{kind=link}

The Bank of Japan will hold its first policy meeting under the stewardship of Kazuo Ueda next week, although it’s looking unlikely that he will kick things off with a bang. The focus may therefore quickly shift to GDP numbers out of the United States and Eurozone where both economies are expected to have dodged a recession, while the all-important PCE inflation report will be one of the final pieces of the rate puzzle before the Fed’s May decision.

Ueda to play it safe at his first meeting

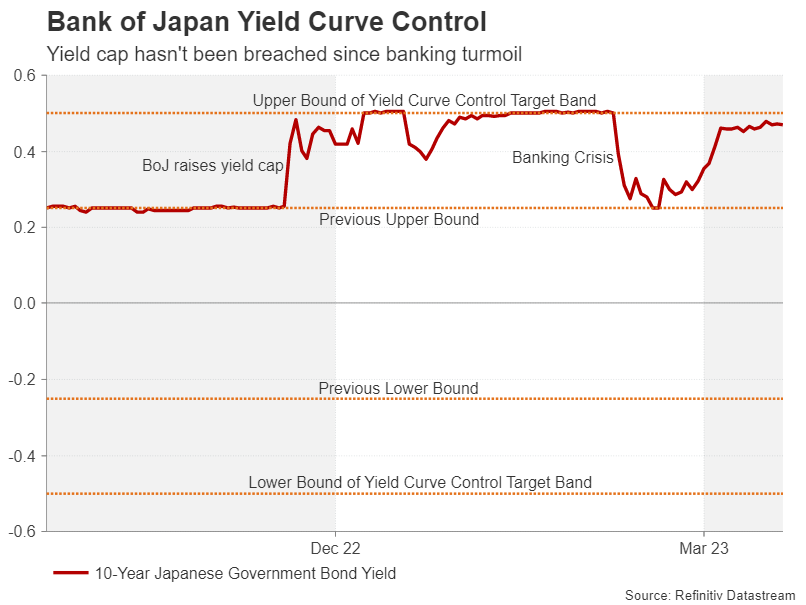

The banking crisis may have been a blessing in disguise for the Bank of Japan as the turmoil sent Japanese government bond (JGB) yields diving, taking the pressure off policymakers to make any imminent tweaks to their controversial yield curve control policy. The 10-year yield, which the BoJ aims to keep below 0.50%, has not breached this cap since the crisis first unfolded.

However, most market participants see it as only a matter of time before the Bank makes further adjustments to rein in its ultra-accommodative policies even though inflation now appears to be on the way down. If as expected, Ueda delivers no surprises in his inaugural meeting on Friday and keeps all of the BoJ’s monetary policy settings unchanged, investors will be hunting for clues about the timing of any possible tweak.

Ueda has so far not strayed too far from his predecessor’s stance, signalling that he wants to see stronger wage growth before altering the policy course. However, his tone on achieving this goal has been somewhat more optimistic and he may use his first post-meeting press conference to lay the groundwork for eventually phasing out yield curve control.

The Bank will also be publishing an updated set of quarterly projections, thus, the forecast on inflation will also guide the markets on where policy might be headed. In addition, there’s a barrage of Japanese economic indicators on the agenda too, the majority of which are due on Thursday and will include April CPI figures for Tokyo, preliminary industrial production readings, as well as retail sales and jobs stats.

The yen may not necessarily react much to the data but should Ueda hint at some kind of a change later in the year, the currency is likely to gain versus its peers.

