{kind=link}

The tragic developments in the Ukraine have not triggered any significant changes in our views on Australian financial markets.

While the shock of aggressive military action in Europe has rattled equity and commodity markets, the keys to assessing any lasting effects are the direct impact that Ukraine and Russia have on global economic activity and Russia’s special role in energy markets.

Apart from energy, Russia has limited global significance – its economic not much larger than Australia’s; with a limited role in global supply chains; and, as one US bank points out, representing around 0.1% of all sales across US S&P500 companies.

US President Biden clearly pointed out that sanctions on Russian financial activities would not include energy payments – his argument is that given Russia’s significance in energy markets, banning energy exports would place a huge burden on global consumers.

While the US is energy independent, Russia controls around 8% of global oil production, including 25% of the European market and 35% of European gas.

Eliminating such supply in energy markets that are already stretched with perilously low inventory levels would surely put enormous upward pressure on crude prices.

While there is certain to be significant short term volatility, comfort that the crisis is unlikely to severely affect global supplies of energy and therefore add further upward pressure on inflation is likely to see equity markets settle back – as has been the case with previous geopolitical disruptions that do not have lasting effects of global inflation or economic activity.

With this background, our assessment of Thursday’s release of the Wage Price Index (WPI) is that while the Index printed in line with our expectations there was evidence of some intensifying wage pressures, ableit insufficient at this stage to justify the RBA raising rates before our schedule of the August meeting.

The headline increase for the quarter was 0.7%, following 0.6% and 0.4% in the previous two quarters.

We expect the March quarter Index to print 0.8% lifting the six month annualised pace to 3% – enough to justify the first rate hike given an expected lift in the other measures of wage pressures that the RBA will also be considering. These include turnover in the labour market; pressure on bonuses and overtime; average wages in the national accounts; job vacancies and job ads; surveys of businesses and the higher frequency components of the WPI covering individual agreements.

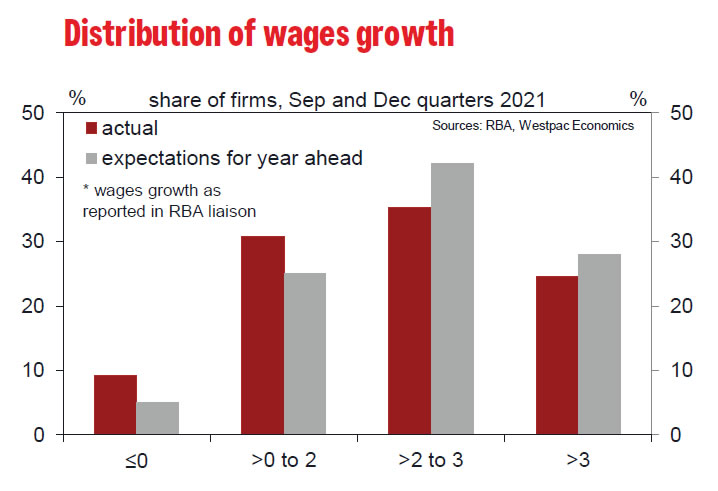

Already the RBA’s own liaison work points to the clear movement towards stronger wage pressures, (see figure from RBA’s February Statement on Monetary Policy) where there is a clear increase in the number of businesses expecting faster increases in wages.

The components of the latest WPI are difficult to assess given the high seasonality of individual agreements and that these figures are not seasonally adjusted. However, the sectors receiving the highest increases the quarter – hospitality; retail; manufacturing; construction; real estate; and professional services – point to the out-performance of sectors that are more heavily influence by individual agreements.

We do not think it will be necessary for the RBA to wait to see a 3% print for annual growth in the WPI before it can act given that it has already highlighted that the Index only measures base rates.

That 3% print is likely to arrive on August 24 when the June quarter WPI is released. The June quarter 2021 printed a COVIDaffected 0.4%. Once that drops out of the annual numbers the Index will lift significantly.

If, as we expect, the next two WPI prints are 0.8% then the annual growth rate will lift to around 3% in June from 2.5% in March.

But we believe that given the likely prints on headline and underlying inflation for the March and June quarters, which will be printing on on April 27 and July 27, the RBA will have enough information to move in August.

The Governor indicated recently to the Economics Committee of the House of Representatives that he would like to see two more inflation prints – not two more WPI prints.

Remember that central banks favour adopting some form of tightening bias before they actually start the tightening process. By the June Board meeting the March quarter CPI will be known as well as the March quarter WPI.

The March quarter CPI is going to see a very substantial lift in both headline and underlying inflation. Annual headline inflation is forecast to lift from 3.5% to 4.2% and underlying inflation to lift from 2.6% to 3.1%.

That is based on the crude oil price holding in the ‘high 90s’ implying no significant relief but as discussed above no surge above the US$100/bbl level that would result from disruptions to Russian oil supplies.

In fact we see more upside risk from housing in the March release although we do not expect a significant impact on the underlying measure.

That type of inflation lift combined with the ongoing evidence of a tightening labour market, including the 3% ‘momentum’ in the WPI will be sufficient for the RBA to begin the process of preparing the market for a rate hike at the June and July meetings.

At the August meeting the Board will have received further evidence of these rising inflationary pressures with the June inflation report where we expect underlying inflation to lift to 3.5% – the final piece to the puzzle to justify the Board delivering on its bias at the August meeting.

Because we are expecting some moderate easing in the oil price by the June quarter, we only expect headline inflation to have lifted to 4.3% from 4.2%.

And, as discussed, these views on the oil price are based on Russia being allowed to maintain its flow of oil.