{kind=link}

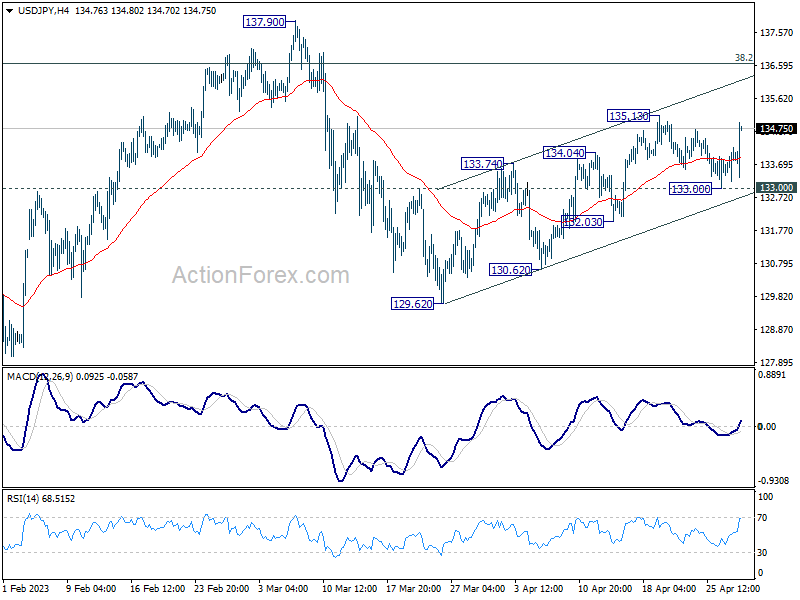

Yen declined broadly in Asian session as traders discovered that BoJ still has the potential to surprise the market with dovish moves. The selloff was triggered by the central bank’s plan to review monetary policy in 12 to 18 months, a major disappointment for those who expected imminent changes as early as at today’s meeting. Additionally, BoJ projects that core inflation will not sustain above target within the projection horizon. Risk-on sentiment, following the strong rebound in US stocks overnight, is another factor pressuring Yen. With the BoJ risk now cleared, bears should be feeling free to act.

At the moment, Australian dollar remains the worst performer for the week, as more analysts anticipate another RBA pause next week. Canadian dollar is the second worst, followed by The Sterling is the best performer, trailed by Euro and New Zealand dollar. While Dollar is recovering today, it remains mixed for the week. The overall picture may change, as Eurozone GDP, Canada GDP, and US PCE inflation data are set to be released today.

Technically, USD/JPY will be a focus in the next few hours, at least before US session. Break of 135.13 will resume the choppy rebound from 129.62. Attention will be on the reaction to the near-term channel resistance (now at around 136.10). Rejection by this resistance will likely keep the rebound corrective and favor a larger decline through 129.62 and 127.20 at a later stage. However, a strong break of the channel resistance will indicate upside acceleration and increase the likelihood of resuming the entire rise from 127.20 through 137.90 resistance.

In Asia, at the time of writing, Nikkei is up 0.80%. Hong Kong HSI is up 0.87%. China Shanghai SSE is up 0.67. Singapore Strait Times is down -0.21%. Japan 10-year JGB yield is down notably by -0.032 at 0.428. Overnight, DOW rose 1.57%. S&P 500 rose 1.96%. NASDAQ rose 2.43%. 10-year yield rose 0.096 to 3.528.

S&P 500 stays near term bullish after biggest rally since Jan

US stocks rebounded strongly overnight with DOW and S&P 500 having the biggest rally since January, and NASDAQ since March. Sentiment was boosted by Meta’s quarterly performance, which shares ended up 14%. The miss in Q1 GDP data also added to hope that Fed is closer to ending the tightening cycle and gave the pessimists some bullets to call for a rate cut before the end of the year if the economy deteriorates further down the road.

