{kind=link}

The American economy is losing power. The housing market has started to show cracks and businesses are warning they might fire workers as they attempt to defend profit margins. Quite frankly, history suggests that avoiding a recession would be a miracle. The good news is that recession doesn’t always mean Armageddon – it could be mild instead. In this piece, we examine the potential effects in the FX market.

Slowing down

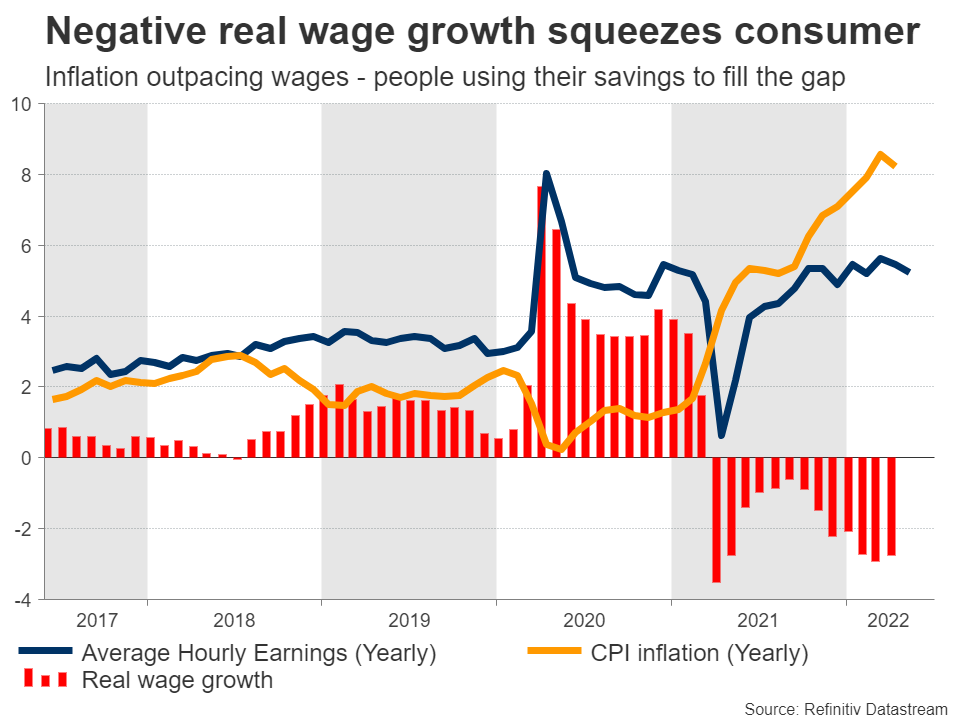

Storm clouds are gathering over the world’s largest economy. Consumers are feeling the burn of high inflation, as soaring food and energy prices force them to spend more on necessities. With real incomes falling so sharply, people are drawing down on the savings they accumulated during the lockdowns to fill the gap and maintain their lifestyle.

Federal Reserve officials have decided to go to war against inflation. They are raising interest rates with brute force to reduce demand across the economy, even though most of this inflation is caused by supply shocks that the Fed has no control over. The aim is to cool demand without causing too much damage and sparking a recession, so that there is a soft landing.

