{kind=link}

The currency markets are quiet overall as focus now turns to US job data. The post BoE selloff in Sterling didn’t last long. Meanwhile, Dollar is still range bound against Euro and Yen. The greenback’s rally attempt against Swiss Franc also faltered rather quickly. Commodity currencies are steady. Most major pairs and crosses are stuck inside last week’s range. Hopefully, today’s non-farm payroll will bring some life back to the markets.

Technically, the development in US stock markets, in reaction to NFP, could be the leading factor in other markets. S&P 500 has been making some progress in securing a near term bullish reversal. Immediate focus will be on 4177.51 resistance. Strong break there and a weekly close above should confirm that whole correction from 4818.52 has completed with three waves down to 3636.87. That would set the stage for more upside in SPX for the rest of Q3, and set the risk-on tone which would give Dollar and Yen some extended pressure.

In Asia, Nikkei closed up 0.85%. Hong Kong HSI is up 0.25%. China Shanghai SSE is up 0.59%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is down -0.0084 at 0.167. Overnight, DOW dropped -0.26%. S&P 500 dropped -0.08%. NASDAQ rose 0.41%. 10-year yield dropped -0.072 to 2.676.

Australia AiG services rose to 51.7, two-speed sector emerges

Australia AiG Performance of Services rose 2.9 pts to 51.7 in July. Sales jumped 7.4 to 49.3. However, employment dropped -2.9 to 52.4. New orders rose 1.7 to 50.6. Supplier deliveries rose 5.9 to 47.6. Input prices rose 5.3 to 74.3. Selling prices dropped -3.8 to 63.4.

Innes Willox, Chief Executive of Ai Group, said: “We are seeing a ‘two-speed’ services sector emerge as businesses contend with labour shortages and rising interest rates. Business & property and personal services grew dramatically in July, while retail & hospitality and logistics fell dramatically. Chronic labour shortages and a super-charged winter spike in absenteeism are large and growing challenges for labour-intensive service industries. And rising interest rates are dampening consumer sentiment, casting a shadow over consumer-facing sectors.”

Fed Mester: Interest rates continue to rise this year and into next through first half

Cleveland Fed President Loretta Mester said that “interest rates continue to rise this year and into next year through the first half and maybe by then we can pause and we can start bringing them back down.” She would “pencil in going a bit above four as appropriate”.

As for September meeting, she said, “it’s not unreasonable to think we might have to do a 75 (basis point move) but I can imagine it could be a 50. We’ll just have to look at the data as it comes in.”

