{kind=link}

Overall, the moves in the forex markets are still indecisive. Dollar and Yen are striking back today and rise broadly. Swiss Franc follows as the third strongest, suggesting a risk-off undertone. Nevertheless, other markets are still relatively steady. New Zealand Dollar’s post-RBNZ rally faded rather quickly. But for now, Aussie is the weakest one, followed by Euro and then Canadian. Sterling and Kiwi are just mixed.

Focuses will turn to FOMC minutes. From recent comments, Fed official displayed a consensus on the plan of 50bps hike per meeting, at least for the next few ones. FOMC minutes should reflect the discussions and affirm this message too. Meanwhile what next beyond August, as well as the end point for the year would remain data dependent.

Technically, it’s still early to conclude that Dollar has already completed its near term correction. But while still remote, some levels could be put under radar. The levels include 1.0563 minor support in EUR/USD, 1.2329 support in GBP/USD, 0.6948 support in AUD/USD and 0.9763 minor resistance in USD/CHF. Dollar should have a sustainable rally if these levels are all violated.

In Europe, at the time of writing, FTSE is up 0.33%. DAX is up 0.06%. CAC is up 0.06%. Germany 10-year yield dropped -0.033 to 0.934. Earlier in Asia, Nikkei dropped -0.26%. Hong Kong HSI rose 0.29%. China Shanghai SSE rose 1.19%. Singapore Strait Times dropped -0.48%. Japan 10-year JGB yield dropped -0.0202 to 0.212.

US durable goods orders rose 0.4% in Apr, ex-transport orders up 0.3%

US durable goods orders rose 0.4% mom to USD 265.3B in April, below expectation of 0.6% mom. Ex-transport orders rose 0.3% mom, below expectation of 0.6% mom. Ex-defense orders rose 0.3% mom. Transportation equipment, rose 0.6% mom to USD 86.7B.

ECB Panetta: Policy normalization needs to be clearly defined

ECB Executive Board member Fabio Panetta said in a speech, “the very shocks that have led to a surge in inflation (in Eurozone) are also depressing output”. Hence, “the inflation path is starting from a much higher point but the medium-term inflation outlook is characterised by high uncertainty.” Policy normalization needs to be “clearly defined”.

Panetta explained that normalization does not mean moving to a “neutral” policy stance. it shouldn’t be assessed against “unobservable reference points” such as neutral rate. And, it “does not imply adjusting unconventional instruments more rapidly than conventional ones”.

Normalization is “a process of gradually reducing that stimulus in a way that firmly anchors the inflation path at 2% over the medium term”, he said.

Germany Gfk consumer confidence rose to -26, war and inflation still weighing

Germany Gfk consumer confidence for June rose slightly from -2.66 to -26.0, worse than expectation of -25.6. In May, economic expectations rose from -16.4 to -9.3. Income expectations rose from -31.3 to -23.7. Propensity to buy dropped from -10.6 to -11.1.

“Although this means that the consumer climate has improved slightly, consumer sentiment is still at an all-time low,” explains Rolf Bürkl, GfK consumer expert. “Despite further easing of pandemic-related restrictions, the war in Ukraine and especially high inflation are weighing heavily on consumer sentiment.”

RBNZ hikes by 50bps, rate projected to peak at 3.9%

RBNZ raised the Official Cash Rate by 50bps to 2.00% as widely expected. The central bank now projects OCR to peak at 3.9% in Q2 of 2023, before moving down slightly starting from Q3 2024.

In the statement, RBNZ said: “The Committee viewed the projected path of the OCR as consistent with achieving its primary inflation and employment objectives without causing unnecessary instability in output, interest rates and the exchange rate. Once aggregate supply and demand are more in balance, the OCR can then return to a lower, more neutral, level.”

Also in the new forecasts, GDP would grow 5.4% in 2022, then slow to 3.2% in 2023, 1.3% in 2024, and 1.2% in 2025. CPI would average 6.9% in 2022, then slow to 4.4% in 2023, 2.5% in 2024, and 2.0% in 2025. Unemployment rate is projected to be at 3.2% in 2022, then gradually climb to 3.8% in 2023, 4.4% in 2024, and 4.7% in 2025.

Japan government concerned of re-spread of coronavirus in China and Ukraine war

In May’s Monthly Economic Report, Japan’s government maintained that the economy “shows movement of picking up”. Private consumption, business investment and industrial production have “shown movement of picking up”. Exports were still “almost flat”.

Employment assessment was upgrade slightly to “shows movement of picking up” rather than just in “some components. Consumer prices “have been rising recently”, with “moderately” dropped.

The government also warned that “full attention should be given to the downside risks due to supply-side constraints, rising raw material prices and fluctuations in the financial and capital markets while there are concerns regarding the effects of the re-spread of the Novel Coronavirus in China and lengthening the state of affairs of Ukraine”.