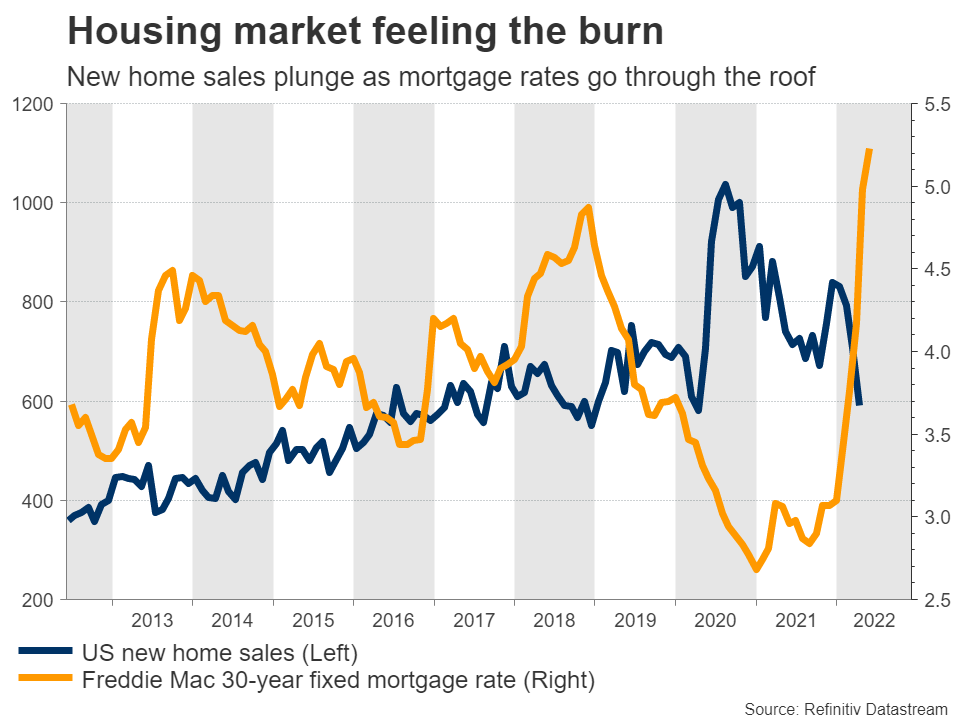

The impact is already visible in the housing market, where soaring mortgage rates have seen home sales decline dramatically in recent months. This is crucial because many Americans are used to refinancing their homes at ever-higher prices, which may not be possible anymore. Hence, household wealth is under pressure and the selloff in stock markets is making things worse.

At the same time, government spending is being rolled back at a stunning pace. Fiscal stimulus played a central role in boosting demand last year, but now many are criticizing the government for spending too much and amplifying inflationary forces.

The labor market has been a bastion of strength but even that is unlikely to remain immune for long as the economy slows. Some of the nation’s biggest employers like Amazon have already warned they could freeze hiring or lay off workers to manage costs, as they desperately try to protect profit margins from soaring inflation.

A look at history

Unfortunately, there haven’t been many soft landings over the past century. Almost every time that the Fed has embarked on a series of rate increases to fight inflation, the endgame has been a recession.

There have been three exceptions to this pattern – 1994, 1984, and 1965. The common characteristic in these episodes was that the Fed was trying to prevent inflation from moving even higher. This is a very different situation than today, when it is actively trying to bring inflation down.

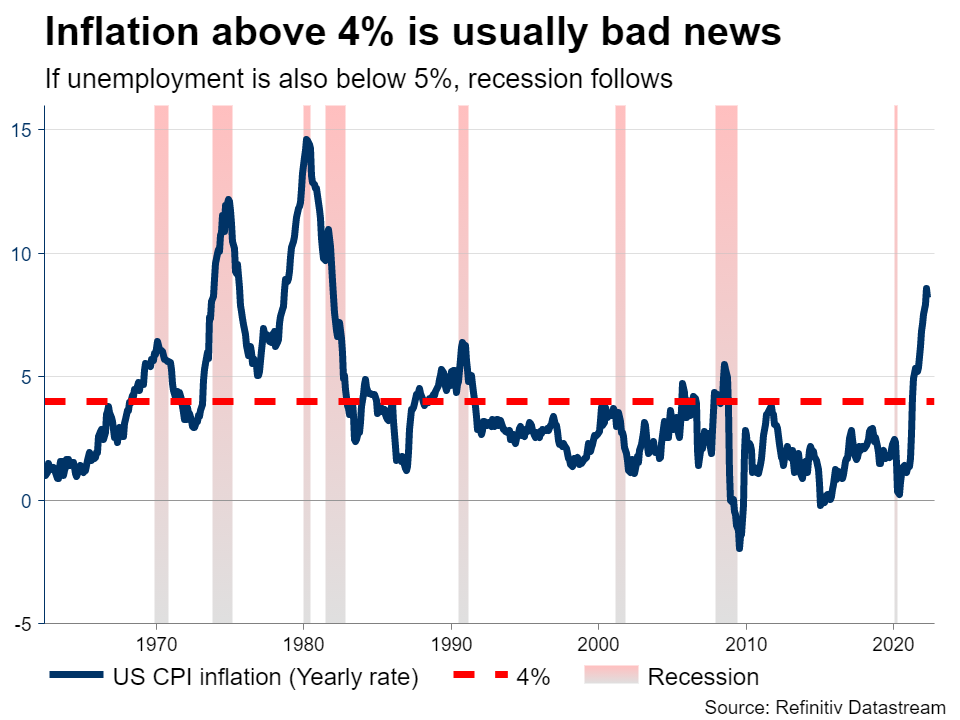

In fact, since 1955 there has never been an instance when inflation was above 4% and the unemployment rate was below 5% that wasn’t followed by a recession in the next two years. The US economy has already overshot both metrics by a mile.