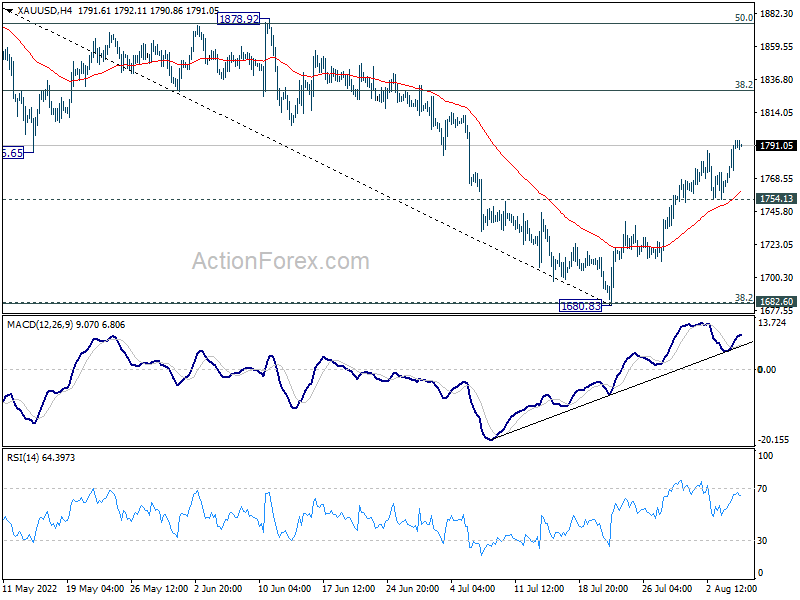

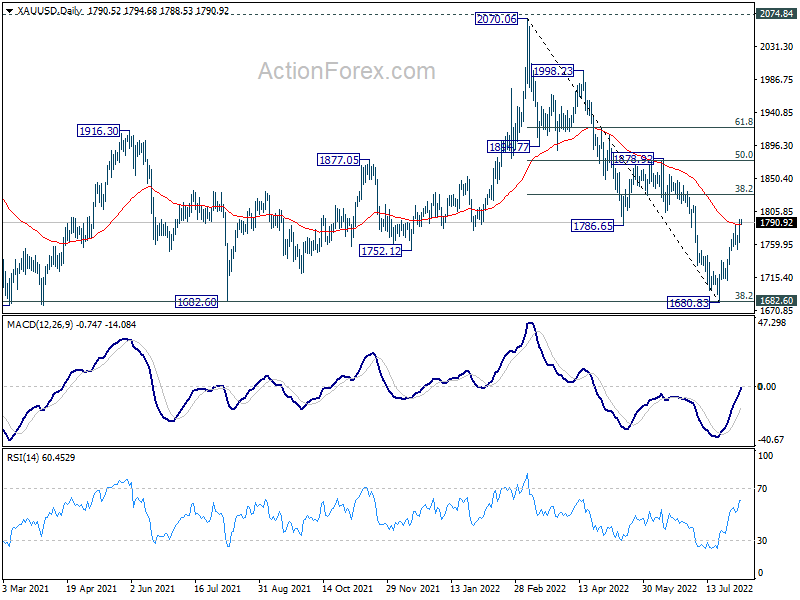

Gold resumes rally as focus turns to NFP

US non-farm payroll report is a major focus today. Employment is expected to grow 250k in July. Unemployment rate is forecast to be unchanged at 3.6%. Average hourly earnings would maintain a growth pace of 0.3% mom.

Looking at related data, ISM manufacturing employment ticked up from 47.3 to 49.9. ISM services employment rose from 47..4 to 49.1. Four-week moving average of initial claims rose from 233k to 255k. Overall, these data suggest that there won’t be a blockbuster NFP today. Wage growth would likely be the more market moving part.

Here are some readings on NFP:

- NFP Preview: Will We See the Lowest Jobs Reading Since 2020?

- US July NFP Expected to Slow

- Dollar Awaits Nonfarm Payrolls as Recession Worries Mount

Gold’s rally from 1680.83 resumed after brief retreat and breaks through 1786.65 resistance. The development adds to the case that whole decline from 2070.06 has completed after defending 1682.60 key support. Further rally is now in favor as long as 1754.13 minor support holds, for 38.2% retracement of 2070.06 to 1680.83 at 1829.51. The move could be accompanied by another round of near term selloff in Dollar.

Elsewhere

Japan labor cash earnings rose 2.2% yoy in June versus expectation of 1.9% yoy. Household spending rose 3.5% yoy versus expectation of 1.5% yoy. Germany industrial production rose 0.4% mom in June, versus expectation of -0.2% mom decline.

France trade balance and Italy industrial production will be released in European session. Later in the data, in addition to US NFP, Canada will also publish job data and Ivey PMI.

