{kind=link}

U.S. Highlights

- Pending home sales rose 8.1% in January, however with mortgage rates now back up around 7% this is unlikely to be sustained moving forward.

- The ISM Manufacturing Index improved for the first time in six months but continued to indicate contraction in the sector.

- Fed speakers this week noted the upside risk to the policy rate path posed by recent economic data, pushing the 10-year Treasury yield above 4%.

Canadian Highlights

- GDP was flat in the fourth quarter of 2022, yet the details paint a slightly better picture. Most notably, consumer spending increased 2% annualized, goosed by autos.

- Statcan’s preliminary estimate suggests a 0.3% gain in monthly, industry-based GDP in January. However, some caution is warranted in interpreting this figure, as industry-based GDP growth has been outstripping the expenditure-based measure (which is what the Bank of Canada forecsats).

- The Bank of Canada meets next week, and a pause is all but assured. We think policymakers are done hiking rates, although are ready to adjust should growth and/or inflation surprise.

U.S. – Higher Rates Abound

Congratulations on successfully making it to the third month of 2023. We are now just two and a half weeks away from economists’ most anticipated day of 2023. No, not the first day of Spring, the next FOMC rate announcement on March 22nd. This week we got a peek into six different FOMC members thinking on the expected path of policy and got pulse checks on the housing, manufacturing, and service sectors. In financial markets, Treasury yields continued their upward march, with the ten-year Treasury yield rising above 4% while the S&P 500 has clawed back earlier losses and is up 1% on the week as of the time of writing.

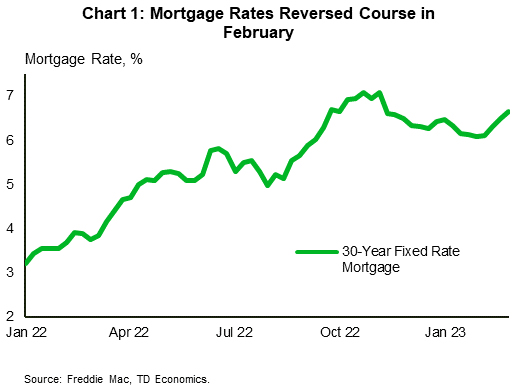

Pending home sales in January increased for the second consecutive month, rising by 8.1% month-on-month (m/m). Falling mortgage rates in late 2022 helped slow the year-long decline in sales activity, despite prices continuing to sink through the end of the year. Seasonally adjusted national home prices, as measured by the S&P CoreLogic Case-Shiller index, continued to decline in December (-0.3% m/m), matching the decline seen in November. With the 30-year mortgage rate rising to 7% in February this reprieve is likely to prove temporary (Chart 1).

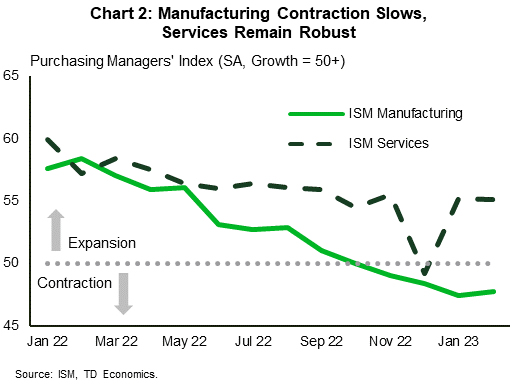

On Wednesday, the ISM Manufacturing Index improved for the first time since August, though the sector remained in contractionary territory for the fourth consecutive month (Chart 2). New orders and backlogged orders continued to contract, albeit at a slower pace. In contrast, the ISM Services Index reading on Friday showed that the industry is still expanding, with new orders growing at a faster pace.

Supplier delivery times continued to see improvement in both sectors with ocean freight costs declining for a sixth consecutive month. However, the manufacturing prices paid subindex increased for the first time since September, reflecting higher raw material prices. Although the subindex remained below the historical level associated with an uptick in the Producer’s Price Index, Treasury yields rose in response to the possible implications this could have on inflation and the Federal Reserve’s policy path.

