{kind=link}

With market participants revising up their implied path for the Fed funds target rate after the astounding US employment report for January, the dollar is set to eke out gains for the second straight week. That said, the next test for the currency may come in the form of the January CPI data, due to be released on Tuesday at 13:30 GMT. How may the greenback react to another notable slowdown?

Dollar stages a comeback after NFPs and ISM PMI

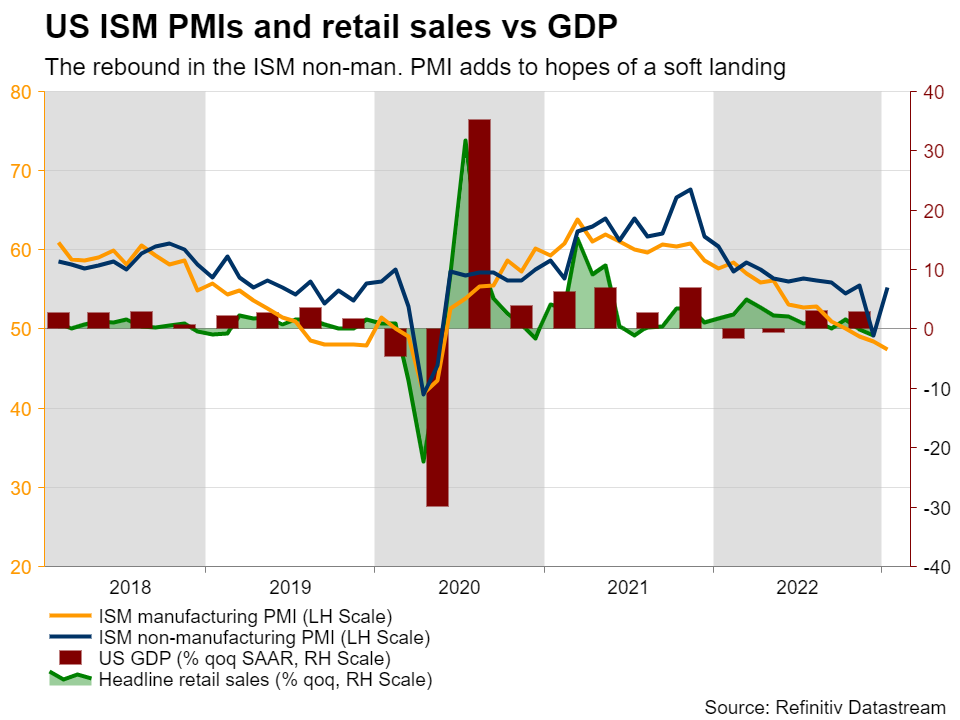

Last Friday, the US employment report showed that nonfarm payrolls surged by 517k in January, with the unemployment rate hitting a more than a 53 1/2-year low of 3.4%. Soon thereafter, the ISM non-manufacturing PMI rebounded strongly back into expansionary territory, adding to hopes that the US economy may eventually avert a recession.

