{kind=link}

Investors will be exploring Japan’s CPI inflation report during Friday’s Asian session in order to get clarity on whether inflation is persisting enough to provoke a tweak in the super accommodative monetary policy. Forecasts are for steady growth after February’s downturn from multi-decade highs, though investors will be on alert for any surprises, which could signal changes in monetary guidance, generating fresh volatility in the yen.

BoJ to stay on course but not for long

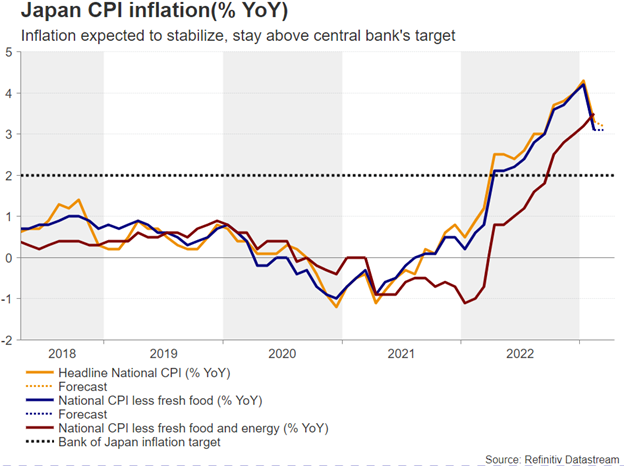

Headline inflation rose at its fastest pace since the end of 1990 in January, while the core measure, which excludes food and energy prices, hit the highest since the 1980s, fueling speculation that the Bank of Japan (BoJ) could soon end its ultra-easy monetary strategy. Despite investors debating over a potential hawkish policy tweak, the BoJ has been bravely dialling down expectations for a hawkish rotation even if its major counterparts are well ahead in the tightening cycle.

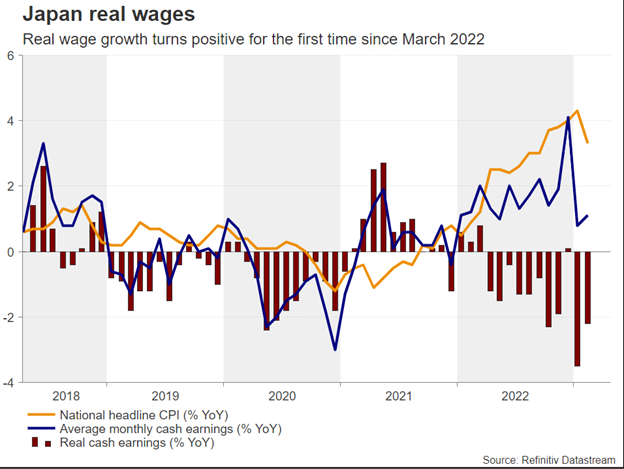

The departure of former BoJ governor Haruhiko Kuroda, who was the first to kick off the aggressive monetary easing strategy a decade ago, did not alter the central bank’s language. Instead, his successor Kazuo Ueda affirmed that current ultra-easy settings are appropriate in the meantime as a sustained achievement of the 2.0% inflation target has yet to be achieved. Neither has nominal wage growth climbed sustainably above 3.0% as the central bank desires, although spring wage talks with unions and businesses promised increases of around 5.0% from April onwards, with real wage growth remaining negative at -2.2% y/y at the moment.

As a result, market pricing for a rate hike at next week’s policy meeting and till September remains zero. On the other hand, commentary on the controversial yield curve control, which aims to keep the 10-year bond yield around 0.5%, has been more ambiguous, with polls showing that scrapping yield curve control is the second most popular choice among investors after a tweak in policy guidance.

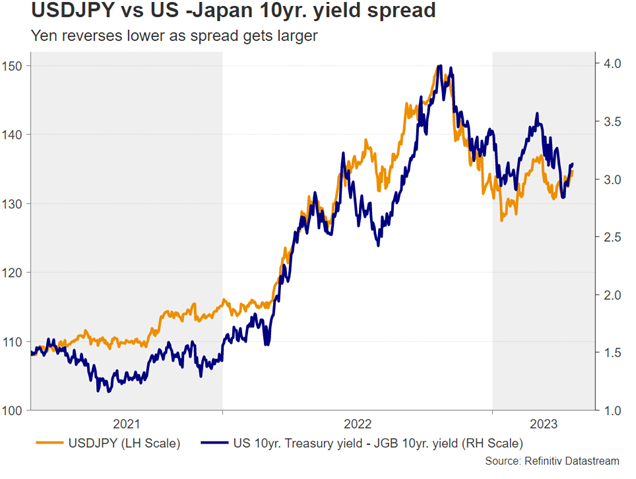

That probably comes as evidence from previous months showed that even under massive policy easing domestically in Japan, yields can still go higher if foreign central banks are raising rates. Perhaps it’s a tool worth keeping for now as GDP growth figures are not that great in Japan and global recession risks loom. However, with major peers such as the Fed unwilling to reverse monetary policy in the face of inflation, the BoJ may have a tough time in sustaining the cap through massive bond buying, with the domestic currency also suffering from negative side effects.

