apr | 5.50% | 5.50% | 5.60% | 5.50% |

| 14:30 | USD | Crude Oil Inventories | -2.2M | -1.3M |