{kind=link}

US stock markets closed last Friday with a substantial and widespread gain. Do we see a dead cat bounce or the beginning of a recovery? So far, there are more reasons to suspect the former.

The CNN Fear & Greed Index was down to 7 last week, rebounding to 12 by Monday. Current levels are still in extreme fear territory, but a rebound from multi-month lows often heralds a return of buyers who think the emotional sell-off has gone too far.

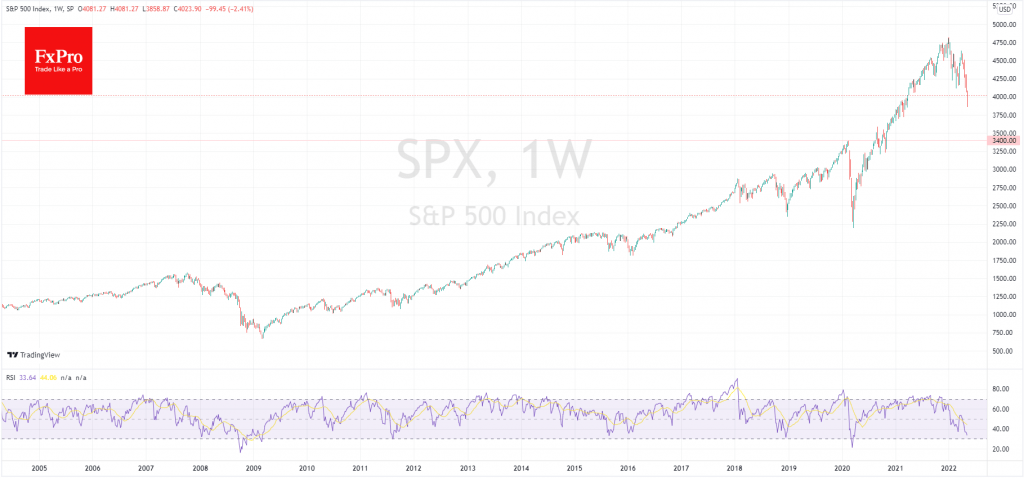

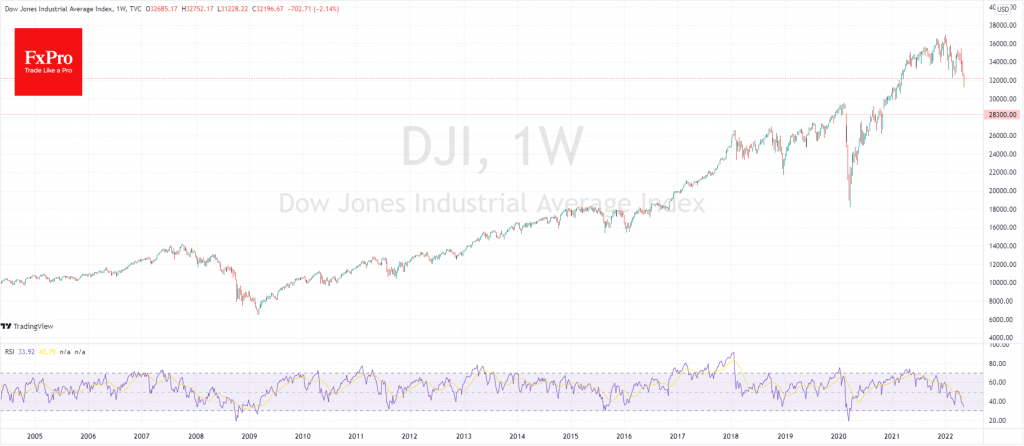

Technically, the S&P500 has managed to bounce back from a bear market territory and has temporarily returned to levels above 4000, while Dow is above 32000.

However, in our view, we saw positional profit-taking on Friday, but not the end of a downward trend. The weekly chart’s S&P500 and Dow Jones indices have not yet reached the oversold area where they appeared attractive for buying in March 2020.

Particularly worrying is the comparatively quiet nature of the sell-off. The market volatility index VIX remains the only one of the seven “Fear and Greed” components in neutral territory.

The latter signals a systematic sell-off of assets rather than a panic flight. This is not a straightforward approach for the market to change.

Treasury and Fed officials are often willing to flood the markets with liquidity in cases of extreme volatility. Still, without it, they see what is happening as a natural process in which it is harmful to interfere.

The technical picture in the US indices now more closely resembles the first half of 2008. That means that the climax of the panic (October 2008) and the bottom (March 2009) are yet to come.

This is also supported by the Fed’s rhetoric that hopes to avert an economic recession through policy tightening is prevented. So far, we can see the intention of a 50-point hike in the next two meetings in June and July after a similar move in May at the same time as the asset sales from the balance sheet.

Monetary tightening locally looks like a breeding ground for bears, who might target the area below 30000 in the Dow Jones, trying to close the gap near 28300 from November 2020.

For the S&P500, the bears’ ultimate target might be the 3300-3400 area, where the pre-pandemic peak and the starting point of the rally in November after the Biden victory are concentrated.

Perhaps only by zeroing in on all the coronavirus and retail-associated gains in equities and taking inflation into negative territory could we see an inflow of long-term capital into equities.