Technically, DOW, S&P 500 and NASDAQ all received strong support from their respective 55 D EMA this week. As for SPX, the development keeps the rally from 3808.83 alive. Near term outlook will now stay bullish as long as 4049.35 support holds. Break of 4195.44 resistance will confirm resumption of whole rebound from 3491.58.

The key hurdle remains on 4325.28 cluster resistance (61.8% retracement of 4818.62 to 3491.58 at 4311.69). Sustained break of this cluster resistance will open up further rally back to historical high at 4818.62. The reaction from this 4300 handle will hinge on next week’s FOMC rate decision and Chair Jerome Powell’s press conference.

BoJ stands pat, to take 1-1.5 yrs to review monetary policy

BoJ keeps monetary policy unchanged as widely expected, by unanimous vote. Under the yield curve control, short-term policy interest rate is held at -0.10%. 10-year JGB yield will be kept at around 0% with bond purchases without upper limit. 10-year JGB yield will continue to be allowed to fluctuate in range of around plus and minus 0.50% from 0% level.

The central bank maintained the pledge to continue with Quantitative and Qualitative Monetary Easing with Yield Curve Control for “as long as it is necessary” for meeting inflation target in a “stable manner”. It “will not hesitate to take additional easing measures if necessary”. BoJ will conduct a “broad-perspective review of monetary policy”, with a planned time frame of around 12 to 18 months.

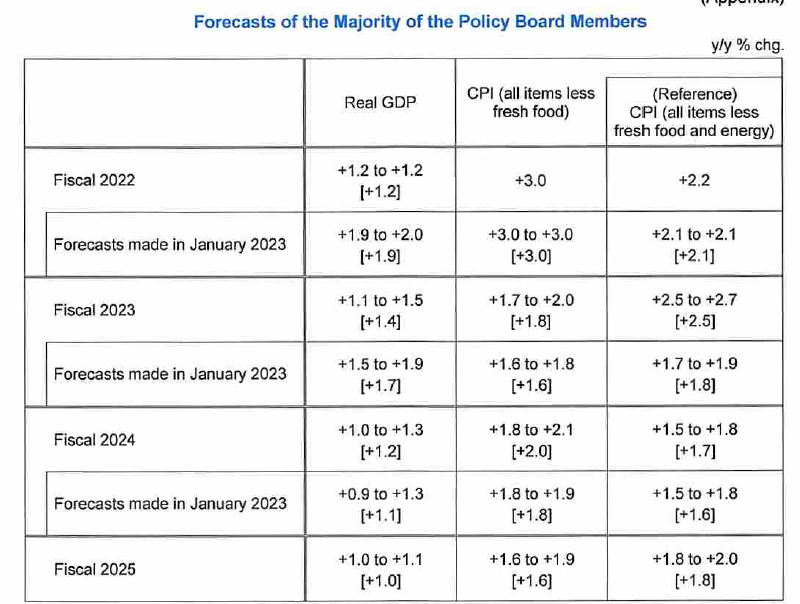

In the new economic projections, while core inflation forecasts were upgraded, it’s not expected to sustain at the 2% level throughout the horizon.

- Real GDP forecasts (versus January estimates):

- Fiscal 2023 at 1.4% (down from 1.7%).

- Fiscal 2024 at 1.2% (up from 1.1%).

- Fiscal 2025 at 1.0% (new)

- CPI Core forecasts (versus January estimates):

- Fiscal 2023 at 1.8% (up from 1.6%).

- Fiscal 2024 at 2.0% (up from 1.8%).

- Fiscal 2025 at 1.6% (new).

- CPI Core-Core forecasts (versus January estimates):

- Fiscal 2023 at 2.5% (up from 1.8%).

- Fiscal 2024 at 1.7% (up from 1.6%).

- Fiscal 2025 at 1.8% (new).

