{kind=link}

The term of the 31st Governor of the Bank of Japan ends on April 8. For the past 10 years, Governor Kuroda has been spearheading the Japanese efforts to return the country to normal inflation rates and decent growth. The new BoJ Governor will face slightly improved conditions compared to 2013 when Kuroda took over, but the task remains equally daunting. Could the Japanese government hold a surprise in its nomination for the top spot or history will repeat itself and a Deputy Governor will take the job?

Kuroda’s tenure ending

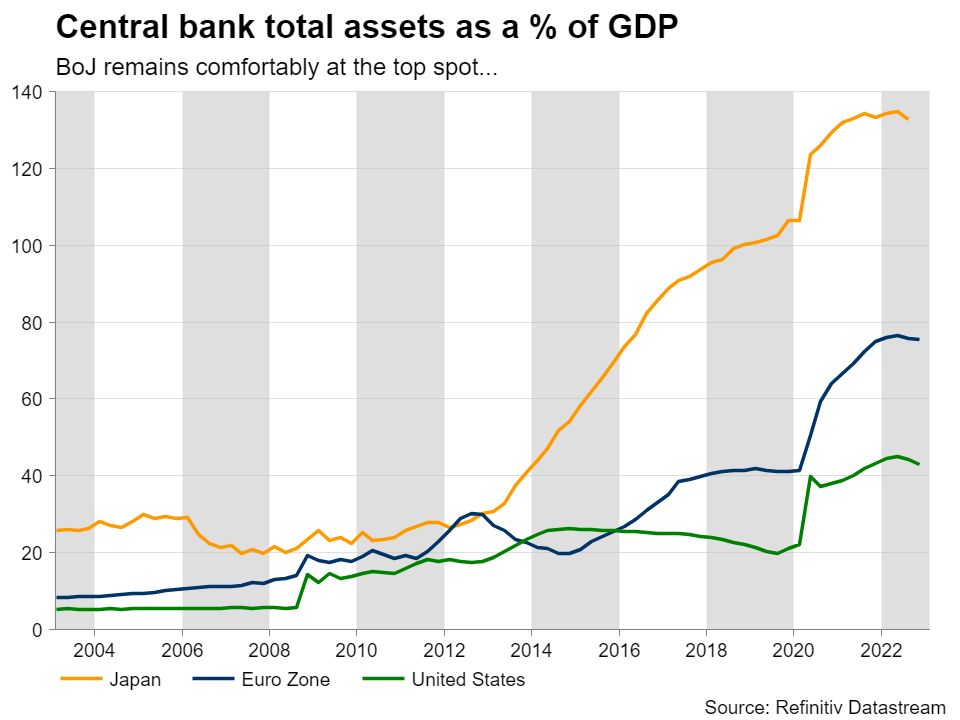

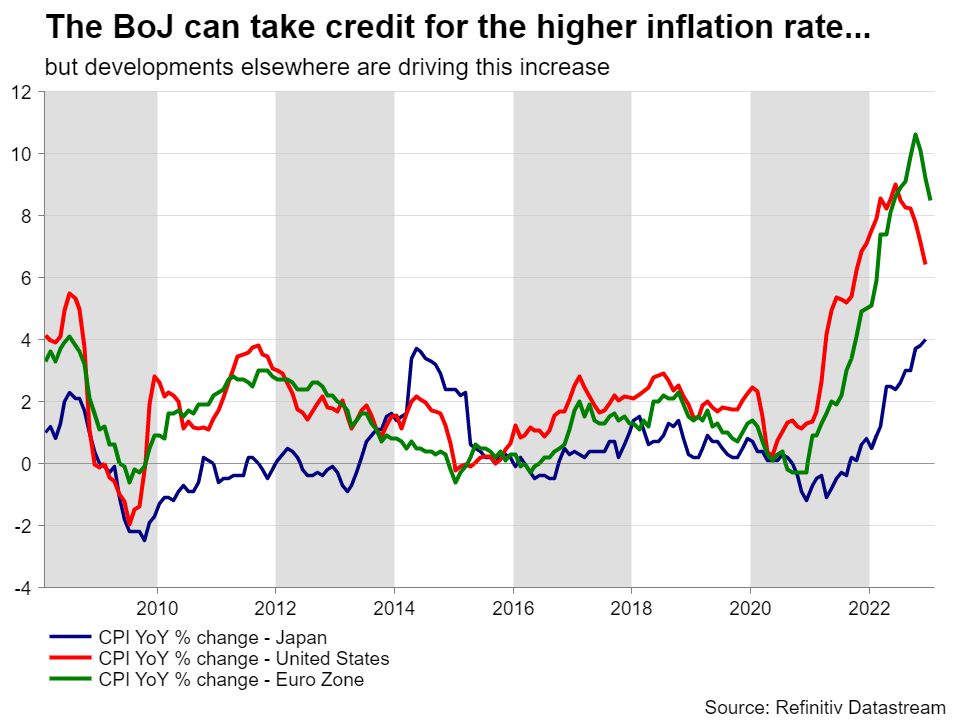

Governor Kuroda took over in March 2013 with the headline CPI year-on-year growth completing almost 4.5 years below the 0.5% rate. In coordination with the then Prime Minister Abe, Kuroda was given carte blanche to lead the Japanese economy into recovery. His immediate reaction was to massively expand the BoJ’s second Quantitative Easing programme that started in October 2010 and never looked back. The CPI performance in 2014 was optimistic, but the increase proved to be purely due to the sales tax increase. The renewed confidence in the BoJ’s efforts gradually dissipated as, despite the continued efforts by Kuroda et al, the results did not match the high expectations. Following the 2014 jump in the CPI, it took the Japanese economy seven years to produce inflation above 2% at a cost of a 488 trillion yen increase at the BoJ’s monetary base. Unfortunately for the Bank, the recent jump in the inflation rate seems to be a product of the recent COVID pandemic and the unfortunate events in Ukraine.

Current situation looks better than 2013

However, the situation on the ground looks more positive compared to 2013. Inflation has reached the highest year-on-year increase since January 1991, and the Japanese economy has been growing at a respectable rate under Kuroda’s leadership. But the main task of the new governor will be the withdrawal of the current massive support programme. Despite the global tightening cycle, the BoJ has only managed to announce a small change in its yield curve framework at the December meeting, resisting calls to more aggressive tightening steps. However, the market seems conservatively optimistic, and it is currently pricing in 14bps of rate hikes by year-end.

Main candidates for the Governor position

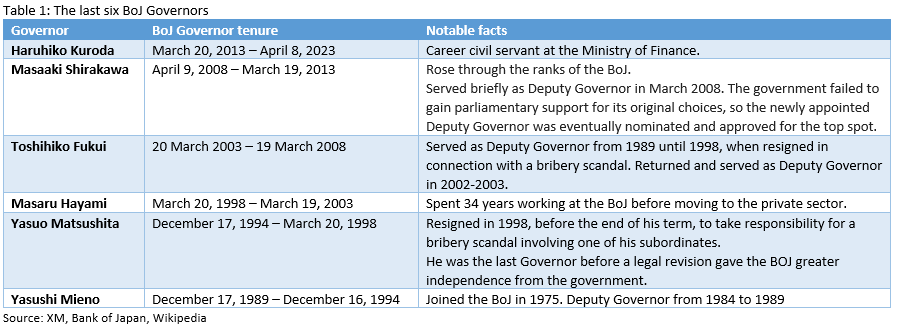

