{kind=link}

Japanese Yen rose broadly in today’s Asian trading session following the release of CPI data, indicating inflation remains persistently above BoJ’s target. While it is still early for BoJ to make any changes to monetary policy, a case for a shift later this year is building. Meanwhile, Dollar and Euro are firmer in relatively quiet trading.

Overall sentiment is slightly risk-off, with Australian Dollar leading other commodity currencies lower. Canadian Dollar is also spiraling down alongside oil prices. Sterling the Swiss franc are currently mixed. Market focus will shift to PMI data from the UK, Eurozone, and the US, as well as Canada’s retail sales report.

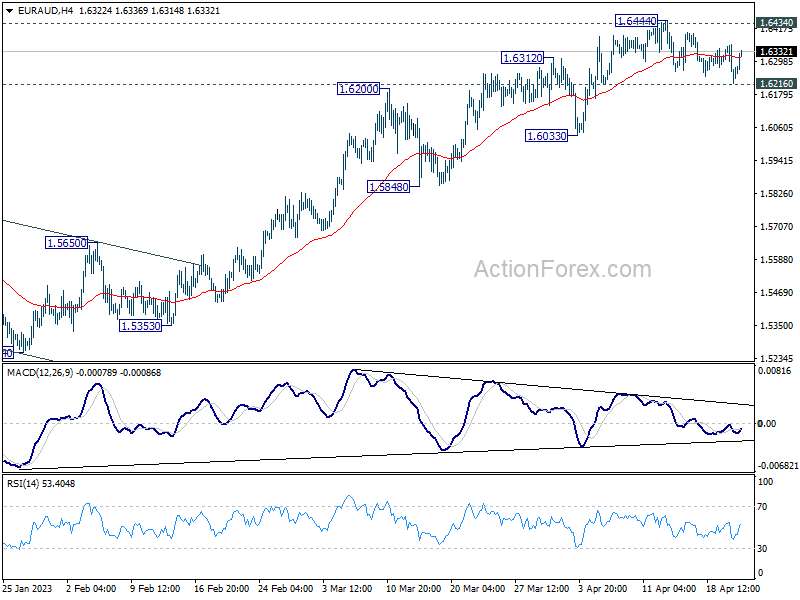

Technically, significant buying emerged in EUR/AUD as it approached a minor support level at 1.6216, keeping the near-term outlook bullish. Focus will return to the 1.6444 temporary top, which coincides with the 1.6434 long-term resistance (2021 high). A decisive break there will add to the case for long-term bullishness in the cross. Simultaneously, AUD/USD could also move in tandem with the Aussie selloff, potentially breaking the 0.6619 support level and reaching 0.6563 low.

In Asia, at the time of writing, Nikkei is down -0.24%. Hong Kong HSI is down -1.09%. China Shanghai SSE is down -1.40%. Singapore Strait Times is down -0.29%. Overnight, DOW dropped -0.33%. S&P 500 dropped -0.60%. NASDAQ dropped -0.80%. 10-year yield dropped -0.057 to 3.545.

Fed’s Mester foresees further tightening to ensure downward trajectory of inflation

Cleveland Federal Reserve President Loretta Mester emphasized the need for further tightening in monetary policy to ensure a “sustained downward trajectory” of inflation. She pointed out that “demand is still outpacing supply in both product and labor markets and inflation remains too high.”

To tackle the persistent inflation, Mester suggested that monetary policy will need to “move somewhat further into restrictive territory”, with fed funds rate “moving above 5%” and “real fed funds rate staying positive for some time”. However, she also acknowledged that the tightening journey is closer to its end than the beginning, with future rate decisions being dependent on the economy’s performance.

Mester expects the unemployment rate to rise to between 4.5% and 4.75% and inflation to ease to 3.75% this year. She projects that inflation will reach the central bank’s 2% target by 2025. In response to an audience question, Mester emphasized the Fed’s aim for a “soft landing” and mentioned that she expects slow growth, well below 1%, in the current economic environment.

Fed’s Harker: Some additional tightening may be needed

Philadelphia Fed President Patrick Harker has indicated that “some additional tightening may be needed to ensure policy is restrictive enough to support both pillars of our dual mandate.” Harker expects that once this point is reached, which he believes should happen this year, the Fed will “hold rates in place and let monetary policy do its work”.

Harker also noted that the economy remains strong and inflation is coming down, albeit slowly. He projected that inflation, currently at a 5% annualized rise in the personal consumption expenditures price index, would fall to 3% to 3.5% this year and reach 2% in 2025. The unemployment rate, currently at 3.5%, is expected to move up to around 4.4% this year amid tepid growth.

The bank president acknowledged the impact of last month’s financial sector woes on the economy, stating that “it will take some time to evaluate how recent events may impact overall economic activity and inflation.” Harker added that he expects to see tighter credit conditions for households and businesses, which may slow economic activity and hiring, but the full extent of this impact is still unclear.