Japan industrial production rose 0.8% mom, with signs of moderate pick up

Japan’s industrial production expanded for the second consecutive month, recording a 0.8% mom growth in March, surpassing the expected 0.4% mom increase. The growth was driven by output in eight sectors, led by motor vehicles, while declines were observed in seven sectors, including electronic components and devices.

The Ministry of Economy, Trade and Industry upgraded its basic assessment for the month, stating that industrial production was “showing signs of moderately picking up” as parts supply shortages continued to ease. This is a marked improvement from the previous month’s assessment of “weakening.” The ministry also projects a further 4.1% growth in industrial production for April and a -2.0% decline in May.

Other economic indicators released include 7.2% yoy increase in retail sales for March, surpassing expectations of 6.5% yoy. However, unemployment rate rose for the second month in a row, reaching 2.8%, above expectation of 2.5%.

April, Tokyo core CPI, which excludes fresh food, accelerated from 3.2% to 3.5% yoy, exceeding expectations of 3.2% yoy. Core-core CPI, which excludes fresh food and fuel costs, accelerated from 3.4% to 3.8% year-on-year, marking the highest rate since April 1982.

Looking ahead

GDP data from Eurozone, Germany and France are the main focuses in European session. Germany will also publish CPI flash. Swiss will release retail sales and KOF economic barometer. Later in the day, Canada GDP, US personal income and spending with PCE inflation will be the main focuses.

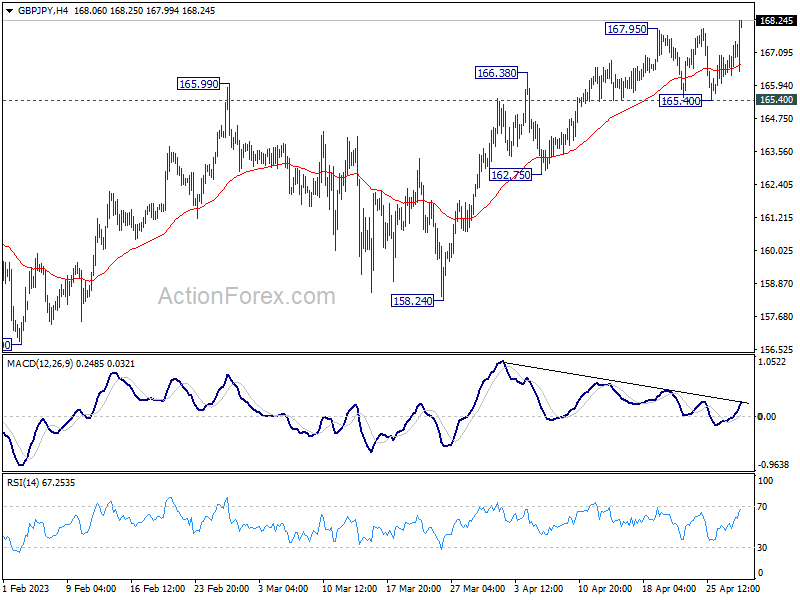

GBP/JPY Daily Outlook

Daily Pivots: (S1) 166.66; (P) 167.09; (R1) 167.85; More…

GBP/JPY’s rally resumed by breaking through 167.95 resistance an intraday bias is back on the upside. Current rise from 155.33 should target 169.26 resistance first, and then 172.11 high. For now, near term outlook will remain cautiously bullish as long as 165.40 support holds, in case of retreat. However, firm break of 165.40 will argue that the corrective pattern from 172.11 is starting another falling leg. Intraday bias will be back on the downside for 162.75 support and below.