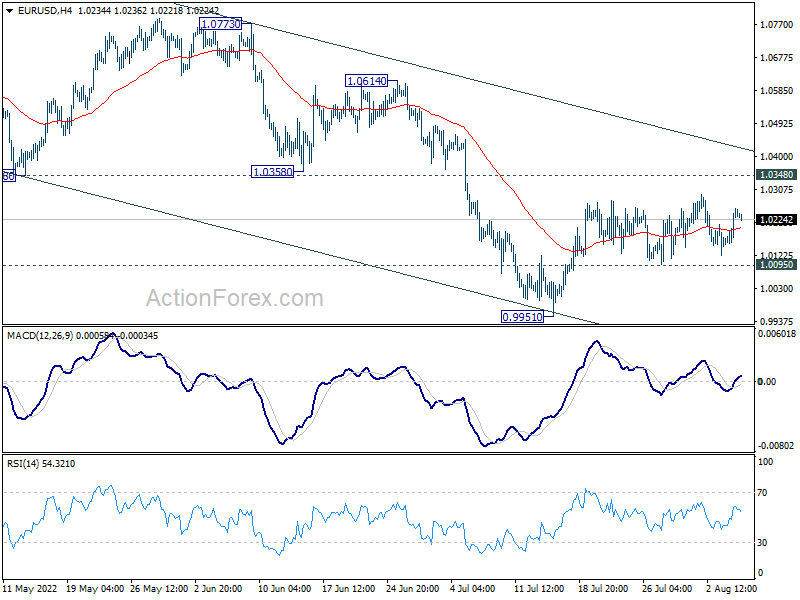

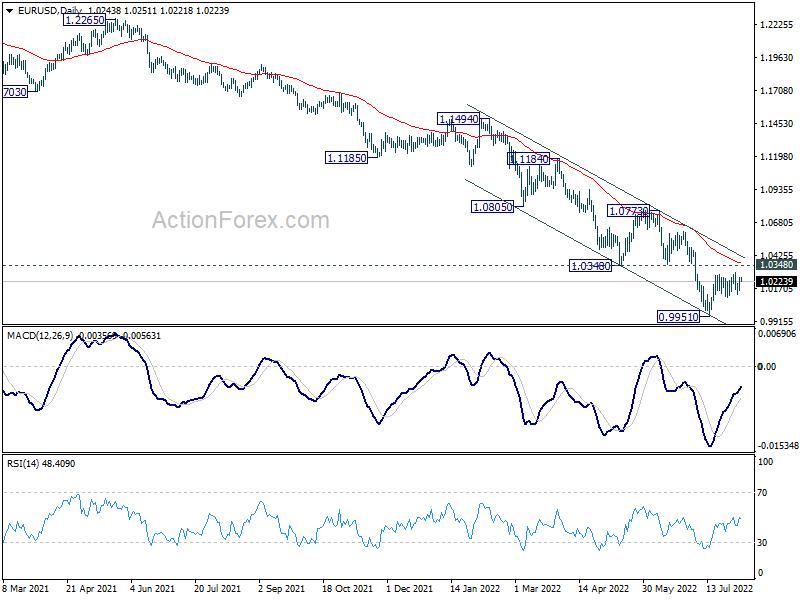

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0183; (P) 1.0219; (R1) 1.0282; More…

Range trading continues in EUR/USD and intraday bias remains neutral. With 1.0095 minor support intact, further rise is still mildly in favor. Rebound from 0.9951 will target 1.0348 support turned resistance. Break there will target channel resistance at 1.0432. On the downside, break of 1.0095 minor support will turn bias back to the downside, and bring retest of 0.9951 low instead.

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0773 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jul | 51.7 | 48.8 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | 2.20% | 1.90% | 1.00% | |

| 23:30 | JPY | Overall Household Spending Y/Y Jun | 3.50% | 1.50% | -0.50% | |

| 05:00 | JPY | Leading Economic Index JunP | 100.6 | 101.2 | 101.2 | |

| 06:00 | EUR | Germany Industrial Production M/M Jun | 0.40% | -0.20% | 0.20% | |

| 06:45 | EUR | France Trade Balance (EUR) Jun | -12.3B | -13.0B | ||

| 08:00 | EUR | Italy Industrial Output M/M Jun | -0.30% | -1.10% | ||

| 12:30 | USD | Nonfarm Payrolls Jul | 250K | 372K | ||

| 12:30 | USD | Unemployment Rate Jul | 3.60% | 3.60% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jul | 0.30% | 0.30% | ||

| 12:30 | CAD | Net Change in Employment Jul | 25.0K | -43.2K | ||

| 12:30 | CAD | Unemployment Rate Jul | 5.00% | 4.90% | ||

| 14:00 | CAD | Ivey PMI Jul | 60.3 | 62.2 |