{kind=link}

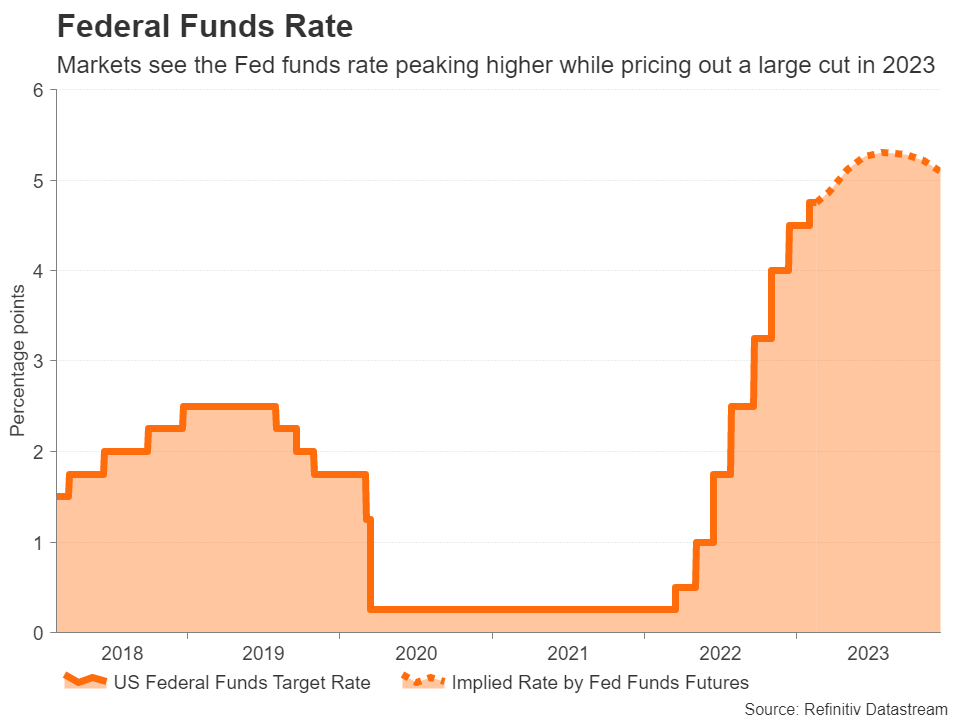

The US dollar has come off the back foot after a series of strong data and hawkish Fed talk, but is there scope for a more substantial recovery? The minutes of the Fed’s January 31-February 1 meeting out on Wednesday (19:00 GMT) will guide traders through to Friday when the all-important PCE inflation figures are due (13:30 GMT). Personal income and consumption readings for January will be vital too as the debate about whether the American economy can avoid a recession rages on.

What recession?

US economic indicators swung up in February, much to the relief of investors as not only does this ease concerns that the Fed’s aggressive rate hiking campaign is choking growth, but it also bodes well for the earnings outlook for corporate America as the worst case scenario is priced out of stocks. However, the strength of the latest batch of data has caught policymakers off guard too.

Some may be scratching their heads right now, wondering if the decision at the last meeting to shift to a slower gear was the right call. The half a million jump in January payrolls in particular must have come as quite a shock and caused angst. Add to that the smaller-than-expected drop in CPI inflation, and Fed officials are once again talking about the “significant road ahead” in their inflation battle.

Significant road ahead

Those were the words of Chair Jerome Powell, who spoke a few days after the jobs report. The minutes may therefore not reveal anything new as far as the Fed chief is concerned. But what will be interesting to see, even though the decision was unanimous, is whether there were any voting members who were hesitant about slowing down the pace of rate increases for the second straight meeting.

Two non-voting members – the Cleveland Fed’s Mester and St. Louis’ Bullard – have already expressed doubt about the need to downshift. Any hint in the discussions of that meeting that policymakers are more than ready to re-accelerate the pace of tightening should inflation prove stickier than anticipated, could put risk assets under renewed pressure.

Labour market is getting tighter

Yet, unless the tone of the minutes is vastly more hawkish than policymakers’ recent remarks, traders might be hesitant to react before they’ve had the chance to digest Friday’s slew of data. A day earlier, the second estimate of fourth quarter GDP will be released, though, no revision to the initial reading of 2.9% annualized growth is anticipated.

The weekly jobless claims on the other hand might be more crucial as they have been running below 200k for the last few weeks, pointing to ongoing tightness in the labour market. Another solid print in the jobless claims on Thursday could put investors on high alert ahead of Friday’s numbers.

