{kind=link}

Dollar’s rally was choked off by terrible PMI data, in particular services, overnight. But the greenback is trying to regain some footing in Asian session. It’s too early to say that the bullish trend in Dollar has reversed. Traders are just holding their bets for now, awaiting more guidance from Fed Chair Jerome Powell at the Jackson Hole symposium. For now, Aussie and Kiwi are the stronger ones with Yen. Euro and Sterling are overwhelmingly weak. Dollar is mixed with Canadian.

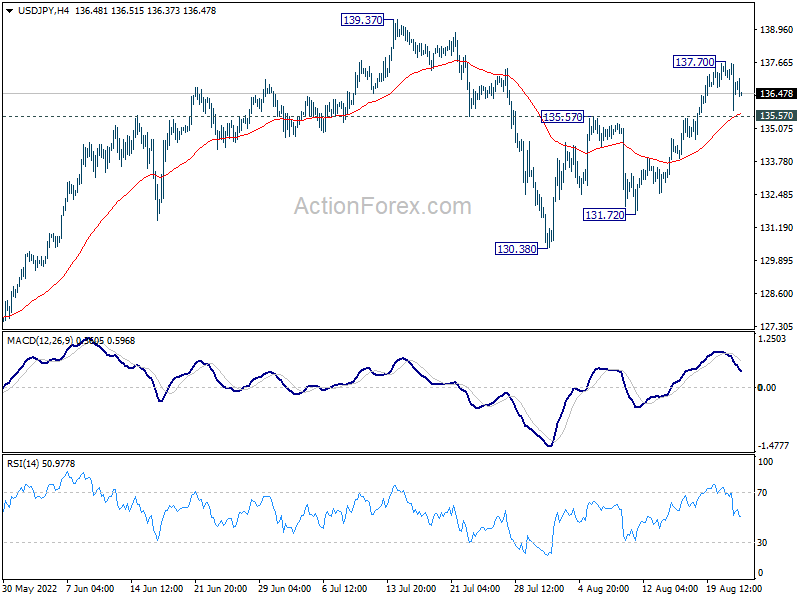

Technically, USD/JPY’s rebound from 130.38 is seen as the second leg of the corrective pattern from 139.37. It might have completed with three waves up to 137.70 already. Firm break of 135.57 resistance turned support will argue that the third leg has started back towards 130.38 support. If happens, it’s likely more of a boost to Yen then a drag on Dollar elsewhere.

In Asia, at the time of writing, Nikkei is down -0.45%. Hong Kong HSI is down -1.34%. China Shanghai SSE is down -1.29%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is down -0.0011 at 0.221. Overnight, DOW dropped -0.47%. S&P 500 dropped -0.22%. NASDAQ dropped -0.00%. 10-year yield rose 0.017 to 3.054.

Fed Kashkari: US economy in a completely unbalanced situation

Minneapolis Fed President Neel Kashkari said yesterday that the US economy is in a “completely unbalanced situation” of “maximum employment” and “very high inflation”. He said, “it’s very clear: We need to tighten monetary policy to bring things into balance.”

“When inflation is 8% or 9%, we run the risk of unanchoring inflation expectations and leading to very bad outcomes that would cause us to have to be very aggressive — Volcker-esque — to then re-anchor them,” he said.

“We needed to err on making sure we are getting inflation and only relax when we see compelling evidence that inflation is well on its way back down to 2%,” he added.

