{kind=link}

On Friday, March 10, the 16th largest US bank suddenly burst. The bankruptcy became the second largest in history among American commercial banks. In this article, we look at what happened and how it could affect all of us.

History of the bank

Forty years ago (in 1983), a bank appeared in California. It decided to serve mainly big-headed guys who created new promising businesses and raised much money from venture investors.

The business occurred in Silicon Valley, and the bank was called Silicon Valley Bank (SVB). This business model was highly successful as, for the next few decades, startups rowed money literally with a shovel and put this money in the bank.

In 2020-2021, the technology industry in the United States experienced another boom: under the slogan of combating covid, the Federal Reserve threw unprecedentedly huge amounts of money into the financial system. A significant part of it went precisely to fast-growing tech companies. The Nasdaq-100 index has almost doubled in these two years, and startups raced to conduct initial public offerings (IPOs) and raise money directly from venture capital investors on an industrial scale.

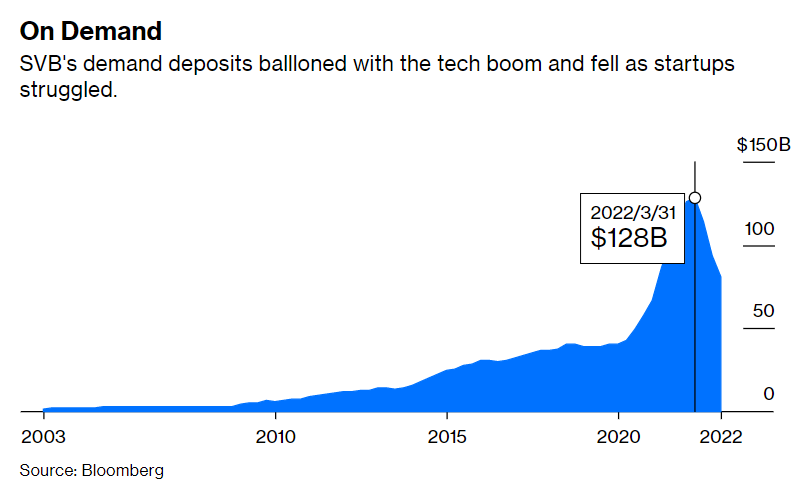

As a result, the business of SVB, which serves all these tech startups, also grew. Its client deposits more than tripled over that period (as did the bank’s stock price) to reach roughly $200 billion by early 2022, making Silicon Valley Bank the 16th largest bank in the US (and second in California).

Any bank, of course, is happy when they bring a lot of money to it. But with big money comes a big responsibility: you have to decide where to invest them so that they earn a nice profit in the pocket of the owners of this bank.

What to do with the money?

The classic business model of any bank is to collect more deposits at a lower rate and distribute this money to reliable companies in the form of loans at a higher rate. In the case of Silicon Valley Bank, this was problematic. Most startups from Silicon Valley do not look much like “safe businesses” with stable cash flows. Moreover, these startups had enough money. In 2020–2021, investors lined up to fill such companies with cash.

Therefore, SVB decided that the money would be logical to invest in the stock market. Of course, they did not go to buy Tesla shares with leverage – that would be too much. However, they decided to buy reliable bonds from the US government (US Treasuries) or mortgage-backed debt securities with suitable collateral in the form of real estate.

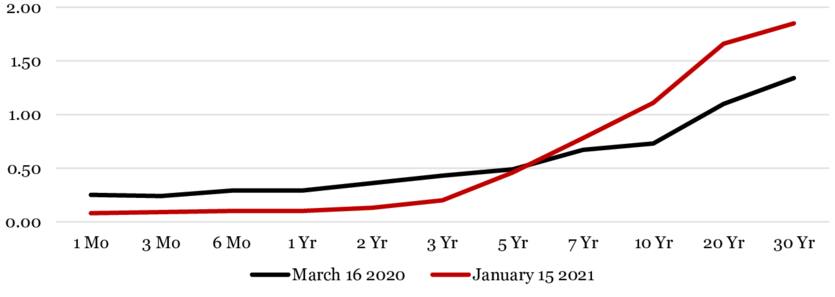

And now, let’s remember what yields gave reliable dollar bonds during that period:

Yield on US government bonds as a percentage (vertical scale) depending on their maturity (horizontal scale) in 2020-2021

The US Federal Reserve then drowned the interest rate to almost zero (to save the economy from covid horrors), so placing money in reliable US Treasuries on the horizon of a year or two could bring about zero profit.

