{kind=link}

Forex markets are currently navigating a landscape of uncertainty, as mixed currency performance contributes to a lack of clear direction. Dollar has experienced a decline in Asian session, but still hovers within familiar boundaries against other major currencies. Meanwhile, Euro has managed to strengthen against the greenback but appears less robust in other pairs.

Yen, on the other hand, has emerged as a strong contender for the day, recouping some of its yesterday’s pullback. In addition, Sterling has found firmer footing after BoE Governor Andrew Bailey’s remarks indicated that the Monetary Policy Committee can concentrate on inflation while the Financial Policy Committee maintains financial stability. Interestingly, Australian Dollar has managed to hold its ground despite disappointing retail sales data.

Looking ahead, the market may experience subdued trading due to a relatively light economic calendar. However, the upcoming release of US consumer confidence data could introduce an element of volatility, as traders and investors alike look for potential opportunities in the midst of uncertainty.

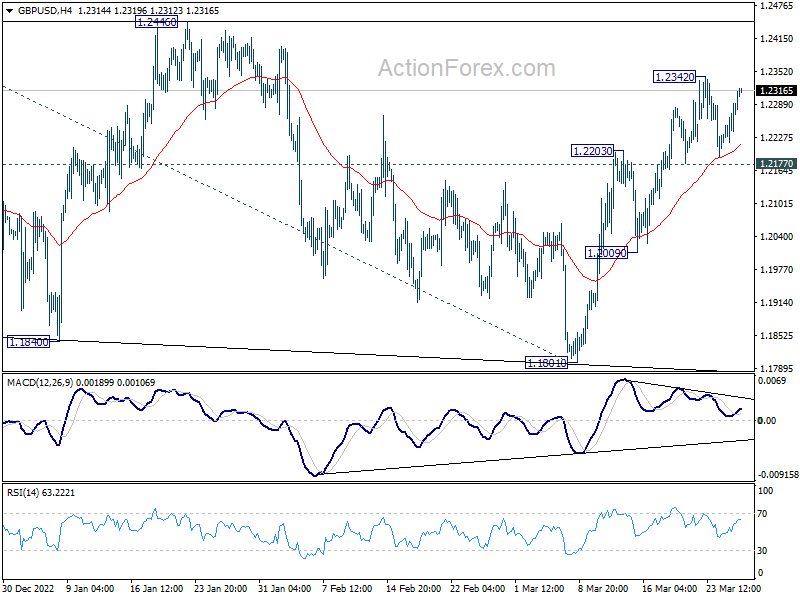

Technically, GBP/USD could now be eyeing 1.2342 temporary top with this week’s rebound. Break there will resume the near term rally to 1.2445/6 resistance zone. Decisive break there will resume larger up trend from 1.0351 (2022 low) to 1.2759 fibonacci level. Let’s see if the Pound has enough buying to back the breakout.

In Asia, at the time of writing, Nikkei is up 0.15%. Hong Kong HSI is up 1.37%. China Shanghai SSE is up 0.18%. Singapore Strait Times is up 0.73%. Japan 10-year JGB yield is up 0.0220 at 0.317. Overnight DOW rose 0.60%. S&P 500 rose 0.16%. NASDAQ dropped -0.47%. 10-year yield rose 0.148 to 3.528.

Fed Jefferson on balancing inflation and economic stability

Fed Philip Jefferson stated yesterday that the current inflation rate is too high, emphasizing the FOMC’s goal to reduce it to 2% as quickly as possible. Speaking at Washington and Lee University in Lexington, Virginia, he acknowledged that the process may take some time due to persistent inflation components such as services excluding housing.

Jefferson said, “I would like to say that inflation will return to 2% soon, but we have to do it in a way that does not damage the economy any more than is necessary. That’s what we are trying to do.” Fed is grappling with the challenge of ensuring price stability amid high inflation while also maintaining financial stability in the wake of the second-largest bank failure in US history.

In his speech, Jefferson also noted that although inflation has begun to decline, it remains unclear whether this decrease is due to higher interest rates, easing pandemic-induced supply strains, or falling energy prices.

He highlighted the uncertainty surrounding the full impact of the Fed’s tightening measures, saying, “Monetary policy affects the economy and inflation with long, variable, and highly uncertain lags, and we are still learning about the full effect of our tightening thus far.”

Australia retail sales turnover up 0.2% mom in Feb, appeared to have levelled out

Australia retail sales turnover rose 0.2% mom to AUD 35.14B in February, matched expectations. Through the year, retail sales rose 6.4% yoy.

Ben Dorber, ABS head of retail statistics, said retail sales rose modestly in February and appear to have levelled out after a period of increased volatility over November, December and January.

“On average, retail spending has been flat through the end of 2022 and to begin the new year.”

