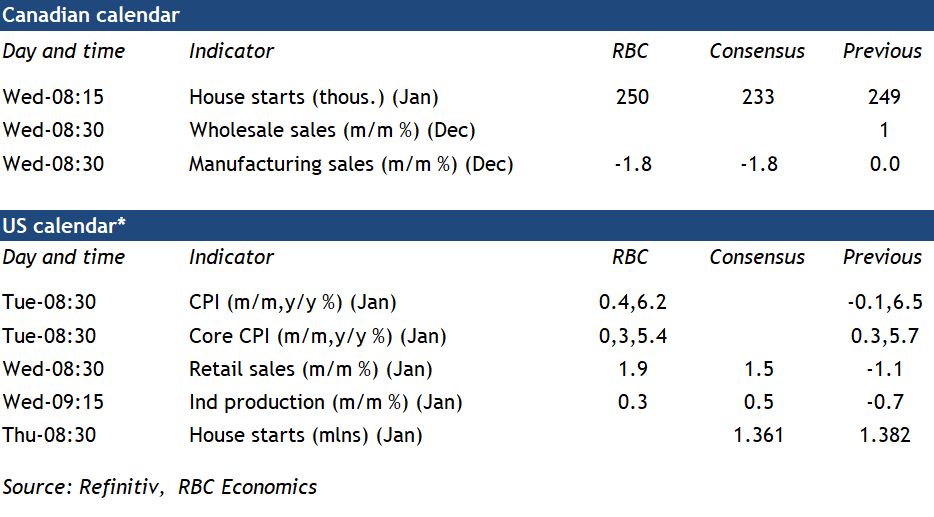

{kind=link}

U.S inflation will be the focus next week after a surge in January employment raised eyebrows. The surprise jump in the measure has raised concerns that the economy isn’t cooling quickly enough to ease price pressures. Still, we expect CPI growth edged down to 6.2% in January from 6.5% in December (year-over-year). Food price growth likely also continued to slow, albeit from very high levels. By contrast, we expect energy price growth ticked up for the first time in 7 months—though to an 8% rate that is still well below a June peak of 42%.

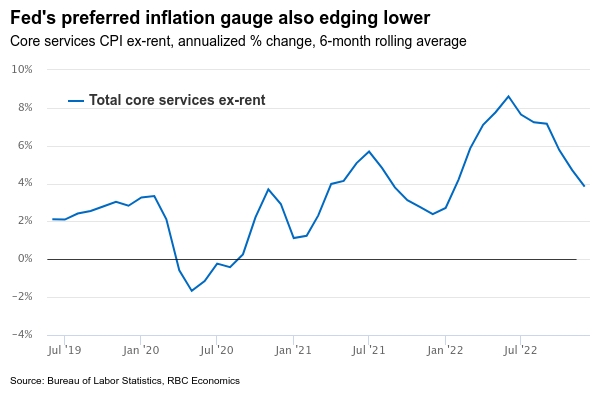

Both food and energy prices are heavily influenced by global cost pressures—which have been easing. But U.S. Federal Reserve officials will be more focused on ‘domestically-driven’ price growth. We look for core inflation to slow further in January, coming in at 5.4% year-over-year, down from 5.7% in December. And prices for purchased goods are also expected to have softened. Home rents will continue to fuel core inflation as earlier price increases ripple through to leases, but those pressures are likely to slow in the months ahead. Core services ex-rents, a measure Federal Reserve officials have highlighted as a key indicator of where U.S. inflation is heading, will be watched more closely. But all told, recent inflation reports have pointed to relatively broadly-based easing in price pressures.

The labour market remains strong, with last week’s employment report showing payrolls up by 517,000 and the unemployment rate down to 3.4%. Wage growth has been decelerating–a measure Federal Reserve policymakers are also closely monitoring for further signs of disinflation. For now, we continue to look for another 25 basis point hike to the Fed funds rate in March—though any robust (and sustained) labour market data could alter this outlook.

Week ahead data watch

January U.S. retail sales likely rose 1.9% from a 1.2% decline in December, thanks to an 18% surge in unit vehicle sales. U.S. industrial production likely edged up 0.3% during that month, with higher manufacturing outputs offsetting a weather-related decline in utility output.

StatCan’s flash estimate of Canadian manufacturing sales showed a 1.8% decline in December, and flagged a drop in petroleum and coal products. The decline in petroleum and coal sales was likely price-related but isn’t significant enough to explain in the overall decline total sales. This suggests weaker sales in other sectors as well.

Canadian housing starts are expected to stay at 250,000 units in January. Residential building permit issuances have been slowing, with a 3-month rolling average of 242,000 units in December.