Fed officials highlight the need for further action to tame inflation

Atlanta Fed President Raphael Bostic, Dallas Fed President Lorie Logan, and Fed Governor Michelle Bowman have all expressed concerns over the persistently high inflation rate.

Bostic, speaking on CNBC, said that “one more move should be enough for us to then take a step back and see how our policy is flowing through the economy, to understand the extent to which inflation is returning back to our target.” He acknowledged that inflation has been much too high, with Fed having raised interest rates by 4.5 percentage points over the past year in an attempt to bring the economy into better balance.

Lorie Logan emphasized the need for sustained improvement in inflation statistics, an economy evolving as forecast, and a change in the factors underlying inflation, such as the hot labor market and imbalance in supply and demand. She reiterated the concern, stating, “As you surely know, inflation has been much too high.”

Bowman also highlighted the importance of the Fed’s focus on lowering inflation. She said, “Lately, as you know, the Fed has been focused on lowering inflation, which is essential if we want to support a growing economy and rising incomes.” Bowman added, “We clearly need to continue to work to bring inflation down.”

BoE Tenreyro: We may already have tightened too much

BoE MPC member Silvana Tenreyro, a known dove, said interest rates have already been raised more than enough.

“The shape of the inflationary shock stemming mostly from the large increase in energy prices, coupled with the long lags with which monetary policy affects the economy, means that the most likely scenario now is that we undershoot the inflation target in the medium term, meaning 2025,” Tenreyro said.

“Given policy lags, policy needs to be based on forward looking forecasts and those forecasts at least for the UK are telling us that we may already have tightened too much.”

Those who want to keep raising rates she likened to Milton Friedman’s “fool in the shower.” “When the fool starts the water and it runs cold, he keeps turning the faucet and, eventually, because he’s impatient, he gets burned,” she said.

Australian PMIs reveal divergence between manufacturing and services, RBA rate hike likely in May

Australia’s April PMI Manufacturing has dropped to a 35-month low at 48.1, down from 49.1, while PMI Services jumped to a 10-month high of 52.6, up from 48.6. The PMI Composite also reached a 10-month high at 52.2. The data reveals a growing divergence between the performance of Australia’s manufacturing and service sectors.

Warren Hogan, Chief Economic Advisor at Judo Bank, said, “Manufacturing activity remains soft, a reflection of weaker demand for goods and a gradual slowdown in construction activity in Australia. The April flash results for the services sector have bounced strongly, bringing into question the broader economic slowdown.”

Hogan dismissed the idea of a recession, stating that the results point to a lift in Australia’s economic momentum through mid-2023. However, he noted that the risk to inflation is from excess demand in the economy, putting upward pressure on domestic prices in energy, housing, and labor markets.

With the RBA Board set to meet in early May, Hogan believes the April flash PMI, strong employment outcomes in March, and a resurgence in parts of the housing market all suggest that another 25bp rate hike in May is more likely than not, depending on the March quarter CPI to be released on April 26th.

Japan PMIs: Private sector expands driven by resurgent service economy

Japan’s PMI Manufacturing in April slightly rose from 49.2 to 49.5, missing expectations of 49.9. PMI Services experienced a slight drop from 55.0 to 54.9, while PMI Composite fell from 52.9 to 52.5. Despite this, the country’s private sector continued to expand solidly at the beginning of Q2, with the service economy’s resurgence helping to offset the weak manufacturing sector performance.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said, “Inflows of total new business increased at the quickest pace for nearly a year-and-a-half as services companies registered a steep upturn in sales amid reports of stronger demand conditions and improved customer numbers.” Fiddes also noted signs of cost pressures easing, with overall input costs rising to the weakest extent in 15 months in April.

Regarding the year-ahead outlook, optimism in the service sector hit a record high in April, but weakened among manufacturers. While service providers anticipate further improvements in demand and operating conditions as the impact of COVID-19 fades, some manufacturers expressed concerns over the economic outlook, rising costs, and component shortages.

Japan’s CPI core unchanged at 3.1%, core-core at highest since 1981

Japan’s CPI growth slowed from 3.3% yoy to 3.2% yoy, exceeding the expected 2.6% yoy increase. The CPI core (all items excluding food) remained unchanged at 3.1% yoy, in line with expectations. The CPI core-core (all items excluding food and energy) accelerated from 3.5% yoy to 3.8% yoy, surpassing the anticipated 3.4% yoy figure. This marks the 10th consecutive uptick and the highest level since December 1981.