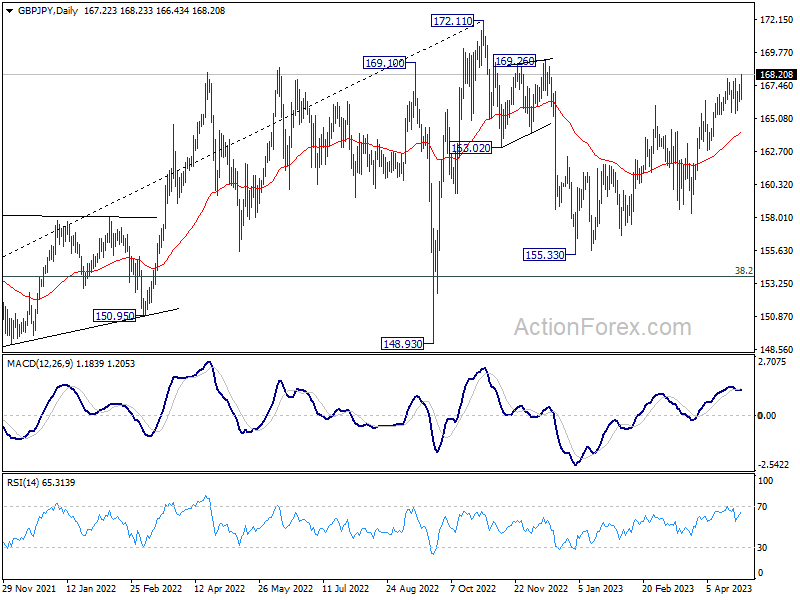

In the bigger picture, as long as 38.2% retracement of 123.94 (2020 low) to 172.11 (2022 high) at 153.70 holds, medium term bullishness is retained. That is, larger up trend from 123.94 (2020 low) is still in progress. Break of 172.11 high to resume such up trend is expected at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Apr | 3.50% | 3.20% | 3.20% | |

| 23:50 | JPY | Industrial Production M/M Mar P | 0.80% | 0.40% | 4.60% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | 7.20% | 6.50% | 6.60% | 7.30% |

| 23:30 | JPY | Unemployment Rate Mar | 2.80% | 2.50% | 2.60% | |

| 01:30 | AUD | Private Sector Credit M/M Mar | 0.30% | 0.30% | 0.30% | |

| 01:30 | AUD | PPI Q/Q Q1 | 1.00% | 1.50% | 0.70% | |

| 01:30 | AUD | PPI Y/Y Q1 | 5.20% | 5.80% | 5.80% | |

| 04:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Mar | -3.2% | -3.70% | -0.30% | |

| 05:30 | EUR | France GDP Q/Q Q1 P | 0.10% | 0.10% | ||

| 06:00 | EUR | Germany Import Price Index M/M Mar | -0.90% | -2.40% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Mar | 0.40% | 0.30% | ||

| 07:00 | CHF | KOF Leading Indicator Apr | 98 | 98.2 | ||

| 07:55 | EUR | Germany Unemployment Change Mar | 10K | 16K | ||

| 07:55 | EUR | Germany Unemployment Rate Mar | 5.60% | 5.60% | ||

| 08:00 | EUR | Italy GDP Q/Q Q1 P | 0.20% | -0.10% | ||

| 08:00 | EUR | Germany GDP Q/Q Q1 P | 0.10% | -0.40% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.10% | 0.00% | ||

| 12:00 | EUR | Germany CPI M/M Apr P | 0.60% | 0.80% | ||

| 12:00 | EUR | Germany CPI Y/Y Apr P | 7.30% | 7.40% | ||

| 12:30 | CAD | GDP M/M Feb | 0.20% | 0.50% | ||

| 12:30 | USD | Personal Income M/M Mar | 0.20% | 0.30% | ||

| 12:30 | USD | Personal Spending Mar | -0.10% | 0.20% | ||

| 12:30 | USD | PCE Price Index M/M Mar | 0.30% | 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Mar | 4.60% | 5.00% | ||

| 12:30 | USD | Core PCE Price Index M/M Mar | 0.30% | 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 4.50% | 4.60% | ||

| 12:30 | USD | Employment Cost Index Q1 | 1.10% | 1.00% | ||

| 13:45 | USD | Chicago PMI Apr | 43.7 | 43.8 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | 63.5 | 63.5 |