Eurozone GDP probably rebounded mildly in Q1

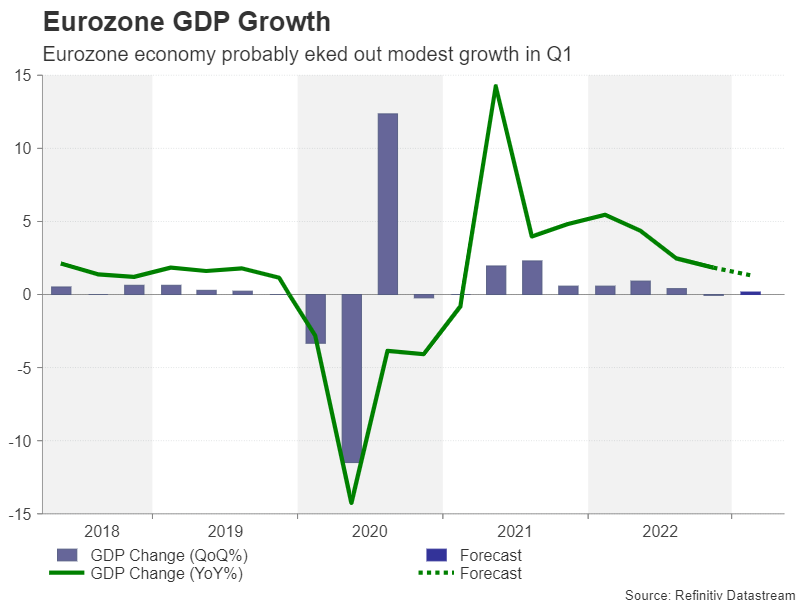

The Eurozone economy grinded to a halt at the end of last year, but it’s expected to have eked out modest growth in the first three months of 2023. Lower fuel prices and a relatively mild winter that didn’t leave households completely out of pocket likely helped the euro area avoid a recession, at least for now. The flash GDP estimates out on Friday are forecast to show GDP rising by 0.2% over the quarter.

That’s not exactly cause for a huge celebration, but the outlook has improved dramatically from a few months ago, or even more recently when there was a real threat of the bank collapses in the US and Switzerland having a domino effect on Eurozone banks.

A notable miss in the GDP print might make the European Central Bank more hesitant about hiking rates by 50 basis points at its May meeting, whereas a bigger rebound would probably remove any doubts about going big.

However, ECB policymakers will also be monitoring the flash CPI figures out of Germany and France due the same day. The Eurozone-wide numbers will be released a few days later but Friday’s sneak peek still has the capacity to move the markets as a 50-bps move is only 30% priced in.

Should those odds creep up, the euro could climb higher as it fights to make a clear break above the $1.10 level.

PCE inflation to lead data-packed week in the US

Fed officials will be staying mum over the coming week as they enter the blackout period ahead of the May 2-3 policy meeting. However, there’s plenty on the US economic agenda that should provide some last-minute guidance as to what to expect from the Fed.

Starting things off is the consumer confidence index for April on Tuesday along with March new home sales. Durable goods orders will follow on Wednesday, but the first top tier release will land on Thursday with the advance estimate of Q1 GDP.

The American economy is expected to have expanded by an annualized pace of 2.0% over the period, which would imply that a recession is not imminent. Pending home sales are also due the same day.