Retail turnover rose modestly across most of the states and territories, with rises at 1.0% or less. Queensland recorded the only fall in turnover, down -0.4%.

Looking ahead

BOE will release quarterly bulletin. Later in the day, US will publish goods trade balance, housing index and consumer confidence.

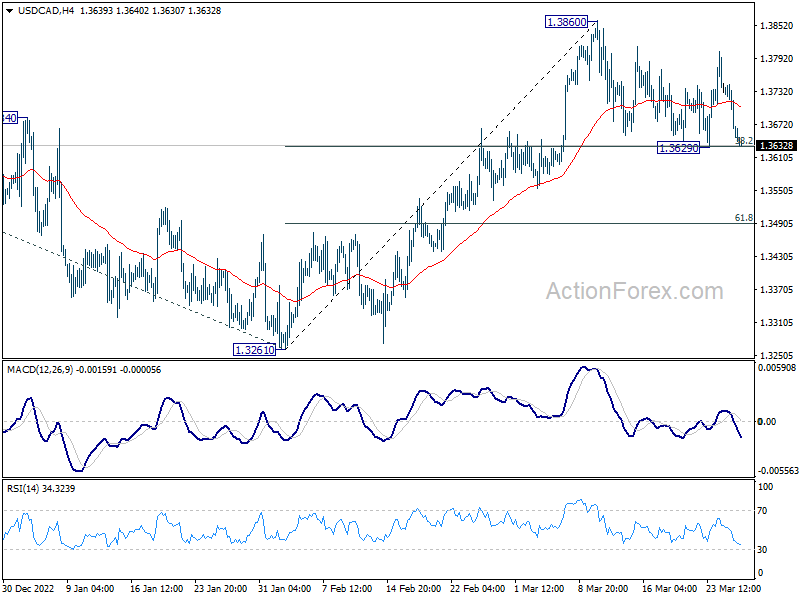

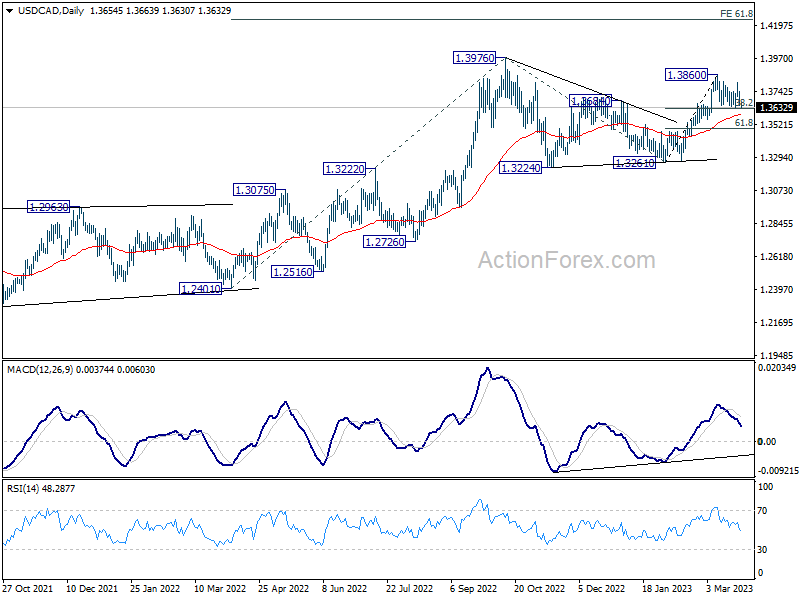

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3625; (P) 1.3685; (R1) 1.3720; More….

Intraday bias in USD/CAD stays neutral at this point. Further rally is expected as long as 1.3629 support holds. Firm break of 1.3860 will target 1.3976 high. However, break of 1.3629 will mix up the near term outlook. Intraday bias will be back on the downside for 55 day EMA (now at 1.3586), or even further to 61.8% retracement of 1.3261 to 1.3860 at 1.3490.

In the bigger picture, the up trend from 1.2005 (2021 low) is still in progress. Break of 1.3976 will confirm resumption and target 61.8% projection of 1.2401 to 1.3976 from 1.3261 at 1.4234. Firm break there will pave the way to long term resistance zone at 1.4667/89 (2016, 2020 highs). On the downside, break of 1.3261 support is needed to confirm medium term topping. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Feb | 0.20% | 0.40% | 1.90% | 1.80% |

| 11:00 | GBP | BoE Quarterly Bulletin | ||||

| 12:30 | USD | Goods Trade Balance (USD) Feb P | -89.9B | -91.5B | ||

| 12:30 | USD | Wholesale Inventories Feb P | 0.20% | -0.40% | ||

| 13:00 | USD | Housing Price Index M/M Jan | -0.20% | -0.10% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jan | 4.50% | 4.60% | ||

| 14:00 | USD | Consumer Confidence Mar | 101.7 | 102.9 |