The government will most likely present the nominees for the top three BoJ positions next week. By examining the BoJ Governors since 1989, it is evident that there is a tendency for the government to choose the Governors from the BoJ ranks or the Japanese Finance Ministry. Even Hayami (1998-2003), then considered an outsider, spent 34 years working at the BoJ before moving to the private sector, only to return for BoJ’s top post. Interestingly, three of the last six governors had already served as Deputy Governors, and one held an executive director position before securing the Governor’s role.

Having said that, it makes sense for the government to firstly look at the Deputies’ ranks to find its new top man. Understandably, Masayoshi Amamiya is considered the most likely successor of Kuroda as he has spent his entire professional career at the BoJ, and for the past five years he has been working alongside Kuroda as a Deputy Governor. He is credited with drafting the 2013 expansion plan and supporting Kuroda’s strategy through the years.

From the pool of the remaining Deputy Governors, Hiroshi Nakaso appears to be a close contender. He was a Deputy Governor during Kuroda’s first term between 2013-2018, but he has recently taken another prestigious position. However, if the government decides to nominate him for the BoJ top spot, he is expected to honour the nomination. Nakaso is seen as more hawkish on monetary policy than Amamiya.

On the other hand, one cannot exclude a surprise from the government. The candidacy of the former Deputy Governor Nishimura has been making the rounds at the Japanese parliament. However, most remember in a negative way his tenure under BoJ Shirakawa, who was criticized for easing policy fast enough during this 2008-2013 period.

Yen would like a hawk taking over

To sum up, the government would prefer to avoid surprising the market and go for the safest option possible. However, it also makes sense for the PM Kishida to decide to distance himself from Abe’s choices and potentially announce a new face from the Ministry of Finance or a candidate that does not sit currently at the BoJ Policy Board. Kishida’s selection would potentially reflect his own view on the economic outlook for the Japanese economy, and hence a dovish selection could have ripple effects across the foreign exchange market, complicating the new governor’s work well before taking over. Yen recorded a 5% rally against the dollar when the amendment of the yield curve framework was announced in December. Part of this move is currently being unwound as the market appears to believe that Kishida might not be as bold as originally hoped in his selection. As a result, the massive support programme could potentially be wound down at a less aggressive pace than the yen bulls would have preferred.