Investors on alert

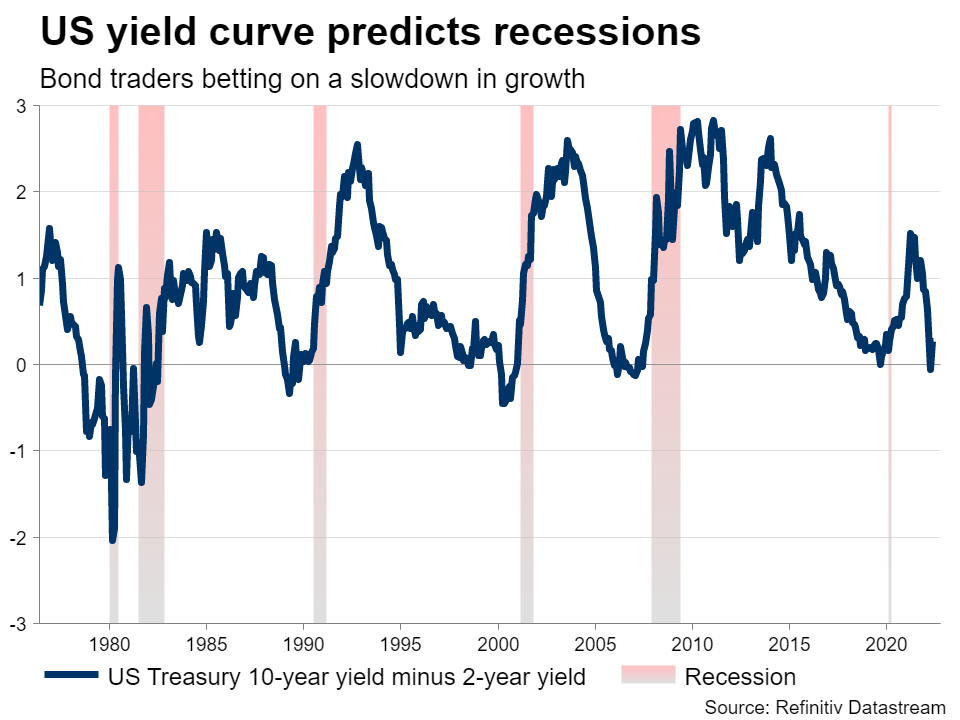

The bond market is already flashing warning signals. The most popular indicator that a recession is imminent is when long term Treasury yields fall below shorter term ones. It shows that investors are betting on a severe slowdown in economic growth and it has preceded recessions with terrifying accuracy over the last five decades.

This happened earlier this year, so bond traders are saying the distribution of outcomes has indeed shifted in this direction. Prominent economists like former Treasury Secretary Larry Summers share this view, along with business leaders like the CEO of JPMorgan Chase, who recently warned a hurricane is about to hit the economy.

Some good news

While a downturn seems increasingly likely, it is fruitful to remember that a recession is not the end of the world. There have been thirteen recessions since the end of World War II and most of them were ‘plain vanilla’ – brief and shallow. The prolonged suffering many people experienced after the 2008 crisis was an extreme outlier, not the norm.