Speaking of the Fed, we heard from seven different Federal Reserve officials this week, six of whom are current voting FOMC members. Their talking points covered a range of topics, from Governor Jefferson pushing back against calls for the Fed to raise its inflation target to Chicago Fed President Goolsbee saying it would be a mistake for the Fed to rely too heavily on financial market reactions. We also received policy specific comments, with Minneapolis Fed President Kashkari noting that he is open to a 50 basis point hike at the next meeting and Atlanta Fed President Bostic (a 2024 FOMC member) saying in an essay that he sees the policy rate going to 5.00 – 5.25% and staying there well into 2024.

Members made it clear that they are not yet convinced of the downward trajectory in inflation and upside risks to the policy rate path remain. All eyes will be on next week’s February employment data, which will show whether January’s blowout job growth was just a blip or something more concerning altogether for the Fed.

Canada – The Devil is in the Details

The release of this week’s fourth quarter GDP report likely brought some level of comfort to a Canadian central bank that is trying to cool economic growth and inflation. A flat performance (the economy recorded 0% growth in 2022Q4) is about as slow as it gets without the economy dipping into outright contraction.

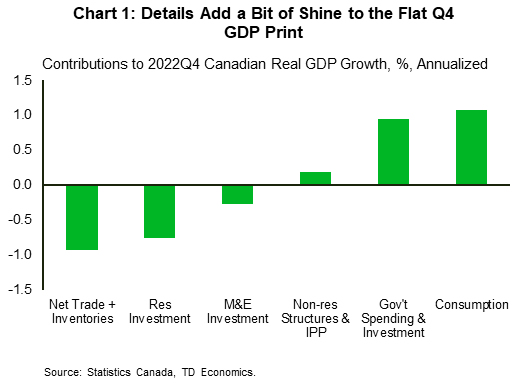

The details could best be characterized as “lukewarm”. However, they did paint a slightly better picture of the economy’s performance heading into 2023 than the headline figure would suggest (Chart 1). The headline was held back by a normalization in inventories, which subtracted 5.6 percentage points from growth. Inventories often experience large swings, and the drag in the fourth quarter came after the largest two quarter inventory build in decades through the middle of 2022. Final domestic demand was up 1% (quarter-on-quarter annualized (q/q)) – again, lukewarm, but not a disaster. Underlying this was a decent 2% q/q showing in consumer spending, supported by a pop in auto sales as improving supply chains fed pent-up demand. Moving forward, this could be one area of consumption that shows some strength as auto supply chains continue to normalize. Elsewhere, there were encouraging signs (from the Bank of Canada’s perspective) that higher rates weighed on interest-sensitive spending last quarter. For example, residential investment dropped 9%.

The fourth quarter stall in activity was a much softer performance than what the Bank expected in their January Monetary Policy Report (1.3%). It also undershot consensus, which was looking for a similar print. Part of the consensus call was probably conditioned on monthly, industry-based GDP data that was flagging a much stronger gain. GDP by industry increased 1% in the fourth quarter. This isn’t the first time the two series have diverged, and industry-based GDP outpaced its expenditure-based counterpart every quarter last year. We should keep this in mind when assessing Statcan’s preliminary estimate that industry-based GDP expanded 0.3% m/m in January. Assuming no growth in February and March, industry-based GDP is on track to record a 1% gain in the first quarter of this year. However, expenditure-based GDP (which is what the Bank of Canada forecasts) could be weaker if the recent divergence between the two GDP measures persists.

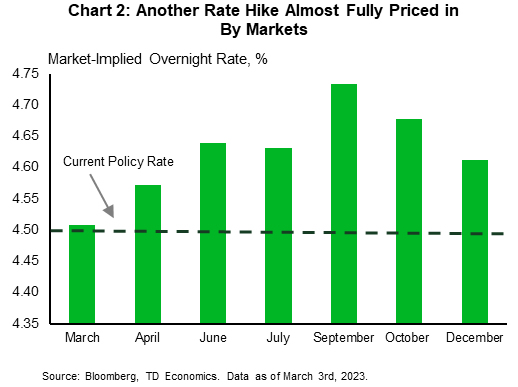

The Bank of Canada announces its interest rate decision next Wednesday, and given its recent communication of a (conditional) pause in January, there’s almost no chance it deviates from that stance. However, markets don’t agree that policymakers are quite done yet, with another hike fully priced-in by later this year (Chart 2). We view this week’s flat GDP print as supporting our case that the Bank of Canada is done hiking rates. This view is conditioned on a continued cooling in inflation and softening in the job markets.