New BOJ Governor Kazuo Ueda has recently committed to maintaining ultra-loose monetary policy. While no major changes to the bond yield control policy are expected at Ueda’s first policy-setting meeting next week, the spreading inflation from energy to the broader economy may keep market expectations alive that BOJ could begin phasing out its massive stimulus later this year. However, this will depend on whether wages increase sustainably and support consumption.

Looking ahead

UK PMIs, as well as Eurozone PMIs are the main focus in European session. Later in the day, Canada will release retail sales while US will also publish PMIs.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 146.91; (P) 147.38; (R1) 147.73; More….

A temporary top is in place at 147.85 in EUR/JPY ahead of 148.38 high. Intraday bias is turned neutral first. Further rally will remain mildly in favor as long as 145.66 resistance turned support holds. Decisive break of 148.38 will resume larger up trend to 149.75 long term resistance. However, firm break of 145.66 will indicate that corrective pattern from 148.38 has started the third leg. Intraday bias will be back on the downside for 142.53 support first and possibly below.

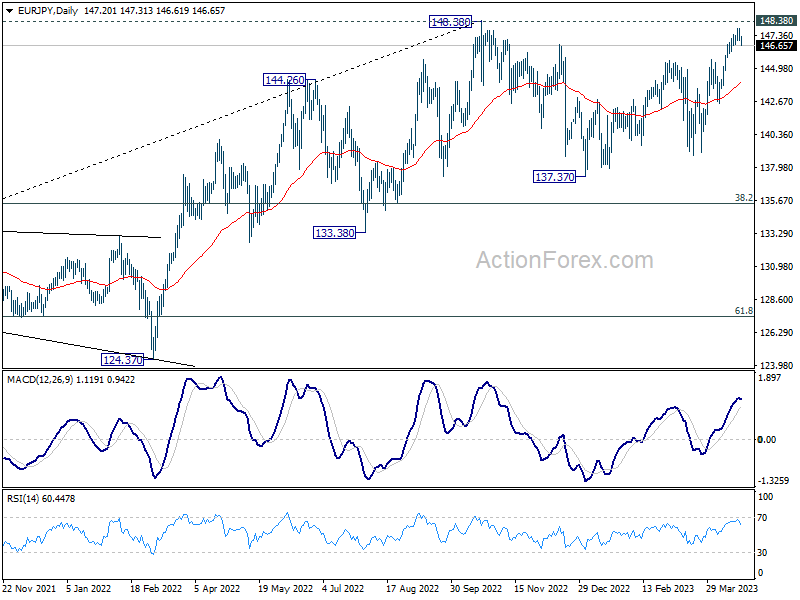

In the bigger picture, as long as 55 W EMA (now at 140.44) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance. Decisive break there will resume long term up trend. However, sustained break of 55 W EMA will bring deeper fall to 38.2% retracement of 114.42 to 148.38 at 135.40.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Apr P | 48.1 | 49.1 | ||

| 23:00 | AUD | Services PMI Apr P | 52.6 | 48.6 | ||

| 23:01 | GBP | GfK Consumer Confidence Apr | -30 | -35 | -36 | |

| 23:30 | JPY | National CPI Y/Y Mar | 3.20% | 2.60% | 3.30% | |

| 23:30 | JPY | National CPI Core Y/Y Mar | 3.10% | 3.10% | 3.10% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Mar | 3.80% | 3.40% | 3.50% | |

| 00:30 | JPY | Manufacturing PMI Apr P | 49.5 | 49.9 | 49.2 | |

| 00:30 | JPY | Services PMI Apr P | 54.9 | 55 | ||

| 06:00 | GBP | Retail Sales M/M Mar | -0.90% | -0.50% | 1.20% | 1.10% |

| 06:00 | GBP | Retail Sales Y/Y Mar | -3.10% | -3.10% | -3.50% | |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Mar | -1% | -0.70% | 1.50% | 1.40% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Mar | -3.20% | -3.10% | -3.30% | -3.00% |

| 07:15 | EUR | France Manufacturing PMI Apr P | 47.5 | 47.3 | ||

| 07:15 | EUR | France Services PMI Apr P | 53.6 | 53.9 | ||

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 45.6 | 44.7 | ||

| 07:30 | EUR | Germany Services PMI Apr P | 53.5 | 53.7 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 48.2 | 47.3 | ||

| 08:00 | EUR | Eurozone Services PMI Apr P | 54.6 | 55 | ||

| 08:30 | GBP | Manufacturing PMI Apr P | 48.8 | 47.9 | ||

| 08:30 | GBP | Services PMI Apr P | 52.9 | 52.9 | ||

| 12:30 | CAD | Retail Sales M/M Feb | -0.60% | 1.40% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | 0.00% | 0.90% | ||

| 13:45 | USD | Manufacturing PMI Apr P | 49.2 | 49.2 | ||

| 13:45 | USD | Services PMI Apr P | 51.8 | 52.6 |