{kind=link}

The forex markets are generally quiet today, with most major pairs and crosses staying inside yesterday’s range for now. Dollar is staying in a pole position for the week, maintaining most of the gains. The greenback will look into today’s PCE inflation data for next move. Euro and Swiss Franc are both on the weaker side, together with Aussie. Sterling is also firm but lacks momentum to extend the post-PMI rally. Yen is mixed for now after incoming BoJ Governor Kazuo Ueda confirms his dovish stance.

Technically, CHF/JPY’s rebound from 137.40 lost momentum after failing to break through near term falling channel. Immediate focus is now back on 143.21 support. Firm break there will argue that such rebound has completed, and the whole corrective fall from 151.43 is extending with another leg. Deeper decline would be seen back towards 137.40. In such case, Swiss Franc’s weakness could also be seen in extended rebound in EUR/CHF and GBP/CHF.

In Asia, Nikkei rose 1.29%. Hong Kong HSI is down -1.22%. China Shanghai SSE is down -0.54%. Singapore Strait Times is up 0.63%. Japan 10-year JGB yield is down -0.0069 at 0.496. Overnight, DOW rose 0.33%. S&P 500 rose 0.53%. NASDAQ rose 0.72%. 10-year yield dropped -0.044 to 3.879.

BoJ Ueda: Current policy a necessary, appropriate means to achieve 2% inflation

At a parliamentary confirmation hearing, incoming BoJ Governor Kazuo Ueda said, “current policy is a necessary, appropriate means to achieve 2% inflation,” despite various side effects emerging from the stimulus.

“Japan’s trend inflation is likely to rise gradually. But it will take some time for inflation to sustainably and stably achieve the BOJ’s 2% target,” he said.

“Consumer inflation is likely to fall below 2% in the latter half of the next fiscal year. It takes time for the effect of monetary policy to appear on the economy. ”

“It’s standard practice to act preemptively to demand-driven inflation, but not respond immediately to supply-driven inflation. Otherwise, the BOJ will be cooling demand, worsening economy and pushing down prices by tightening monetary policy.”

“If trend inflation heightens significantly and sustained achievement of the BOJ’s 2% target comes into sight, the central bank must consider normalizing policy. But if trend inflation lacks strength, the bank must continue how to maintain its ultra-easy policy, while paying attention to deterioration in market function.”

Japan CPI core hit 41-yr high at 4.2% in Jan

Japan all item CPI rose from 4.0% yoy to 4.3% yoy in January, below expectation of 4.5% yoy. CPI core (all-item ex-food) rose from 4.0% yoy to 4.2% yoy, matched expectations. CPI core-core (all-item ex-food and energy) rose from 3.0% yoy to 3.2% yoy, matched expectations.

Core CPI rate of 4.2% was the highest in 41-year since September 1981. The core inflation rate stayed above BoJ’s 2% target for nine consecutive months.

RBNZ Silk: A tightening pause is being contemplated now

RBNZ Assistant Governor Karen Silk said in a Bloomberg interview “there’s still more work to do here” on interest rate and fighting inflation. While “all levels are on the table” for April meeting, the central bank is not contemplating a pause.

“This is still an economy that has excess demand, a tight labor market, and as a consequence both headline inflation and core inflation at levels that are well outside the (target) band,” she said.

Regarding April meeting, “all levels are on the table for discussion at every meeting,” she said. “I’m not going to turn round and comment on whether we would be looking at 25, 50 or 75, they will all be on the table for discussion and they will depend on the information at hand.”

Nevertheless, a pause in tightening is “certainty not something that we’re contemplating at this point in time,” she said.

Silk also noted that some upside risk was built into the forecast interest peak of 5.5%. However, “without building that in, any variation to that peak would have been still at the margin,” she said. “There’s potentially still some upside risk on the fiscal side of it. Let’s just see how it plays out over the next six weeks.”

Looking ahead

Germany Gfk consumer confidence and Q4 GDP final are the only feature in European session. US will release personal income and spending with PCE inflation, and new home sales.

