{kind=link}

Summary

- European banks are in focus today with banking sector stocks under some pressure. In this report, we provide brief and aggregated metrics related to the stability of the Eurozone banking sector.

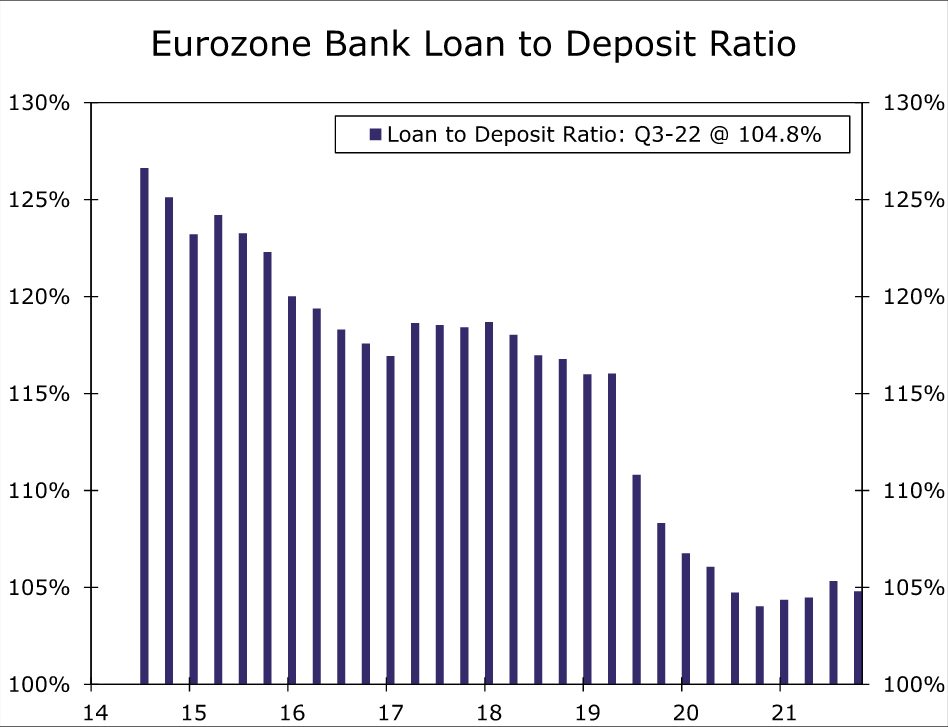

- The liquidity position of the Eurozone banking sector appears to have improved in recent years, as evidenced by a drop in the loan-to-deposits ratio (LDR). For countries participating in the Single Supervisory Mechanism (SSM), in Q2-2015 the LDR ratio stood at 126.6%, but by Q3-2022 that ratio had fallen to 104.8%, suggesting more of a balance between banks’ deposits base and loans extended to customers.

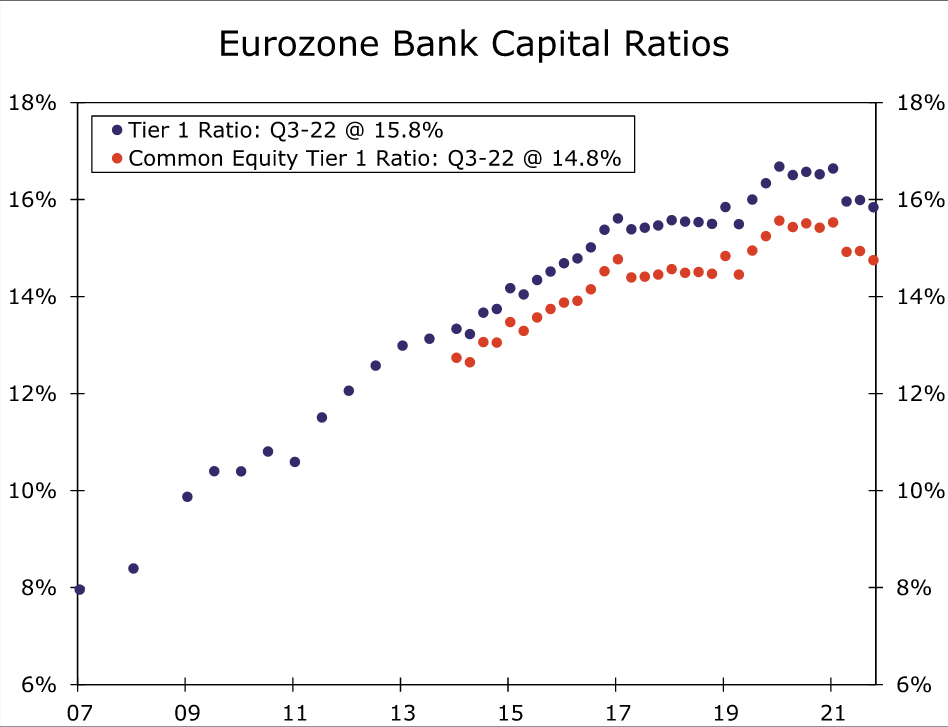

- Eurozone banks in aggregate appear to be adequately capitalized. The broader Tier 1 ratio stood at 15.84% in Q3-2022, down from a peak of 16.67% in Q4-2020. However, capital ratios are well above the levels that prevailed at the time of the global financial crisis.

- From a policy perspective, if European banking sector difficulties were to worsen and have meaningful economic effects, it could curtail the extent of European Central Bank monetary tightening. However, at this stage we would view aggressive and emergency monetary easing from the European Central Bank to stabilize the banking sector as a low probability scenario.

Eurozone Banking Sector Solid, But Softening

After concerns surrounding the U.S. banking sector in recent days, European banks are in focus today with banking sector stocks under pressure. In this report we provide brief and aggregated metrics related to the stability of the Eurozone banking sector.

Overall, the liquidity position of the Eurozone banking sector appears to have improved in recent years, as evidenced by a drop in the loan-to-deposits ratio (LDR). For countries participating in the Single Supervisory Mechanism (SSM), in Q2-2015 the LDR ratio stood at 126.6%, but by Q3-2022 that ratio had fallen to 104.8%, suggesting more of a balance between banks’ deposits base and loans extended to customers.

Meanwhile, Eurozone banks in aggregate appear to be adequately capitalized. The Common Equity Tier 1 ratio stood at 14.75% in Q3-2022, down slightly from a peak of 15.56% in Q4-2020. The broader Tier 1 ratio stood at 15.84% in Q3-2022, down from a peak of 16.67% in Q4-2020. While those capital ratios have softened moderately in recent quarters, they remain well above levels prevailing at the time of the global financial crisis. For comparison, the Tier 1 capital ratio stood at 7.96% in Q4-2007.

Considering the liquidity and capital position of the Eurozone banking sector, these dynamics should mitigate the chances of any broad based systemic issues across the Eurozone banking sector. That is not to say, however, that bank lending standards could tighten, and credit growth could slow—developments that could affect the outlook for Eurozone growth and inflation over the medium term. From a policy perspective, if European banking sector difficulties were to worsen and have meaningful economic effects, it could curtail the extent of European Central Bank monetary tightening. However, in our view at this stage we believe aggressive and emergency monetary easing from the European Central Bank to stabilize the banking sector is not that likely.