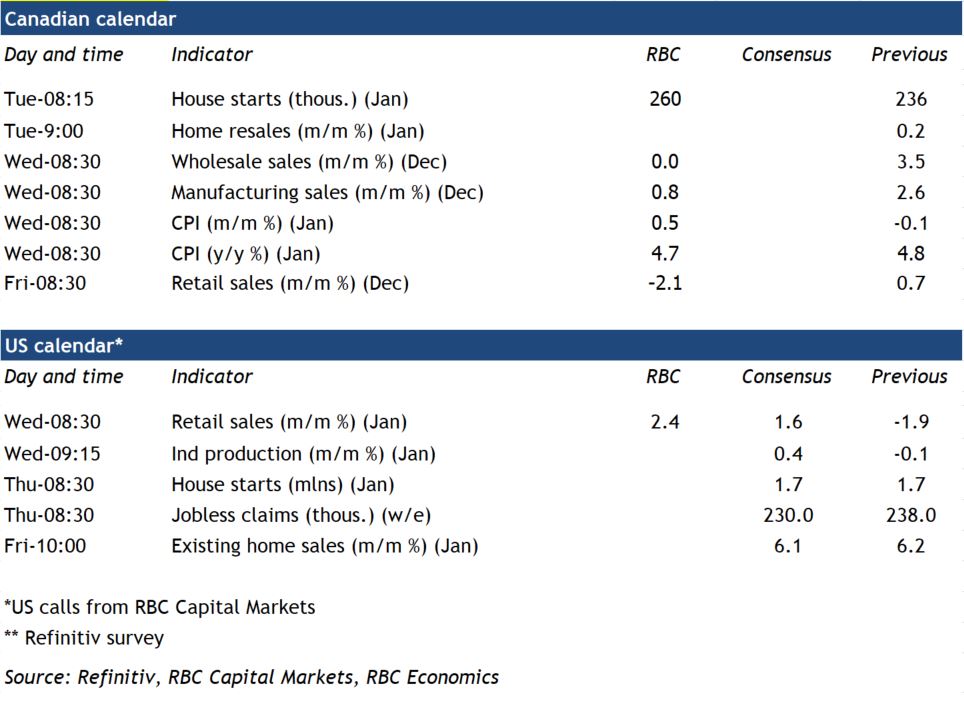

{kind=link}

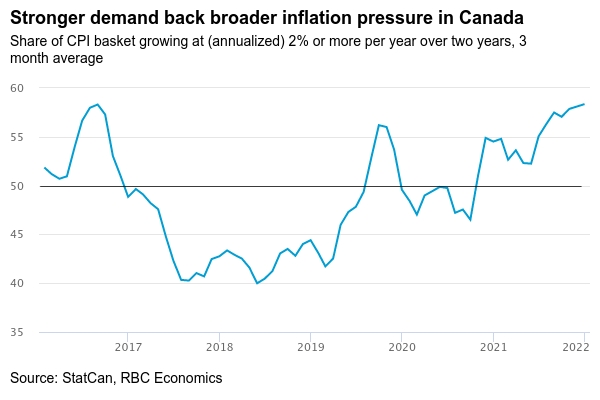

Canada’s January inflation report will be the headline event next week after another acceleration in the U.S. numbers. The Canadian CPI year-over-year growth rate is expected to have ticked down to 4.7% in January, little changed from December. Gasoline and home buying costs combined are expected to once again account for just under half of the headline price gain—as they did in December. Price growth is still being biased higher by so-called ‘base effects,’ or comparisons with a year ago when prices were lower and the pandemic economic impact was more severe. But price pressures have been broadening out into more goods as well. By our count, close to 60% of the consumer price basket has been running at more than 2% per year versus pre-pandemic levels.

Travel spending has deteriorated substantially since December and the employment count dropped sharply in January. But household purchasing power will have held up much better thanks to government support programs. Early indicators are pointing to a quick rebound in spending with containment measures easing into February. A resurgence in employment, strong household demand, and higher oil prices are expected to keep a floor under inflation growth in the near term, even as pandemic base effects ease. Given ongoing inflation pressure and the expectation that Omicron will ultimately have a temporary impact on labour markets, there is little reason for the Bank of Canada to delay rate hikes further. We expect a 25 basis point increase in March and could see a follow-up hike as soon as April.

Week ahead data watch:

- The home resale market remained exceptionally tight in January with early regional reports pointing to strong resales limited only by lack of listings and price pressures remaining exceptionally firm.

- The flash estimate of December manufacturing sales was 0.8%. Plastic and rubber product shipments, reportedly, rose sharply while an easing of supply chain pressures allowed another increase in motor vehicle production. Petroleum and coal sales likely declined on lower prices with oil prices dipping in December on early Omicron worries.

- Retail sales fell 2.1% in December according to preliminary Statistics Canada data, broadly in line with our own tracking of credit card transactions in the month. More attention will be paid to the January preliminary estimate, where we expect another 1% dip with weakness earlier in the month.