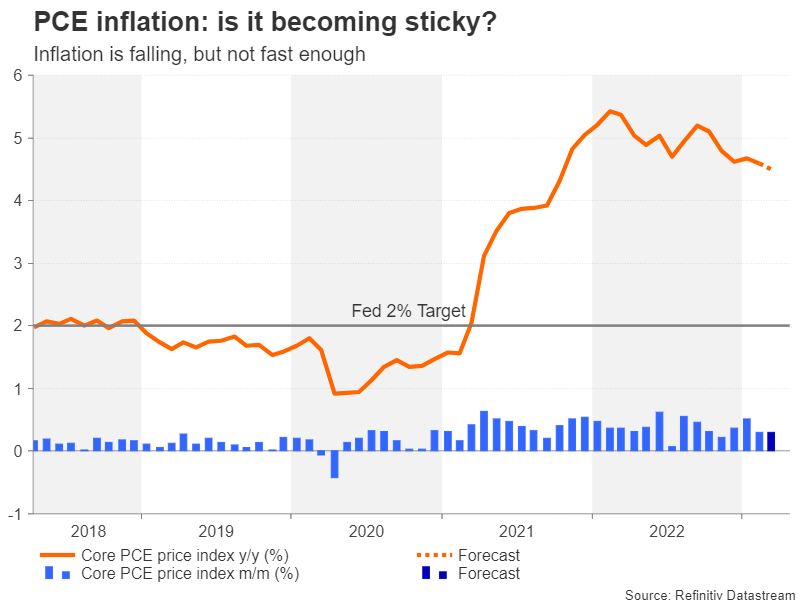

The second highlight will be Friday’s personal income and outlays report that contains the all-important core PCE price index as well as consumption figures. Other data on Friday will include quarterly wages and the Chicago PMI.

Although the Fed’s favourite price gauge has moderated significantly from its high of 5.4% in 2022, the downward progress has slowed in recent months. The core PCE price index is forecast to have edged down slightly to 4.5% y/y in March.

It is almost certain that the Fed will hike rates by 25 bps in March, but a bigger increment is highly unlikely. Nevertheless, a hotter-than-expected reading would reduce the chances of the Fed pausing in May, especially if the incoming data is overall positive.

The bigger question is whether the US dollar can enjoy a meaningful boost from a stronger set of numbers. Investors remain convinced the Fed will begin cutting rates in the second half of 2023 while other key central banks potentially remain on a hiking path.

So the data alone may not do much in tempering those dovish bets and the dollar may struggle to attract much upside unless Fed Chair Powell does a more convincing job of ratcheting up his hawkish rhetoric.

Inflation on tap in Australia

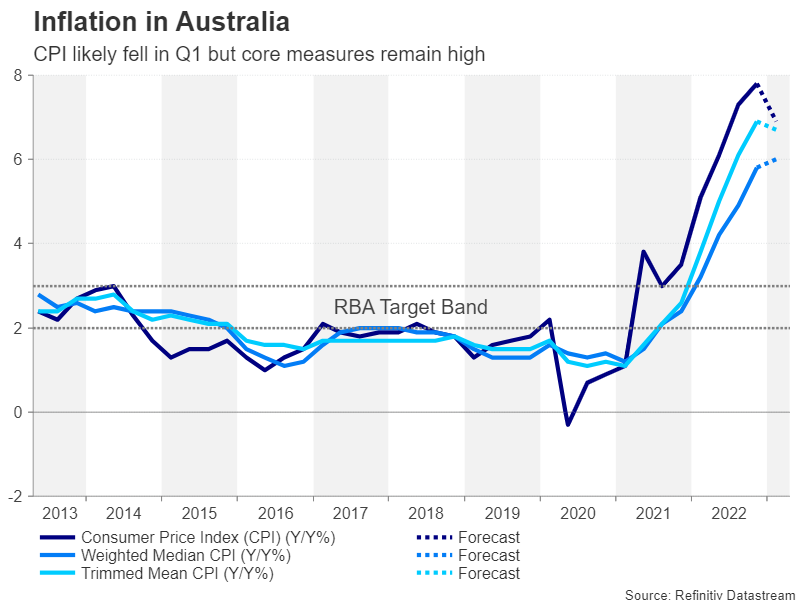

The Australian dollar regained some bullish impetus from the Reserve Bank of Australia’s latest meeting minutes that revealed that the decision to pause rate hikes was a close call. However, Wednesday’s CPI report might see some of those revived hawkish bets being wound back as inflation likely eased in the fourth quarter of 2022.

The headline rate of CPI reached a three-decade high of 7.8% at the end of 2022 but is expected to have fallen back to 6.9% in the first quarter of 2022. The March print is also due and investors will be watching to see if CPI continued to decline after the sharp drops in January and February, as well as keeping an eye on the core measures, which are only published quarterly.

If the latest price gauges reinforce the picture of subsiding inflationary pressures, the aussie might slip back against its US counterpart.