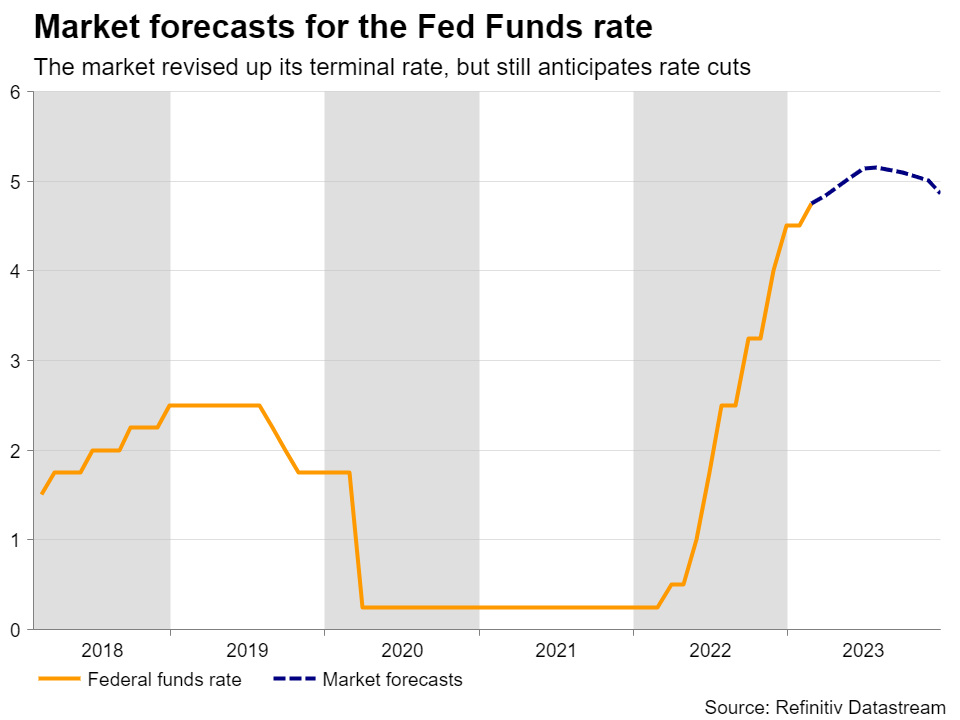

The result was a massive wave of dollar buying and a strong rebound in Treasury yields as investors revised up the level of where they expect interest rates to peak and priced out one of the two quarter-point rate reductions they were seeing towards the end of the year. Although Fed Chair Powell reiterated his disinflation remarks on Wednesday, market pricing was not altered much. Currently, investors are pricing in a terminal rate of 5.15%, in line with the Fed’s own projections, while they see interest rates being 30bps lower by the end of the year.

But CPIs could bring the dollar recovery to an end

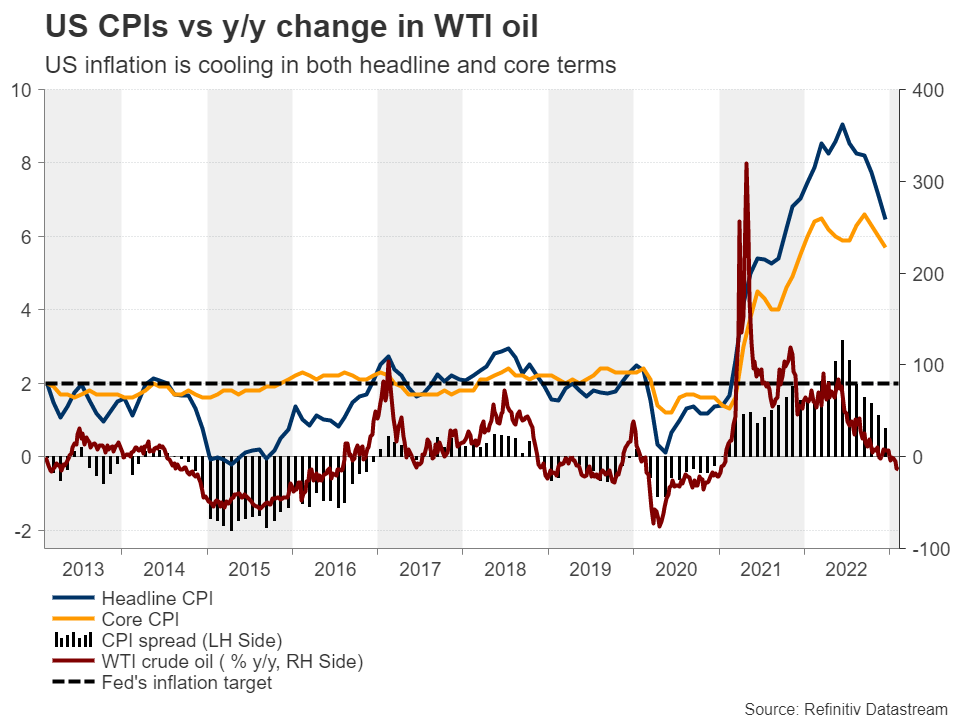

Having said all that though, investors bets and thereby the greenback will be put to the test on Tuesday, when we get the US CPIs for January. This data set has proven to be the dollar’s biggest nightmare in the past as consistent downside surprises in previous months were the fuel behind speculation for a Fed pivot and two quarter point cuts until December. Both the headline and core rate are expected to have continued to decline, to 6.2% y/y and 5.5% y/y from 6.5% and 5.7% respectively. Nonetheless, with the y/y chance of oil prices dipping further in the negative territory, the risks surrounding the headline rate may be tilted to the downside.

Another downside surprise could revive speculation about a lower peak in US interest rates as well as more rate cuts for later this year. US Treasury yields may come under renewed pressure and thereby the dollar could be sold again. With the ECB still expected to continue raising interest rates more aggressively than the Fed, especially following hawkish remarks by German policymakers Joachim Nagel and Isabel Schnabel, euro/dollar may rebound and continue its prevailing uptrend.