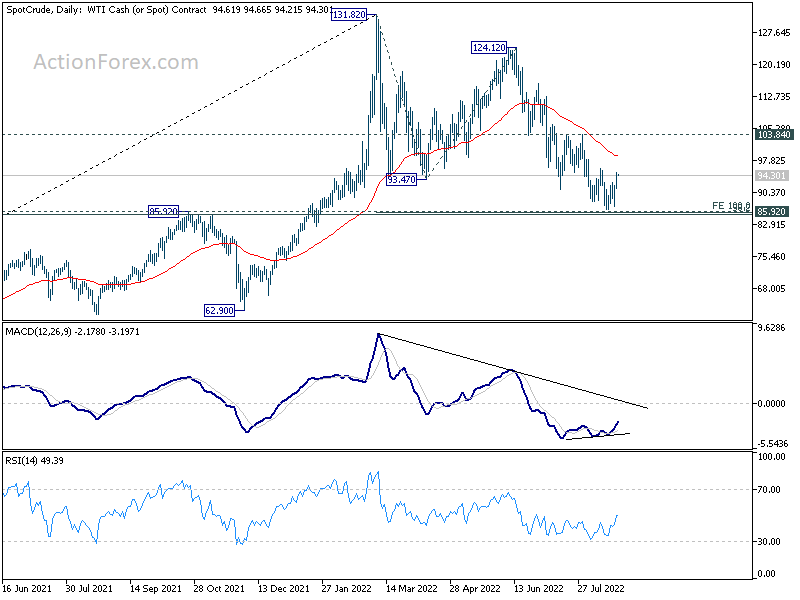

WTI oil ready for a bounce through 100

Oil prices rebounded this week on the prospect of production cut by OPEC+. Saudi Energy Minister Prince Abdulaziz bin Salman was quoted earlier that OPEC+ has the commitment, flexibility, and means to deal with challenges and provide guidance including cutting production at any time and in different forms. However, upside is so far capped as Reuters, based on information from nine OPEC sources, said productions cuts may not be imminent, and might coincide with Iran’s return to the market.

Technically, the conditions for a stronger bounce for WTI crude oil are there. Bullish convergence conditions are seen in both 4 hour and daily MACD. A near term falling channel resistance is already broken. More importantly, 86.41 is close enough to an important cluster support at 85.92, with 100% projection of 131.82 to 93.47 from 124.12 at 85.77.

Immediate focus is now on 95.91 resistance. Firm break there should confirm near term reversal for 103.84 resistance and possibly above. Also, in case of another fall, strong support is expected from 85.77/92 to contain downside.

Looking ahead

The economic calendar is empty in Europe. Main focuses are on US durable goods orders and pending home sales later in the day.

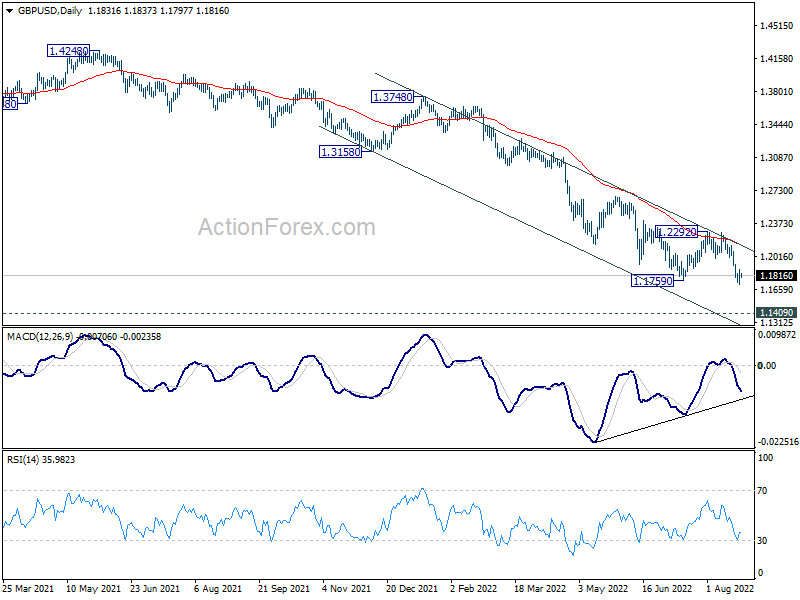

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1740; (P) 1.1809; (R1) 1.1900; More…

A temporary low is formed at 1.1716 with current recovery. Intraday bias in GBP/USD is turned neutral first. Upside of recovery should be limited by 1.2002 support turned resistance to bring another fall. Break of 1.1716 will resume larger down trend to 1.1409 long term support.

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2292 resistance holds. Next target is 1.1409 low. However, firm break of 1.2292 will bring stronger rise back to 55 week EMA (now at 1.2859).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | USD | Durable Goods Orders Jul | 0.60% | 2.00% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Jul | 0.20% | 0.40% | ||

| 14:00 | USD | Pending Home Sales M/M Jul | -2.50% | -8.60% | ||

| 14:30 | USD | Crude Oil Inventories | -7.1M |