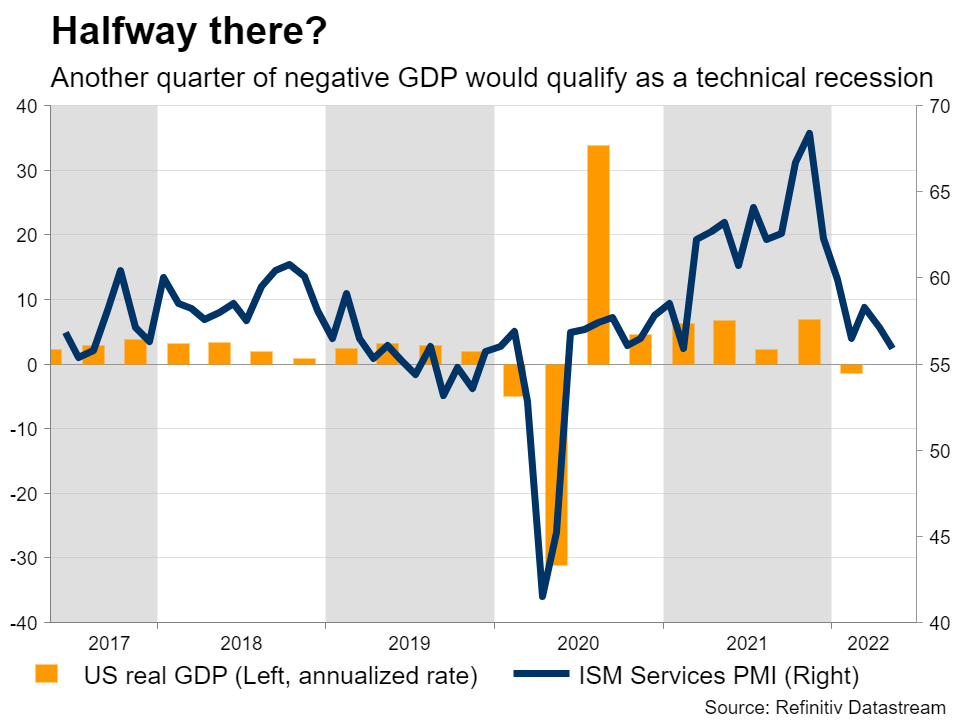

A couple of quarters of negative GDP growth would qualify as a recession but not necessarily a crisis. In fact, we are already halfway there. Economic growth in the US turned negative in the first quarter and the Atlanta Fed GDPNow model estimates growth at only 0.9% this quarter.

Another point to consider is that historically, the Fed has reversed course at the first sign of trouble. After all, an economic slump would probably destroy enough demand to crush inflation. This is another argument as to why any recession might be mild. The Fed will take its foot off the brakes as soon as the engine starts to fail.

Market implications

The US dollar typically performs well when investors panic about a recession, even if the crisis originates from America. This dynamic boils down to the dollar’s reserve currency status acting as a hedge against uncertainty and the unparalleled liquidity it offers businesses even during times of market stress.

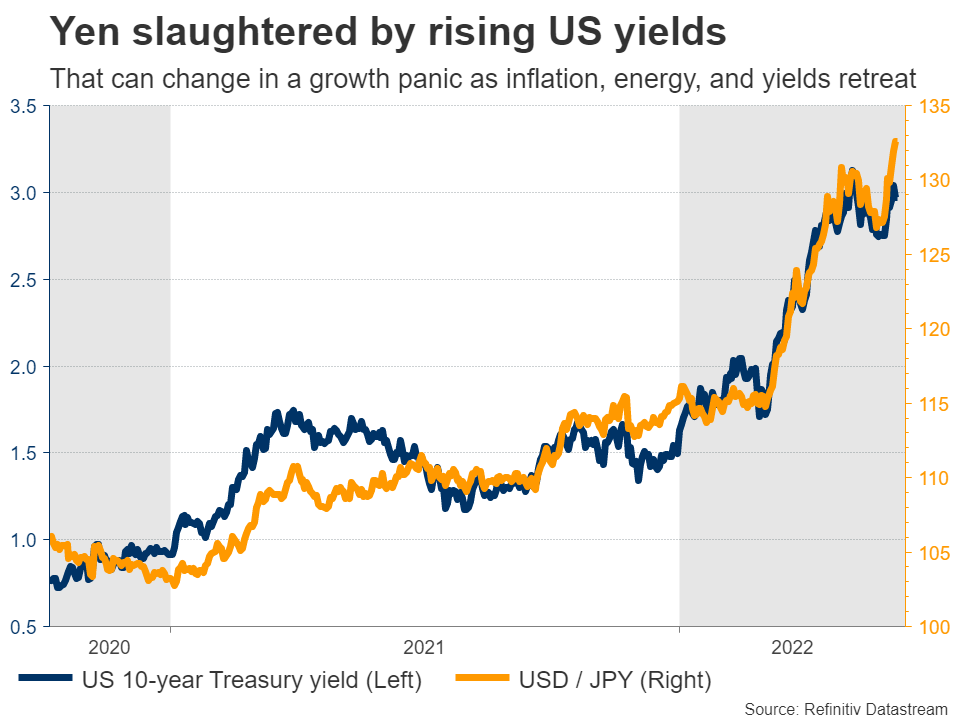

Another currency that’s likely to shine is the Japanese yen. The yen has been slaughtered so far this year by rising yields in the rest of the world and a trade shock as energy prices soared. But in case a recession hits, inflation expectations and yields globally are likely to fall back alongside energy prices, helping the yen to recover.

Meanwhile, the currencies likely to underperform in this scenario are the commodity-linked dollars, and to a lesser extent the British pound. The Australian and New Zealand dollars are tied to global growth since their economies rely on commodity exports, while sterling has a strong correlation to stock markets, trading almost like a proxy for global risk sentiment. Therefore, pairs like aussie/yen or sterling/yen could experience the sharpest moves.

All told, a recession is not inevitable. There is a path where the Fed manages to engineer a soft landing with growth slowing just enough to cool inflation. It just doesn’t seem very realistic from a historical perspective. Instead, let’s hope that any downturn turns out to be mild, causing little damage and ending quickly.