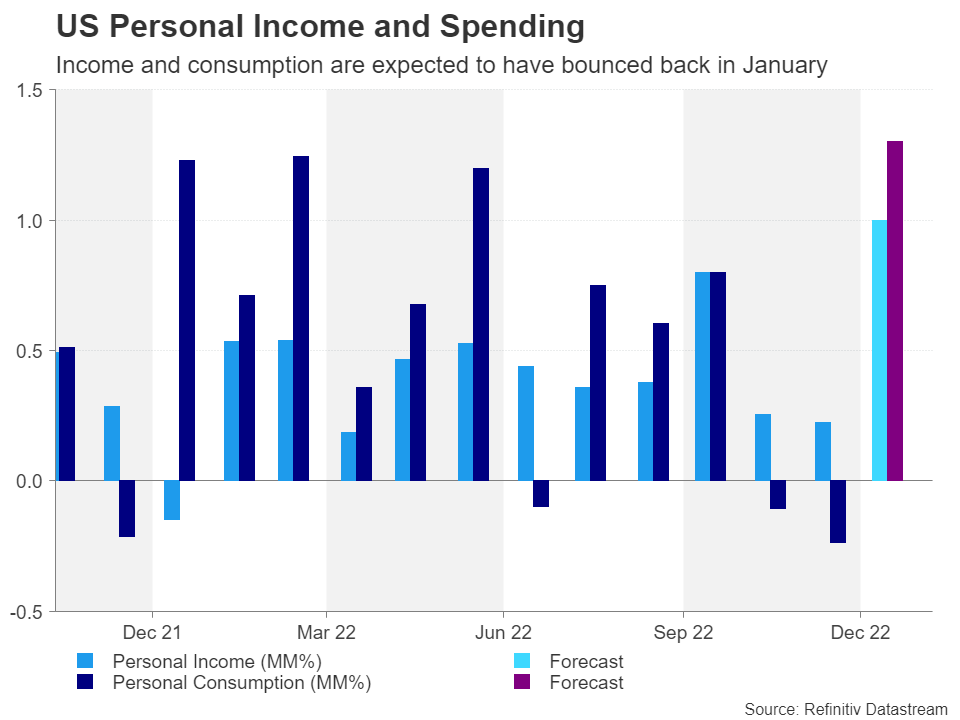

US consumers are spending again

Both personal income and personal spending are expected to have bounced back strongly in January, rising by 1.0% and 1.3% month-on-month, respectively. Consumer spending sagged towards the end of 2022, but as indicated by the retail sales figures, milder weather likely spurred a rebound in January.

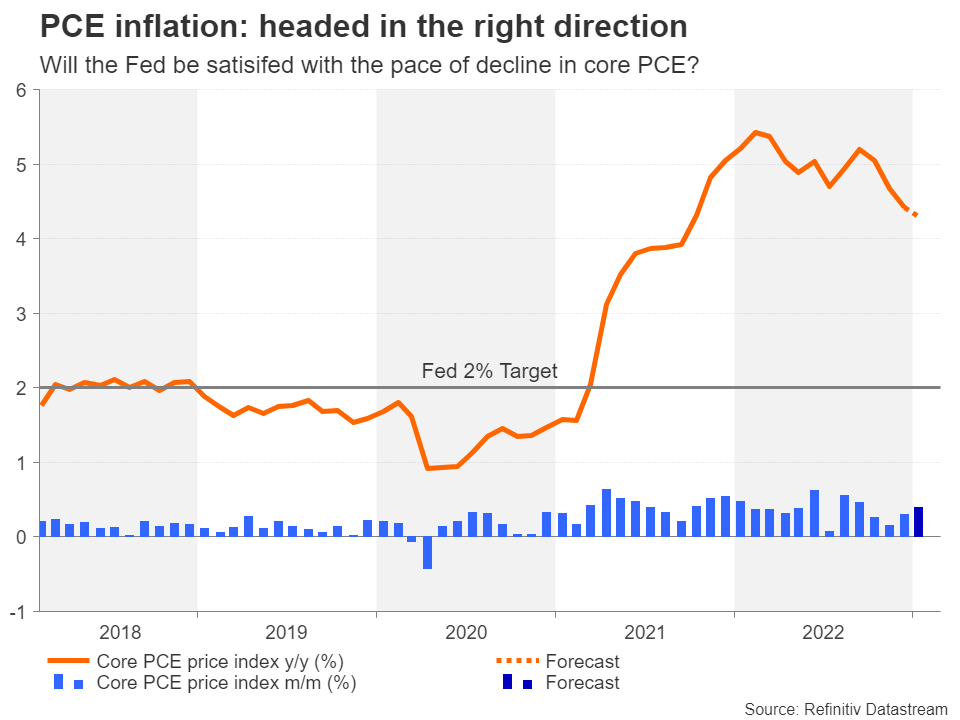

The highlight, however, on Friday will be the core PCE price index, which poses the biggest threat to risk appetite following the CPI surprise. The Fed’s favourite inflation gauge is forecast to have inched down 0.1 percentage point to 4.3% y/y in January, while the monthly measure is projected to have quickened slightly to 0.4%.

With investors already on edge, if the core PCE price index does not maintain a downward path then that would heighten fears of elevated inflation persisting for longer, and therefore, interest rates going higher and staying higher for longer.

