{kind=link}

The dollar index remains in defensive for the second straight day as markets await Fed’s decision at the end of two day policy meeting.

The central bank is widely expected to deliver another 25 basis points rate hike, but markets focus on the signals about Fed’s next steps, in light of the current situation, as a number of factors contribute to decision whether to continue policy tightening or to signal a pause, probably until the end of the year.

Inflation in the US continues to ease from its recent peak, but is still too high, while underlying inflation picked up again in March, adding to worries that the worst may not be behind us and keeping pressure on Fed to extend its tightening campaign.

The economy was hit by strong rise in borrowing cost and slowed the activity, but analysts think that the slowdown was not fast enough to push inflation towards 2% target

Conversely, recent weak US economic data, growing tensions in the banking sector and worries that the government could run out of cash after June 1 without further rise in debt ceiling, add to argument that the Fed should be very cautious in making its decision while pressured by two opposite forces.

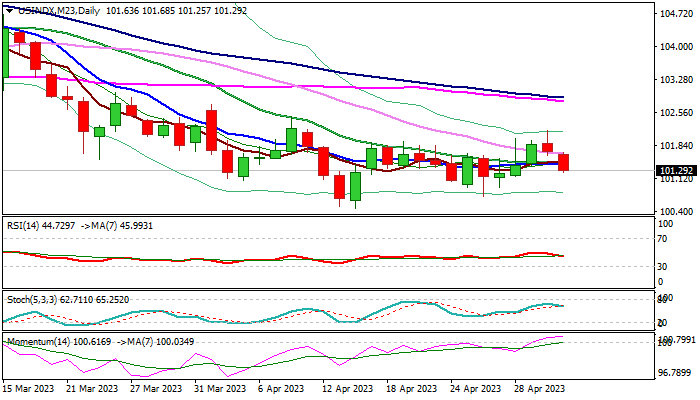

Technical picture on daily chart is weakening as the price fell below converged daily Tenkan-sen / Kijun-sen which remain in bearish setup, RSI declined below neutrality zone, but still strong bullish momentum partially counters negative signals.

Fresh extension lower on Wednesday marked more than 50% retracement of 100.45/102.17 ascend, adding to weak near-term outlook, along with prospect for the third consecutive failure to register weekly close above 101.73 Fibo barrier (23.6% retracement of 105.85/100.45 bear-leg).

Today’s close below Fibo 50% level at 101.31 would add to negative near-term outlook and increase risk of renewed attack at key supports at 100.66/45 (lows of Feb 2/Apr 14).

Alternatively, bounce and close above 101.60 zone (daily Kijun-sen / Asian session high) would ease downside pressure, though extension above Monday’s peak (102.17) is still needed to bring bulls fully in play.

The dollar would react negatively in a widely expected scenario on 25 bps hike today and signal of a pause in tightening cycle, while more hawkish Fed’s stance would offer fresh support to the greenback.

Res: 101.44; 101.60; 101.76; 101.99.

Sup: 101.11; 100.86; 100.66; 100.45.