CPI inflation

On Friday it would be interesting to see if Japan’s headline CPI inflation inched lower to 3.2% y/y from 3.3% previously and 4.3% y/y in February without the central bank’s aid as forecasts suggest. The core measure, which excludes volatile food and energy prices, is expected to stabilize at 3.1% y/y. If that proves to be the case or the figures head lower, pressure for a policy change may soften. Alternatively, a new inflation upturn before businesses raise wages as pledged could increase criticism on the current accommodative settings during the April 28 gathering.

USD/JPY

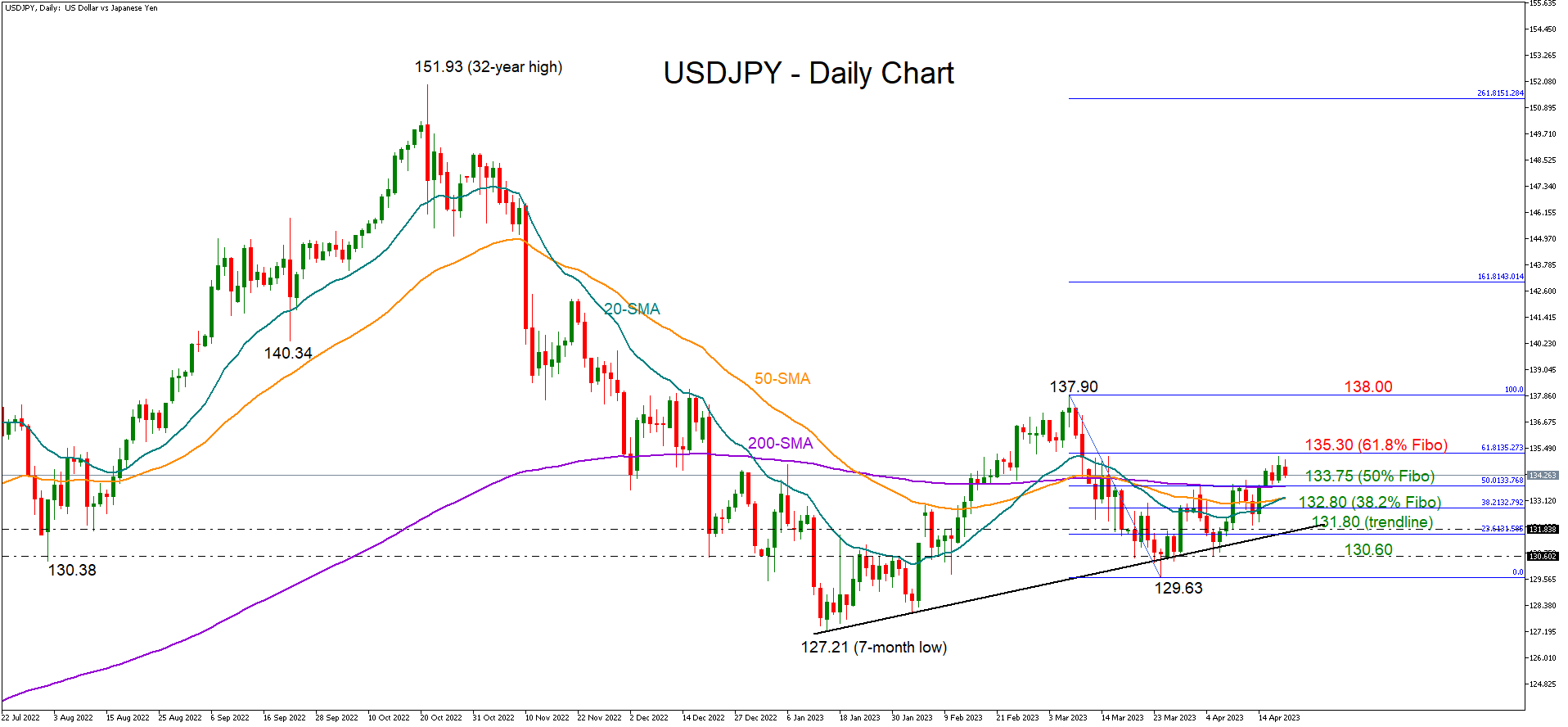

As regards the market reaction, a notable upside deviation from forecasts could help the yen regain some lost ground. Looking at USD/JPY, the 200-day simple moving average (SMA) could immediately come under the spotlight at 133.75. Breaking that base, the price may pause near 132.80 before heading for the key support trendline seen at 131.80.

Alternatively, weaker-than-expected readings may back “Abenomics” policies, which many members of the ruling LDP party are still endorsing. The spread between the 10-year US and Japan government bond yields could maintain its latest upturn, helping the dollar to breach the 135.30 resistance and rally towards the March high of 137.90.