{kind=link}

With the market still digesting the recent central banks’ announcements, the focus in Australia now shifts to incoming economic data. Next week will give us more information on the consumer sector, with the RBA hoping that these data releases justify its recent surprise rate hike. In the meantime, the aussie would clearly love another push, especially as most of the gains recorded after the May 2 move have evaporated.

RBA probably feels better after various rate hikes globally

The RBA managed to pull a surprise at its most recent meeting by announcing a 25 bps rate hike and keeping the door open for further rate moves. This action was partly a reversal of the April meeting, but in our book, there was sufficient justification for this announcement. The rate hikes that ensued by both the Fed and ECB, and the hawkish commentary from the latter, are bound to have lifted the spirits in the RBA halls.

In the meantime, the statement of Monetary Policy published early on Friday, May 5 gave a bit more insight into the RBA’s decision. The updated forecasts point to inflation at 3%; the upper boundary set by the RBA, in 2025 and thus justifying the recent rate announcement. The market should probably pay more attention to this publication as the overall tone is not conducive to a stop in the rate hiking cycle.

As we are getting close to the peak of the current hiking cycle, central banks are afraid of repeating the famous “rate hike mistake” by Trichet et al in 2008. Therefore, incoming data remain extremely important for the monetary policy outlook, especially as we are clearly entering a critical phase with the market pricing in rate cuts for the key central banks over the next 12-15 months. In the case of the RBA, the market assigns a 40% change for another 25 bps rate increase by August, but then expects almost 53 bps of rate cuts by May 2024.

The consumer sector in the spotlight

The monthly Consumer inflation expectations will be released on Friday, May 12 with the market looking for a small acceleration. This indicator has actually been on an aggressive downwards path since June 2022, but remains elevated at a 4.6% year-on-year change. This recent drop has been captured by the Westpac consumer confidence survey jumping last month to the highest level since October 2020. Another strong set of consumer-related data would offer some early confirmation about the appropriateness of the recent RBA rate hike.

Housing data and business survey kick off the week

The week though starts on an equally high note. The building permits print for March is unlikely to be an easy reading for the RBA as this indicator is flirting with the multi-decade low print recorded in May 2022. The housing sector is the black spot globally, especially in regions like the euro area where the floating rate mortgages dominate the housing market.

Also on Monday, we get another business survey. The NAB business confidence survey has been stabilizing lately in negative territory, but the Business Conditions subcomponent is portraying a more positive picture. This move could be the result of some initial impact from the Chinese reopening, but it is evident that both the market and regional central banks were clearly expecting a stronger impact on their export volumes from China.

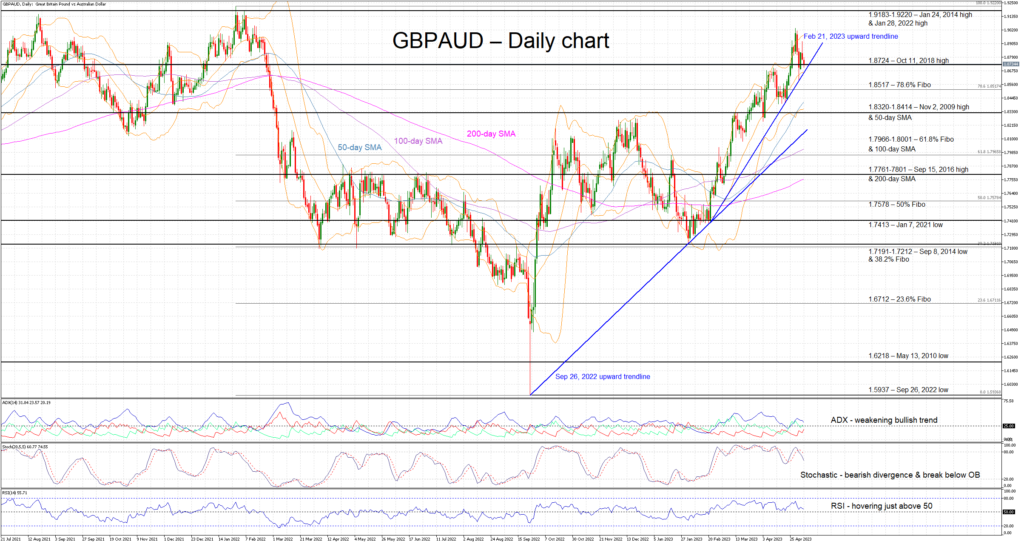

GBPAUD retreating from 15-month high

The aussie has had an interesting week following the RBA surprise announcement on Tuesday, May 2. The GBPAUD pair managed to retreat from the 15-month high, but it has come up against the February 21, 2023 upward sloping trendline. The recent upleg since mid-February has been very aggressive and hence a more sizeable pullback could be on the cards. A positive set of data releases could infuse some confidence into the aussie bears and help them stage a move towards the 1.8517 area.

On the other hand, a combination of weak economic figures and the growing expectations for another rate hike by the BoE on Thursday, 11 May could open the door for a retest of the April highs, and potentially a more convincing move towards the 1.90 area.