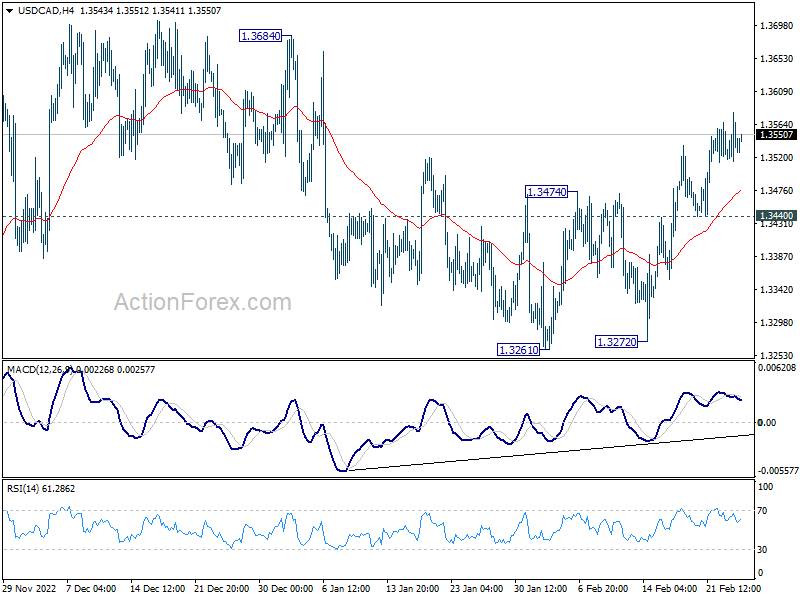

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3516; (P) 1.3548; (R1) 1.3581; More….

USD/CAD is losing some upside momentum, but further rally is expected as long as 1.3440 support holds. Next target is 1.3684 resistance. Sustained break there will pave the way back to retest 1.3976 high. On the downside, however, break of 1.3440 support will turn bias back to the downside for 1.3261 support again.

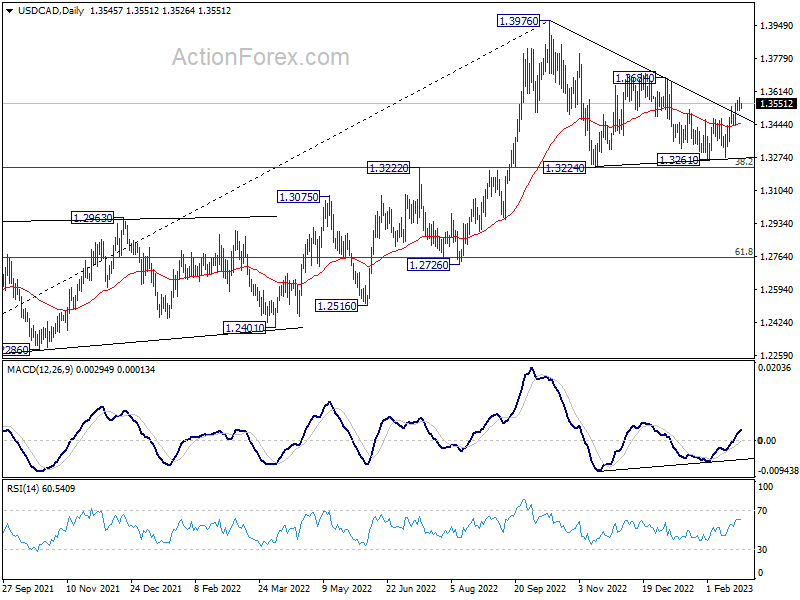

In the bigger picture, as long as 1.3222 cluster support (38.2% retracement of 1.2005 to 1.3976 at 1.3223) holds, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 high at a later stage. However, firm break of 1.3222/3 will indicate that the trend might have reversed. Deeper fall would be seen to next cluster support at 1.2726 (61.8% retracement at 1.2758).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Jan | 4.20% | 4.20% | 4.00% | |

| 00:01 | GBP | GfK Consumer Confidence Feb | -38 | -40 | -45 | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Mar | -30 | -33.9 | ||

| 07:00 | EUR | Germany GDP Q/Q Q4 F | -0.20% | -0.20% | ||

| 13:30 | USD | Personal Income M/M Jan | 1.00% | 0.20% | ||

| 13:30 | USD | Personal Spending Jan | 1.00% | -0.20% | ||

| 13:30 | USD | PCE Price Index M/M Jan | 0.50% | 0.10% | ||

| 13:30 | USD | PCE Price Index Y/Y Jan | 4.90% | 5.00% | ||

| 13:30 | USD | Core PCE Price Index M/M Jan | 0.40% | 0.30% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Jan | 4.10% | 4.40% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Feb F | 66.4 | 66.4 | ||

| 15:00 | USD | New Home Sales Jan | 620K | 616K |