Dollar’s revival not yet convincing

The question for the dollar, however, is would that be enough to rally the bulls? Although the Fed is unlikely to pause anytime soon, other central banks like the ECB are still hiking too, while the Bank of Japan may soon exit from all its stimulus policies. Still, if everything from the minutes to the data go in the dollar’s favour, there could be some healthy gains in store for the currency.

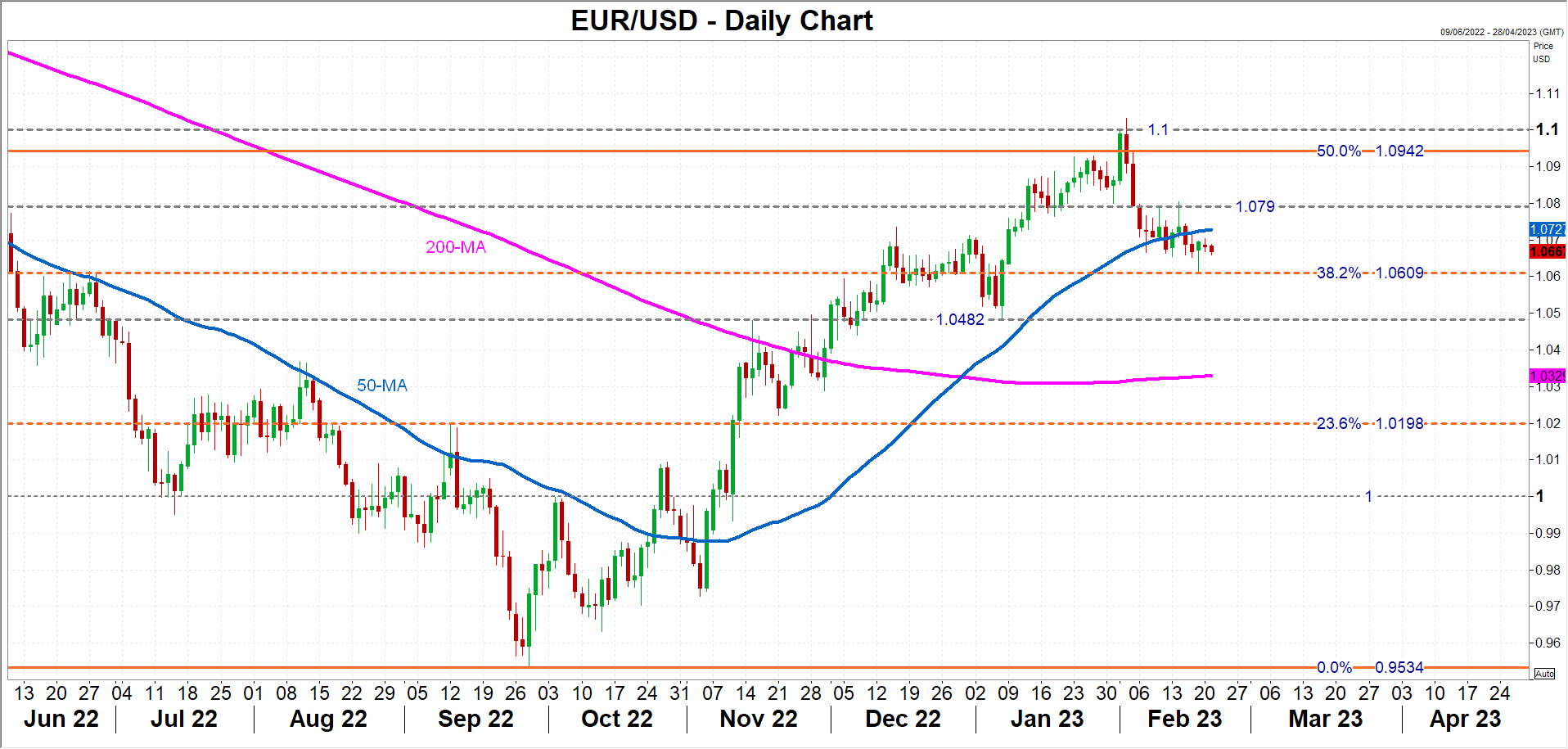

The euro, which has just slid below its 50-day moving average (MA), has found support in the $1.06 region where the 38.2% Fibonacci of the 2021-2022 downtrend runs across. Should this support crumble, the early January trough of $1.0482 would likely come into focus before attention turns to the 200-day MA near $1.0330.

In the event, though, that the minutes are no more hawkish than Fed official’s latest comments and there are no nasty surprises in the PCE inflation numbers, the euro might just be able to recapture the 50-day MA and have another attempt at the $1.10 handle where the uptrend stalled in January.

For the moment, the dollar’s recovery appears to be a short-term correction rather than a trend reversal so further positive momentum is required to push the greenback to at least the half-way point of the downward phase that began in late September to signify a sustainable rebound.