Door for a rebound in euro/dollar remains open

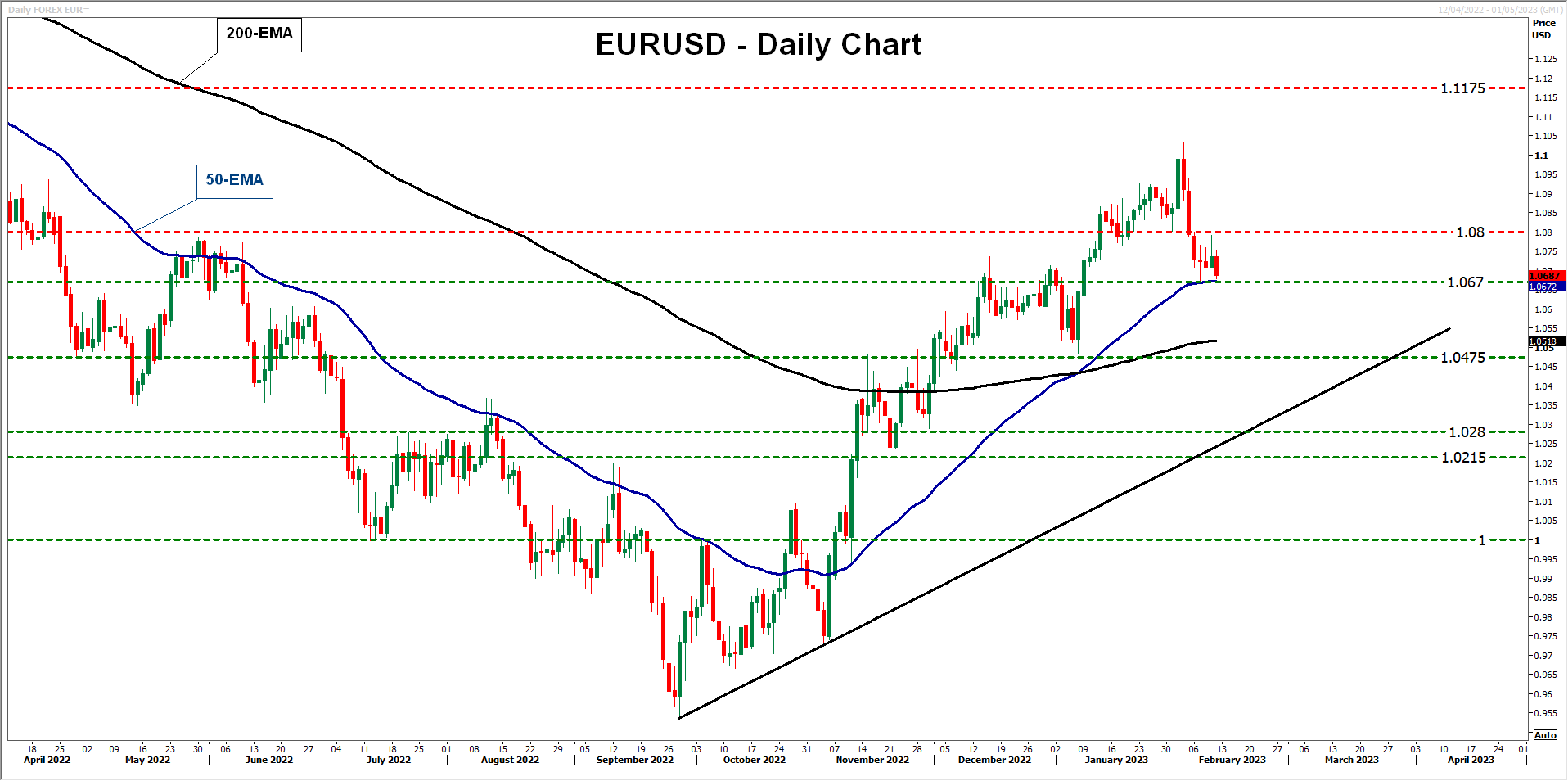

From a technical standpoint, euro/dollar is now testing the 1.0670 zone, which coincides with the 50-day exponential moving average. In the bigger picture, despite the steep slide following the NFPs, the pair is still trading well above the uptrend line drawn from the low of September 28, which keeps the door for a rebound in the foreseeable future open. Should the price rebound back above 1.0800, traders may be encouraged to put the key resistance of 1.1175 back on their radar.

On the downside, a dip below 1.0715 and the 50-day EMA could allow declines towards the 1.0475 zone. Such a dip could occur if the CPI data surprises to the upside. Having said all that though, even in the case of such a slide, the pair would still be trading above the aforementioned uptrend line. For the outlook to turn overly bearish, a clear dip below 1.0215 may be needed.