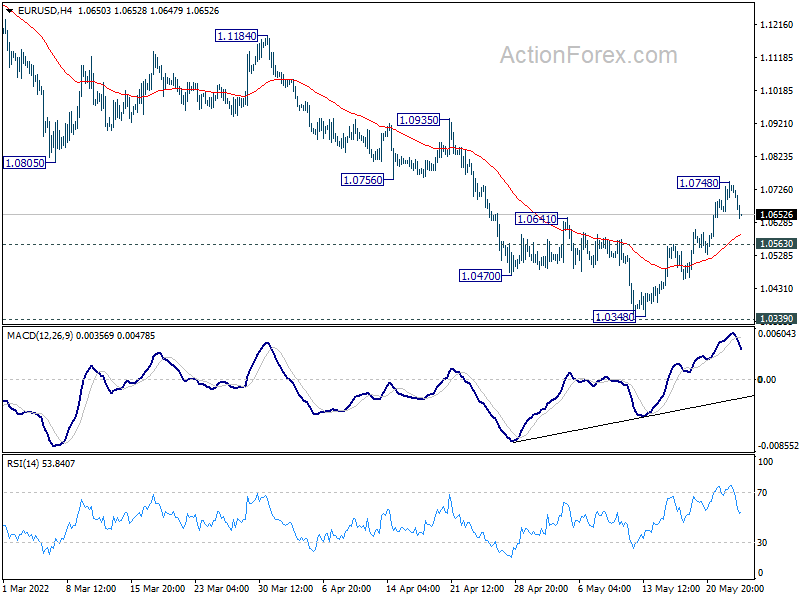

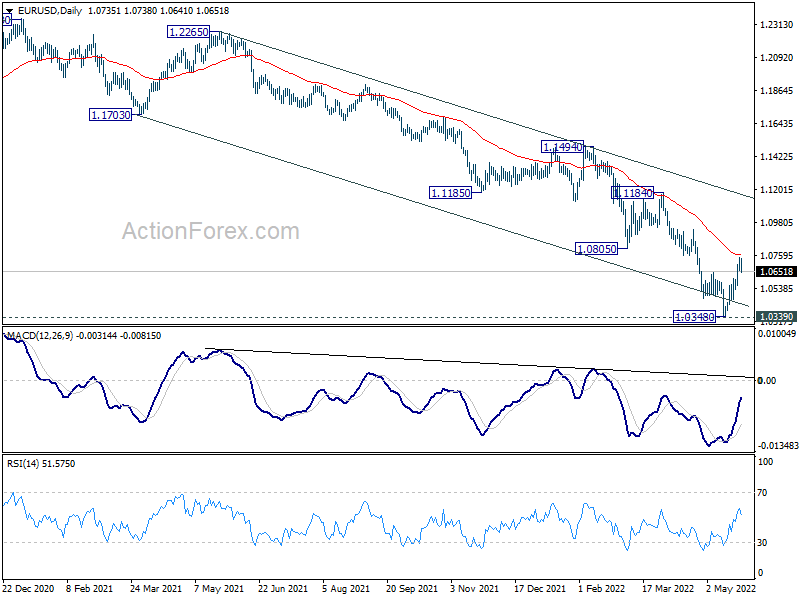

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0682; (P) 1.0715 (R1) 1.0770; More…

Intraday bias in EUR/USD is turned neutral first with today’s retreat. Another rise could be seen with 1.0563 minor support intact. Above 1.0748 will resume the rebound from 1.0348. Firm break of 55 day EMA (now at 1.0760) will target 1.0935 resistance next. However, below 1.0563 minor support will turn intraday bias back to the downside for retesting 1.0348 low instead.

In the bigger picture, focus stays on 1.0339 long term support (2017 low). Decisive break there will resume whole down trend from 1.6039 (2008 high). Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. However, firm break of 1.0805 support turned resistance will delay this bearish case and bring medium term corrective rebound first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Construction Work Done Q1 | -0.90% | 1.00% | -0.40% | 0.60% |

| 02:00 | NZD | RBNZ Interest Rate Decision | 2.00% | 2.00% | 1.50% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Jun | -26 | -25.6 | -26.5 | -26.6 |

| 06:00 | EUR | Germany GDP Q/Q Q1 F | 0.20% | 0.20% | 0.20% | |

| 08:00 | CHF | Credit Suisse Economic Expectations May | -52.6 | -51.6 | ||

| 12:30 | USD | Durable Goods Orders Apr | 0.40% | 0.60% | 1.10% | |

| 12:30 | USD | Durable Goods Orders ex Transport Apr | 0.30% | 0.60% | 1.40% | |

| 14:30 | USD | Crude Oil Inventories | -2.2M | -3.4M | ||

| 18:00 | USD | FOMC Minutes |