So, the bankers from Silicon Valley Bank thought that you wouldn’t earn much by investing at 0%. The solution was simple – the bankers invested most of the capital into longer bonds with a 5-10 years maturity, which at that time had a yield slightly above 1.5% per annum.

How rising rates killed bonds

Any financier knows that when you buy long bonds, you take on the risk of rising interest rates.

Why is this happening? Suppose a company issues a $100 value bond with a 1% coupon (the market level at the time), maturing in 50 years, and you buy it. A year later, the level of rates increased, and now these companies are lent at 2% per annum.

Can you sell your bond to someone for $100? Of course not. But for $50, such a bond will be bought from you without any problem. After all, a coupon of $1 per year will yield 2% on the “current market value” of the paper at $50.

This happened in 2022 when the US Federal Reserve raised the interest rate from about zero to almost 5%.

As a result, the bond portfolio of Silicon Valley Bank showed a drawdown from 9 to 17%, which already, as it were, exceeded the size of the bank’s capital (the difference between existing assets and liabilities).

Investors caused the bankruptcy

It is interesting that, in itself, this loss has yet to be fatal for the bank. Accounting standards allow losses to be recognized after a while. And there is even logic in this: because of the rate increase, the bonds sink not forever but temporarily. If you hold them until maturity, they will recover over time, and everything will be ok.

But this logic only works if the bank has “the ability to wait.” And here is the time to remember that most of the deposits in Silicon Valley Bank can be withdrawn by the customers at any time.

The systematic outflow of such deposits from the bank began in mid-2022. The tech industry began to decline, and attracting new investors’ money was no longer easy.

But for SVB, this felt like a gradual activation of a time bomb. The faster the outflow of deposits became, the clearer that simply “sitting out to maturity” in these bonds would not work. Sooner or later, they would have to be sold at a loss to receive funds to return money to customers.

This is what happened. In 2023 the bank had to start selling these long bonds at a loss, and then it suddenly became very clear to everyone that there would not be enough money for everyone. Venture start-ups from Silicon Valley began to call each other and advise urgently to remove all the money from Silicon Valley Bank.

The concentration of SVB in one sector played a cruel joke on the bank: if they had many small retail clients, they might have passed. But since IT startups in the Valley communicate very closely, there was a full run on the bank when everyone tried to get their money out early (because the last one in this line may not get anything).

As a logical result – on March 10, banking regulators in the United States began, de facto, the bankruptcy procedure for SVB.

What is next?

The collapse of the SVB has undermined investor confidence in the US banking sector. Clients began withdrawing money from other banks, fearing a repetition of the situation, and already on Monday, some banks lost from 20% to 80% of their share price.

Such behavior of investors can provoke more than one bankruptcy — the following contenders: the American First Republic Bank, Pacific Westerns, and Western Alliance.

During the weekends, the US officials clarified that the situation is manageable and promised “cheap” loans for the banking sector. As a result, the US dollar declined as cheap loans involved running a “printing press”. Moreover, markets are now pricing the Federal Reserve to leave the rate at the same level on March 22, which could send the US dollar even deeper.

Many investors turned to Bitcoin, which rose 14% on Monday as US stock indices fell. This trend could continue if the banking story continues and the Fed keeps stimulating the economy with bailout money.

Conclusion

Times of crisis are always times of opportunity. The impossibility of determining the fair valuation of the company can be compensated by the possibility of speculative operations on the market.

Fortunately, trading FBS allows you to profit on rising and falling markets. FBS gives traders a significant advantage due to a wide range of instruments, low commissions, and analytical support.